Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

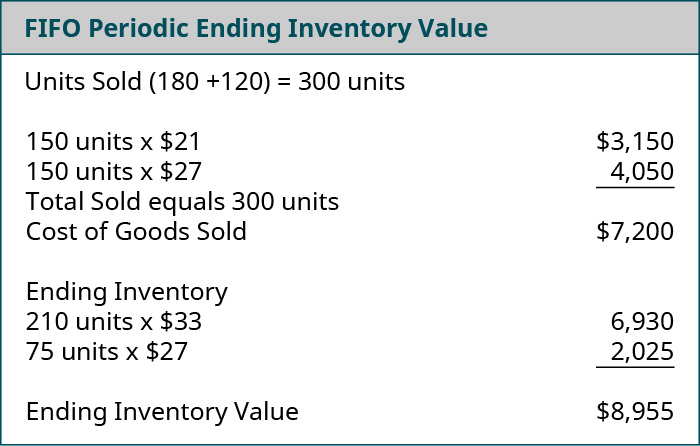

How do you calculate gross profit FIFO?

Gross profit rate is $294,000 divided by $594,000, or 0.49. Beside above, how do you calculate gross profit FIFO? Gross profit method. Add together the cost of beginning inventory and the cost of purchases during the period to arrive at the cost of goods available for sale. Multiply (1 - expected gross profit %) by sales during the period to ...

What is the difference between FIFO vs. LIFO?

- First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method.

- Last-in, first-out (LIFO) assumes the last inventory added will be the first sold.

- Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

How to calculate LIFO and FIFO?

These are the simple steps that help to convert a LIFO-based statement to a FIFO-based statement:

- First, you have to add the LIFO reserve to LIFO inventory

- Then, you have to deduct the excess cash that saved from lower taxes under LIFO (i:e. ...

- Very next, you have to increase the retained earnings component of shareholders’ equity by the LIFO reserve x (1-T)

- Finally, in the income statement, FIFO COGS = LIFO COGS – Δ LIFO Reserve

How do you calculate COGS from LIFO to FIFO?

0:0416:01Calculate Cost of Goods Sold Using LIFO & FIFO 423 - YouTubeYouTubeStart of suggested clipEnd of suggested clipWe're going to work a practice problem in excel related to calculating cost of goods sold using bothMoreWe're going to work a practice problem in excel related to calculating cost of goods sold using both the last in first out method and the first and first out method otherwise known as the lifo method

What is the formula for calculating COGS?

At a basic level, the cost of goods sold formula is: Starting inventory + purchases − ending inventory = cost of goods sold.

Does FIFO increase COGS?

If a company uses the FIFO inventory method, the first items purchased and placed in inventory are the ones that were first sold. If the older inventory items were purchased when prices were higher, FIFO would lead to a higher cost of goods sold and lower net income when compared to LIFO.

How does FIFO impact cost of goods sold?

(a) First-in, First-out (FIFO): Under FIFO, the cost of goods sold is based upon the cost of material bought earliest in the period, while the cost of inventory is based upon the cost of material bought later in the year. This results in inventory being valued close to current replacement cost.

How do you find COGS without ending inventory?

Multiply the gross profit percentage by sales to find the estimated cost of goods sold. Subtract the cost of goods available for sold from the cost of goods sold to get the ending inventory.

What is cost of goods sold with example?

The cost of goods made or bought is adjusted according to change in inventory. For example, if 500 units are made or bought but inventory rises by 50 units, then the cost of 450 units is cost of goods sold. If inventory decreases by 50 units, the cost of 550 units is cost of goods sold.

Why is COGS lower in FIFO?

More on FIFO Since FIFO (first-in, first out) is moving the older/lower costs to the cost of goods sold, the recent/higher costs are in inventory. The lower cost of goods sold generally results in larger amounts of gross profit, net income, taxable income, income tax payments, and certain financial ratios.

How does LIFO and FIFO affect cost of goods sold?

Decreasing Inventory Costs As for declining inventory costs, the impacts of FIFO vs LIFO are: If Inventory Costs Decreased ➝ Higher COGS Under FIFO (Lower Net Income) If Inventory Costs Decreased ➝ Lower COGS Under LIFO (Higher Net Income)

What is FIFO method with example?

Example of FIFO Imagine if a company purchased 100 items for $10 each, then later purchased 100 more items for $15 each. Then, the company sold 60 items. Under the FIFO method, the cost of goods sold for each of the 60 items is $10/unit because the first goods purchased are the first goods sold.

How do you calculate cost of goods sold using LIFO?

2:458:12LIFO Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipFrom which dates with which prices are going to go on the cost of goods sold and which are going toMoreFrom which dates with which prices are going to go on the cost of goods sold and which are going to be in our ending inventory and we're making an assumption and in this case we're going to assume.

