Inputs:

- First of all, you just have to enter the quantity of each unit purchases

- Then, you have to add the quantity of the price/unit you purchased

- Also, the lifo fifo method calculator provides you with options of adding more purchases “one by one” or multiple

- Then, you have to enter the total units sold from your number of purchases

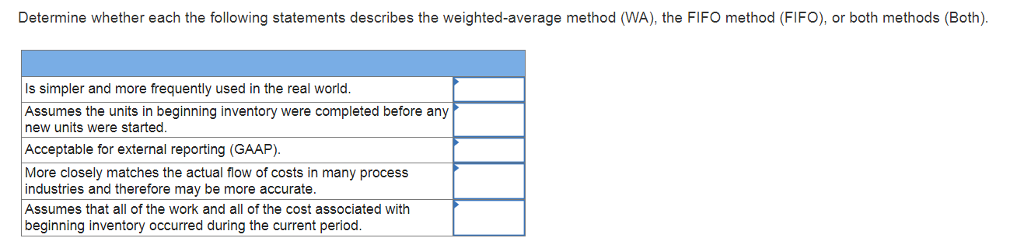

What is the difference between FIFO and average method?

Difference between FIFO and average costing method: 1. Primary distinction: The primary difference between the two methods is the cost ascertained to the inventory that is dispatched or sold by a business. In FIFO method, the basic assumption followed is that inventory which is acquired first or enters the business first will be the first to exit.

Which is a better method LIFO or FIFO?

FIFO assumes that cheaper items are sold first, generating a higher profit than LIFO. However, when the more expensive items are sold in later months, profit is lower. LIFO generates lower profits in early periods and more profit in later months. FIFO is the easier method to use, and most businesses stick with the FIFO method.

How to make a FIFO formula in Excel?

Learn Excel: how to make a fifo formula in exce

- The value of what you have left + value of the newly received stock is your total cost. ...

- How To Enter A Formula Into An Excel Spreadsheet Youtube Excel Spreadsheets Excel Math Formulas . ...

- how to make a fifo formula in excel. how to make sales report in excel with formula. ...

- Love Microsoft Excel? This clip contains a tip that just might induce you to. ...

What are the disadvantages of the FIFO accounting method?

FIFO, Average Cost ... It is possible for some investors to use the average cost method of accounting, which averages the cost basis for all shares in the portfolio, and taxable gains are ...

What is FIFO method with example?

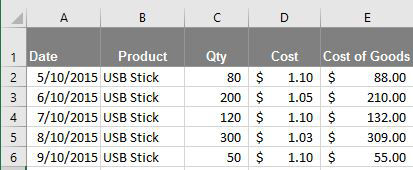

Example of FIFO Imagine if a company purchased 100 items for $10 each, then later purchased 100 more items for $15 each. Then, the company sold 60 items. Under the FIFO method, the cost of goods sold for each of the 60 items is $10/unit because the first goods purchased are the first goods sold.

How do you calculate closing inventory using FIFO?

According to the FIFO method, the first units are sold first, and the calculation uses the newest units. So, the ending inventory would be 1,500 x 10 = 15,000, since $10 was the cost of the newest units purchased. The ending inventory for Harod's company would be $15,000.

How do you calculate cost of goods sold using the FIFO periodic inventory method?

2:024:57FIFO Periodic Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipSo then the next 20 units are gonna come out of this 30 from January 6 purchase. So that's 20 unitsMoreSo then the next 20 units are gonna come out of this 30 from January 6 purchase. So that's 20 units at $40 a unit. So we add those together and that gives us $1,500. As our cost of goods sold.

How do you calculate cost per unit using FIFO?

0:047:52Cost Per Equivalent Unit, FIFO Method, Part 1 - YouTubeYouTubeStart of suggested clipEnd of suggested clipUsing the FIFO method. So the first thing we need to know is the number of equivalent units ofMoreUsing the FIFO method. So the first thing we need to know is the number of equivalent units of production. Which. I'll just abbreviate here is EU. And so we're going to be calculating.

How do you calculate inventory order?

