How to determine which shares to sell, FIFO or LIFO?

How to Determine Which Shares to Sell, FIFO or LIFO

- FIFO vs LIFO Stock Trades. The first-in, first-out method is the default way to decide which shares to sell. ...

- Tell Your Broker. If you plan to use any method besides FIFO, including LIFO, you must specifically direct your broker as to which shares to sell so that your taxes ...

- 2018 Tax Law Changes. ...

- 2017 Tax Law. ...

How do companies report switching from LIFO to FIFO?

Your Top Offers

- FIFO vs. LIFO. ...

- Retrospective vs. Prospective. ...

- Change in Inventory Valuation Method Disclosure Requirements. Financial statements are required to disclose all significant changes in accounting policies. ...

- Federal Tax Changes. ...

What type of business would use LIFO?

- specific identification method

- FIFO

- weighted average method

How would FIFO and LIFO affect the income taxes paid?

The main difference between LIFO and FIFO is based on the assertion that the most recent inventory purchased is usually the most expensive. If that assertion is accurate, using LIFO will result in a higher cost of goods sold and less profit, which also directly affects the amount of taxes you’ll have to pay. What is LIFO?

Do companies prefer LIFO or FIFO?

From a tax perspective, FIFO is more advantageous for businesses with steady product prices, while LIFO is better for businesses with rising product prices.

What percent of companies use LIFO?

The dollar amount of reported LIFO inventories, as a percentage of total reported corporate inventories, declined from 23.7 percent in 1998 to 13.3 percent in 2011, and since then has risen to 14.5 percent.

Do most companies use LIFO?

Since most businesses don't mostly carry expensive items or commodities, most businesses use LIFO or FIFO inventory accounting. Under FIFO the assumption is that the oldest inventory is used first.

Is FIFO the most common?

FIFO is the most common accounting method.

Does Nike use FIFO or LIFO?

Inventories are valued on a Ñrst-in, Ñrst-out (FIFO) basis. During the year ended May 31, 1999, the Company changed its method of determining cost for substantially all of its U.S. inventories from last-in, Ñrst-out (LIFO) to FIFO. See Note 11.

Does Apple use LIFO or FIFO?

Apple uses FIFO Following the FIFO model, Apple sells the units of its older models first.

What inventory method do most companies use?

First-In, First-Out (FIFO) The FIFO method is the standard inventory method for most companies. FIFO gives a lower-cost inventory because of inflation; lower-cost items are usually older.

What is the most common inventory method?

The FIFO valuation methodFirst-In, First-Out (FIFO) The FIFO valuation method is the most commonly used inventory valuation method as most of the companies sell their products in the same order in which they purchase it.

What type of companies use FIFO?

Many companies that sell perishable commodities such as food or flowers use FIFO inventory tracking. Given that inventory has a limited shelf life in these industries, the FIFO method reduces losses.

Why is LIFO so popular?

The biggest benefit of LIFO is a tax advantage. During times of inflation, LIFO results in a higher cost of goods sold and a lower balance of remaining inventory. A higher cost of goods sold means lower net income, which results in a smaller tax liability.

What companies use LIFO?

Here are some of the industries that often use the LIFO method: Automotive industries when needing to quickly ship. Petroleum-based production companies. Pharmaceutical industries with some products.

Why do companies use LIFO?

The primary reason that companies choose to use an LIFO inventory method is that when you account for your inventory using the “last in, first out” method, you report lower profits than if you adopted a “first in, first out” method of inventory, known commonly as FIFO.

What is FIFO in inventory?

First-In, First-Out (FIFO) Under FIFO, it's assumed that the inventory that is the oldest is being sold first. The FIFO method is the standard inventory method for most companies. FIFO gives a lower-cost inventory because of inflation; lower-cost items are usually older.

How long does it take to change to LIFO?

If you filed your business tax return for the year when you want to use LIFO, you can make the election by filing an amended tax return within 12 months of the date you filed the original return. 8. Once you change to the LIFO method, you can't go back to FIFO unless the IRS gives you specific permission.

What is less inventory at the end of the year?