How does FIFO affect ending inventory?

Under FIFO, your Cost of Goods Sold (COGS) will be calculated using the unit cost of the oldest inventory first. The value of your ending inventory will then be based on the most recent inventory you purchased.

Why is FIFO the best method?

FIFO is more likely to give accurate results. This is because calculating profit from stock is more straightforward, meaning your financial statements are easy to update, as well as saving both time and money. It also means that old stock does not get re-counted or left for so long it becomes unusable.

How do you calculate COGS on a balance sheet?

How to Calculate Cost of Goods Sold. The cost of goods sold formula, also referred to as the COGS formula is: Beginning Inventory + New Purchases - Ending Inventory = Cost of Goods Sold. The beginning inventory is the inventory balance on the balance sheet from the previous accounting period.

How do you calculate COGS on an income statement?

COGS, sometimes called “cost of sales,” is reported on a company's income statement, right beneath the revenue line.

How do you calculate COGS on Excel?

Cost of Goods Sold = Beginning Inventory + Purchases during the year – Ending InventoryCost of Goods Sold = Beginning Inventory + Purchases during the year – Ending Inventory.Cost of Goods Sold = $20000 + $5000 – $15000.Cost of Goods Sold = $10000.

Whats included in COGS?

Cost of goods sold (COGS) refers to the direct costs of producing the goods sold by a company. This amount includes the cost of the materials and labor directly used to create the good. It excludes indirect expenses, such as distribution costs and sales force costs.

What does FIFO mean in accounting?

FIFO is an acronym. It stands for “First-In, First-Out” and is used for cost flow assumption purposes. Cost flow assumptions refers to the method of moving the cost of a company’s product out of its inventory to its cost of goods sold. Inventory refers to:

When calculating COGS, what is the company going to go by?

Therefore, when calculating COGS (Cost of Goods Sold), the company will go by those specific inventory costs. Although the oldest inventory may not always be the first sold, the FIFO method is not actually linked to the tracking of physical inventory, just inventory totals. However, FIFO makes this assumption in order for ...

What is the difference between FIFO and LIFO?

The FIFO (“First-In, First-Out”) method means that the cost of a company’s oldest inventory is used in the COGS (Cost of Goods Sold) calculation. LIFO (“Last-In, First-Out”) means that the cost of a company’s most recent inventory is used instead. Here’s What We’ll Cover:

Why use LIFO or FIFO?

The LIFO method for financial accounting may be used over FIFO when the cost of inventory is increasing, perhaps due to inflation. Using FIFO means the cost of a sale will be higher because the more expensive items in inventory are being sold off first.

What is FIFO in COGS?

FIFO means you would calculate your COGS as $15 + $25 = $40 as your COGs expense. Your remaining bookend set, the one priced at $10, is the cost of the most recent merchandise.

What is FIFO in inventory?

FIFO is also adaptable to both types of inventory cycles: perpetual (inventory taken year-round constantly) or periodic (inventory taken certain times of the year)

What is FIFO in grocery?

The FIFO inventory method is popular with grocery stores and other stores that sell perishables, but it has plenty of applications for other retailers as well. As a retailer, you probably aren’t ordering every bit of your inventory at the same time for a number of reasons. The available inventory from vendors consistently changes.

Why do you use FIFO?

Using FIFO helps you mitigate your inflation losses because, as the cost of goods rises, you’re able to adjust your prices of the previous stock and sell it at a higher cost as inflation dictates.

Does Erply POS use FIFO?

If you haven’t learned FIFO inventory calculation yet as a way of calculating your inventory, it’s time to start. Erply POS uses FIFO and features its practices built into the system to offer you a no-hassle way of calculating your inventory valuation.

What is the inventory costing method?

The inventory costing method your company chooses will directly affect the value of the cost of goods sold during each accounting period. There are three inventory costing methods: First In, First Out (FIFO). As the title implies, the first products acquired during the accounting period will be sold.

How much is Hallsen's Q2 inventory?

Hallsen, Inc. has a quarterly accounting period. Their Q2 beginning inventory had a value of $7000. The goods purchased over Q2 are valued at $4000, and the ending inventory is valued at $3000.

What is the beginning inventory?

Your beginning inventory is the inventory value at the beginning of the accounting period or the value of the inventory left over from the previous accounting period. Cost of goods. The cost of goods is the cost of any product bought or made throughout the accounting period.

What is included in the cost of revenue?

In addition to production costs, the cost of revenue also includes costs such as marketing, shipping and distribution, commissions, and discounts applied. Like the cost of goods sold, the cost of revenue does not include any indirect costs.