Take the average number of days (lead time) between ordering items and having these items ready for sale. Multiply this by your average daily sales volume over the past month/quarter/year. Then add your safety stock number.

How do you calculate beginning inventory and ending inventory?

The beginning inventory formula is simple:Beginning inventory = Cost of goods sold + Ending inventory – Purchases.COGS = (Previous accounting period beginning inventory + previous accounting period purchases) – previous accounting period ending inventory.More items...•

How do you calculate FIFO and LIFO periodic?

1:334:41LIFO Periodic Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipSo cost of goods sold is gonna be 25. At $50 a unit and 15 at $40 a unit under LIFO with theMoreSo cost of goods sold is gonna be 25. At $50 a unit and 15 at $40 a unit under LIFO with the periodic method that's gonna be the cost of goods sold.

How do you calculate gross profit in FIFO?

3:076:09Gross Profit, cost of goods sold and ending inventory FIFO - YouTubeYouTubeStart of suggested clipEnd of suggested clipFor $24 each that our cost was $24 in them. So four times 24 is 96 dollars okay and then we made aMoreFor $24 each that our cost was $24 in them. So four times 24 is 96 dollars okay and then we made a sale. Here.

How does FIFO costing work?

What is FIFO costing? In simplest terms, FIFO (first-in, first-out) costing allows you to track the cost of an item/SKU based on its cost at purchase order receipt, and apply this cost against each shipment of the item until the receipt quantity is exhausted.

How do you calculate start and finish?

The materials costs consisted of $30,000 in beginning inventory and $88,000 incurred during the month, for a total of $118,000....MCQ – Process Costing.Beginning WIP10,000 units x 100%10,000Started and completed75,000 units x 100%75,000Ending WIP5,000 units x 100%5,000Weighted-average EUP for materials90,000

What does FIFO mean in accounting?

FIFO stands for “First-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company’s inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation.

Why is FIFO preferred?

The advantages to the FIFO method are as follows: The method is easy to understand, universally accepted and trusted. FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first).

Why is the LIFO method understated?

The value of remaining inventory, assuming it is not-perishable, is also understated with the LIFO method because the business is going by the older costs to acquire or manufacture that product. That older inventory may, in fact, stay on the books forever. Investors and banking institutions value FIFO because it is a transparent method ...

Why do investors value FIFO?

Investors and banking institutions value FIFO because it is a transparent method of calculating cost of goods sold. It is also easier for management when it comes to bookkeeping, because of its simplicity.

Is FIFO overstating profit?

A company also needs to be careful with the FIFO method in that it is not overstating profit. This can happen when product costs rise and those later numbers are used in the cost of goods calculation, instead of the actual costs.

Is the FIFO method legal?

Both are legal although the LIFO method is often frowned upon because bookkeeping is far more complex and the method is easy to manipulate.

What is FIFO expense?

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

What is the benefit of using FIFO?

1. Better valuation of inventory . By using FIFO, the balance sheet shows a better approximation of the market value of inventory. The latest costs for manufacturing or acquiring the inventory are reflected in inventory, and therefore, the balance sheet reflects the approximate current market value.

Can you use LIFO in Canada?

Therefore, we can see that the balances for COGS and inventory depend on the inventory valuation method. For income tax purposes in Canada, companies are not permitted to use LIFO. However, US companies are able to use FIFO or LIFO.

Why use LIFO method?

For some companies, there are benefits to using the LIFO method for inventory costing. For example, those companies that sell goods that frequently increase in price might use LIFO to achieve a reduction in taxes owed.

What is the last in first out method?

Last in, first out (LIFO) is another inventory costing method a company can use to value the cost of goods sold. This method is the opposite of FIFO. Instead of selling its oldest inventory first, companies that use the LIFO method sell its newest inventory first. Under this scenario, the last item in is the first item out.

Is FIFO a good method for calculating COGS?

FIFO is a good method for calculating COGS in a business with fluctuating inventory costs. While the LIFO inventory valuation method is accepted in the United States, it is considered controversial and prohibited by the International Financial Reporting Standards (IFRS).

Is FIFO cash flow assumption accurate?

While an actual sales pattern may not follow the FIFO cash flow assumption exactly, it is still an accurate method for determining COGS and allowed by both generally accepted accounting principles (GAAP) and International Financial Reporting Standards (IFRS).

What is the difference between LIFO and FIFO?

Under FIFO, the cost of goods sold will be lower and the closing inventory will be higher. However, in times of falling prices, the opposite will hold. 2 . FIFO is the default method of determining inventory value.

What is FIFO in 2021?

Updated February 07, 2021. FIFO is one of several ways to calculate the cost of inventory in a business. The other common inventory calculation methods are LIFO (last-in, first-out) and average cost. FIFO, which stands for "first-in, first-out," is an inventory costing method that assumes that the first items placed in inventory are the first sold.

First In First Out

In accounting, First In, First Out (FIFO) is the assumption that a business issues its inventory to its customers in the order in which it has been acquired.

Example 1 (Perpetual)

Bill sells a specific model of a toaster on his website for $12 apiece.

FIFO: Periodic Vs. Perpetual

The example above shows how a perpetual inventory system works when applying the FIFO method.

Example 2 (Periodic)

In the first example, we worked out the value of ending inventory using the FIFO perpetual system at $92.

How to determine inventory cost?

As inventory is usually purchased at different rates (or manufactured at different costs) over an accounting period, there is a need to determine what cost needs to be assigned to inventory. For instance, if a company purchased inventory three times in a year at $50, $60 and $70, what cost must be attributed to inventory at the year end? Inventory cost at the end of an accounting period may be determined in the following ways: 1 First In First Out (FIFO) 2 Last In First Out (LIFO) 3 Average Cost Method (AVCO) 4 Actual Unit Cost Method

How is the cost of inventory sold determined?

Theoretically, the cost of inventory sold could be determined in two ways. One is the standard way in which purchases during the period are adjusted for movements in inventory. The second way could be to adjust purchases and sales of inventory in the inventory ledger itself.

Fifo and Lifo

What do the accountancy terms FIFO and LIFO mean? The methods FIFO (First In First Out) and LIFO (Last In First Out) define methods used to gather inventory units and determine the Cost of Goods Sold (COGS).