Is COGS a business expense?

COGS is a deductible business expense. The IRS has a detailed explanation of how to calculate your cost of goods sold properly. You must follow the set rules and regulations when calculating and filing. Otherwise, you run the risk of an audit later.

Can the cost of goods sold predict the future?

The cost of goods sold can’t give any predictions for the future. It simply accounts for current costs. COGS is just one metric. Investors and analysts cannot rely on the cost of goods sold to give them all the information they require to make decisions.

Does cost of goods help in profit calculation?

Yes, it aids in profit calculation, but it can do so much more. It can help you create a pricing strategy. When you understand the cost of goods sold, you can set or increase prices to leave a healthy profit margin. It can also help you against your competitors.

How to calculate COGS?

FIFO is an alternate method used to account for inventory costs. To calculate COGS using the FIFO method, first take a physical inventory count at the start date and again at the end date. It is important that these counts be 100% accurate.

When to use average cost method?

Companies use the average cost method when their products are easily substituted or physically indistinguishable from each other, such as commodities like minerals, oil and gas. Most companies that use the Average Cost Reporting Method compute the average cost of goods on a quarterly basis.

What is GAAP accounting?

There are Generally Accepted Accounting Principles (GAAP) that dictate the reporting functions that rely on the COGS calculation. Publicly traded companies must submit financial reports based on GAAP, so it is important to pick the COGS calculation and reporting method that will best suit your business.

Is COGS lower under FIFO?

Your COGS is lower under the FIFO reporting method and your profit is higher when inventory costs are rising. In this case your earlier inventory cost less than the inventory acquired later in the week, assuming both are sold to the consumer at the same price.

How to find average COGS?

To find the average COGS, you take the opening inventory balance as well as the purchases that you have done in a period of time to find the average cost. The average price per unit is used to find the COGS and the Closing Inventory Balance.

What does FIFO stand for in accounting?

FIFO stands for “First In First Out”. Both LIFO and FIFO are the cost accounting Frictions that can lead to very different numbers of Cost Of Goods Sold and Gross Profit. Let’s work through a visual example of FIFO and LIFO. We will do the inventory accounting for a hypothetical company, Toy Giraffe INC.

What is a COGS?

COGS stands for Cost Of Goods Sold. It is the cost that a company pays to produce its product or service. All companies incur/bears the cost in the creation of their products. The labour, material, and operating costs, such as building rentals and utility expenses, contribute to the COGS calculation and the final product’s final price. ...

What is the beginning inventory value?

Beginning Inventory Value is the total stock level at the start of the period you have selected.

What is cost of goods sold?

Cost of Goods Sold (COGS) calculates the total cost incurred in getting the product ready for sale in the market. However, COGS doesn't include all the costs incurred while running the business. It mainly comprises direct expenses incurred in making the finished product or getting it to your customer.

What Is the Cost of Goods Sold (COGS)?

Cost of goods sold refers to the total costs associated with the production of goods that a company sells. COGS is typically used by manufacturers, retailers, and wholesalers as these businesses sell or resell products to generate revenue.

What Is Included in COGS?

Cost of goods sold includes the costs related to acquiring or producing a physical product to sell or resell. The costs often include:

Why COGS Is Important

The cost of goods sold is an important metric for a number of reasons.

How do you calculate the variable cost of goods sold?

Variable costs are costs that change from one time period to another, often changing in tandem with sales. In contrast, fixed costs are costs that remain the same. The cost of goods sold is a variable cost because it changes. To calculate it, add the beginning inventory value to the additional inventory cost and subtract the ending inventory value.

What items are included in the cost of goods sold?

The five items included in the cost of goods sold are: inventory at the start of a new tax year; purchases not including cost of items used for personal usage; labor costs; material and supplies; and other costs.

What is not included in COGS?

COGS does not include costs such as overhead, sales and marketing, and other fixed expenses. COGS only includes costs and expenses related to producing or purchasing products for sale or resale such as storage and direct labor costs.

What is FIFO in accounting?

The company makes a physical count at the end of each accounting period to find the number of units in ending inventory. The company then applies first-in, first-out (FIFO) method to compute the cost of ending inventory.

What is FIFO in inventory?

First-in, first-out (FIFO) method in periodic inventory system. Under first-in, first-out (FIFO) method, the costs are chronologically charged to cost of goods sold (COGS) i.e., the first costs incurred are first costs charged to cost of goods sold (COGS).

How to calculate cost of goods sold?

Formula method: Under formula method, the cost of goods sold would be computed as follows: Cost of goods sold = Cost of units in beginning inventory + Cost of units purchased during the period – Cost of units in ending inventory.