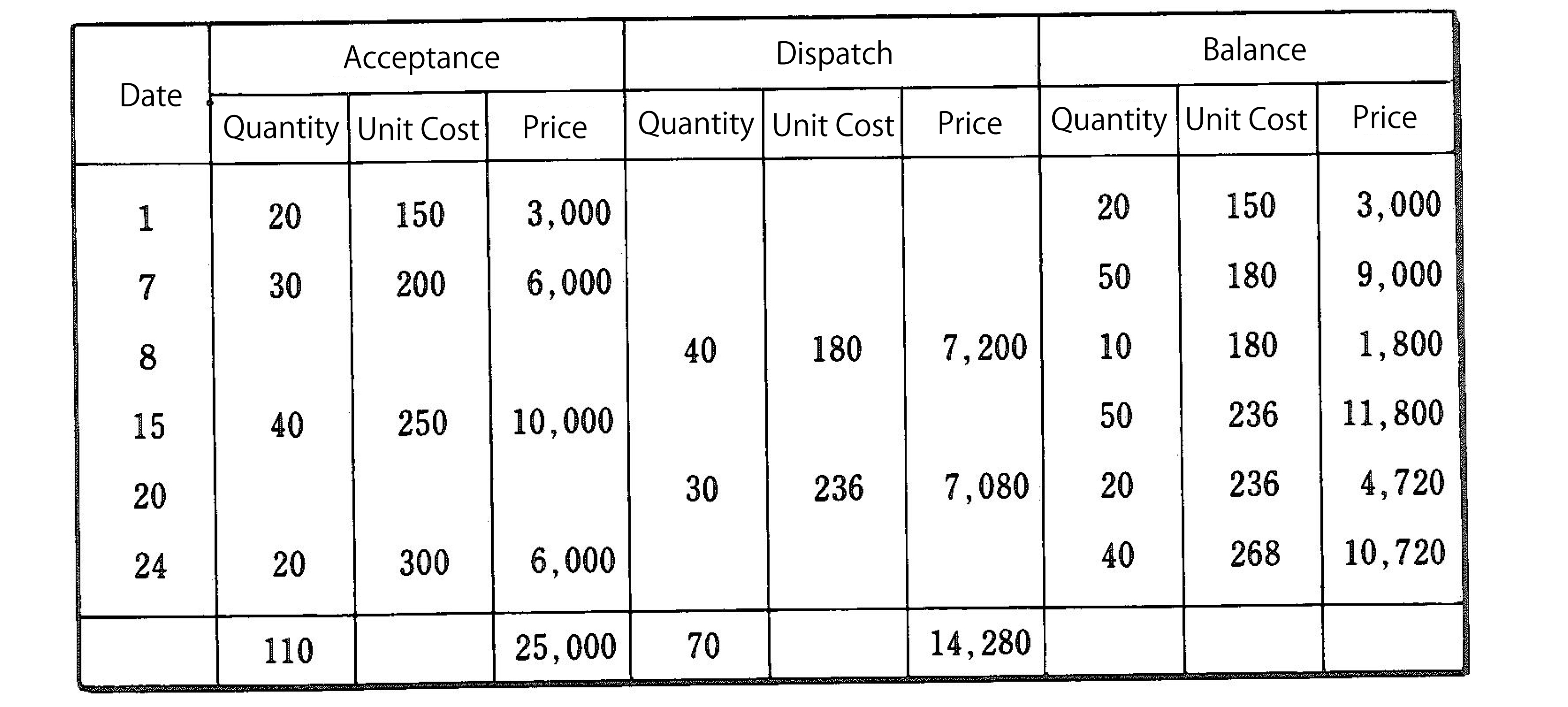

How to calculate FIFO and LIFO?

Consider that there is a watch manufacturing company that gets its units for the last 6 months as follows.

Fifo vs Lifo

If you have a look at the cost of COGS in LIFO, it is more than COGS in FIFO because the order in which the units have been consumed is not the same. In this example as well, we needed to determine the COGS of 250 units.

Ending Inventory

It is the actual amount of products that are available for sale at the end of an auditing period.

References

Business News Daily. (2020, August 28). FIFO vs LIFO: What Is the Difference?

What is FIFO in accounting?

The company makes a physical count at the end of each accounting period to find the number of units in ending inventory. The company then applies first-in, first-out (FIFO) method to compute the cost of ending inventory.

What is FIFO in inventory?

First-in, first-out (FIFO) method in periodic inventory system. Under first-in, first-out (FIFO) method, the costs are chronologically charged to cost of goods sold (COGS) i.e., the first costs incurred are first costs charged to cost of goods sold (COGS).

How to calculate cost of goods sold?

Formula method: Under formula method, the cost of goods sold would be computed as follows: Cost of goods sold = Cost of units in beginning inventory + Cost of units purchased during the period – Cost of units in ending inventory.

Example of First-In, First-Out

- Company A reported beginning inventories of 100 units at $2/unit. Also, the company made purchases of: 1. 100 units @ $3/unit 2. 100 units @ $4/unit 3. 100 units @ $5/unit If the company sold 250 units, the order of cost expenses would be as follows: As illustrated above, the cost of goods sold (COGS)Cost of Goods Sold (COGS)Cost of Goods Sold (COG...

FIFO vs. LIFO

- To reiterate, FIFO expenses the oldest inventories first. In the following example, we will compare FIFO to LIFO (last in first out)Last-In First-Out (LIFO)The Last-in First-out (LIFO) method of inventory valuation is based on the practice of assets produced or acquired last being the first to be. LIFO expenses the most recent costs first. Consider the same example above. Recall that un…

Impact of FIFO Inventory valuation Method on Financial Statements

- Recall the comparison example of First-In First-Out and LIFO. The two methods yield different inventory and COGS. Now it is important to consider the impact of using FIFO on a company’s financial statements?

Key Takeaways from First-In First-Out

- FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold.

- It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system.

- It provides a poor matching of revenue with expenses.

Related Reading

- CFI is a global provider of financial analyst training and career advancement for finance professionals, including the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll t…