Less inventory at the end of the year. 1. The cost of beginning and ending inventory is an important factor in COGS. To determine this cost, the value (cost) of inventory that is sold during the year must be calculated by some reasonable method that is common to all businesses.

Is LIFO costing better than FIFO costing?

If your inventory costs are going up, or are likely to increase, LIFO costing may be better because the higher cost items (the ones purchased or made last) are considered to be sold. This results in higher costs and lower profits. If the opposite is true, and your inventory costs are going down, FIFO costing might be better.

Does the IRS like LIFO?

As you might guess, the IRS doesn't like LIFO valuation, because it usually results in lower profits (less taxable income). But the IRS does allow businesses to use LIFO accounting, requiring an application, on Form 970 . If your business decides to change from FIFO to LIFO, you must file an application to use LIFO by sending Form 970 to the IRS. ...

What is the FIFO method?

They can use the first-in, first-out (FIFO) method, the last-in, first-out method (LIFO), or they can calculate inventory costs by using the average cost method. 1 By comparison, companies reporting under International Financial Reporting Standards (IFRS) are required to use FIFO only. 2 . LIFO has been the subject of some budget controversy in ...

Why did Obama ban LIFO?

In 2014, the administration of President Barack Obama sought to ban LIFO, which it said allowed companies to make their incomes appear smaller for the purposes of taxation. 3 Proponents for keeping LIFO say repeal would increase the cost of capital for companies and have negative consequences for economic growth. 4 .

Why do companies use LIFO?

A final reason that companies elect to use LIFO is that there are fewer inventory write-downs under LIFO during times of inflation. An inventory write-down occurs when the inventory is deemed to have decreased in price below its carrying value .

What is LIFO for businesses?

Businesses that sell products that rise in price every year benefit from using LIFO. When prices are rising, a business that uses LIFO can better match their revenues to their latest costs.

Why is LIFO so controversial?

The higher COGS under LIFO decreases net profits and thu s creates a lower tax bill for One Cup. This is why LIFO is controversial; opponents argue that during times of inflation, LIFO grants an unfair tax holiday for companies. In response, proponents claim that any tax savings experienced by the firm are reinvested and are of no real consequence to the economy. Furthermore, proponents argue that a firm's tax bill when operating under FIFO is unfair (as a result of inflation).

How does LIFO work?

How Last in, First out (LIFO) Works. Under LIFO, a business records its newest products and inventory as the first items sold. The opposite method is FIFO, where the oldest inventory is recorded as the first sold. While the business may not be literally selling the newest or oldest inventory, it uses this assumption for cost accounting purposes.

Why is LIFO used?

When prices are rising, it can be advantageous for companies to use LIFO because they can take advantage of lower taxes. Many companies that have large inventories use LIFO, such as retailers or automobile dealerships.

What is the LIFO method?

Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first . This method is banned under the International Financial Reporting Standards ...

Why do supermarkets use LIFO?

For example, many supermarkets and pharmacies use LIFO cost accounting because almost every good they stock experiences inflation. Many convenience stores—especially those that carry fuel and tobacco—elect to use LIFO because the costs of these products have risen substantially over time.

What is the difference between FIFO and LIFO?

FIFO (first in, first out) inventory management seeks to sell older products first so that the business is less likely to lose money when the products expire or become obsolete. LIFO (last in , first out) inventory management applies to nonperishable goods and uses current prices to calculate the cost of goods sold.

How are FIFO and LIFO similar?

However, they are similar in one regard: Both depend on the product remaining the same, with price being the only fluctuating element. FIFO and LIFO influence a company's earnings on paper.

Why is FIFO a good valuation method?

For businesses that need to impress investors, this becomes an ideal method of valuation, until the higher tax liability is considered. Because FIFO results in a lower recorded cost per unit, it also records a higher level of pretax earnings. And with higher profits, companies will likewise face higher taxes.

What is LIFO in accounting?

The principle of LIFO is highly dependent on how the price of goods fluctuates based on the economy . If a company holds inventory for a long time, holding on to products may prove quite advantageous in hedging profits for taxes. LIFO allows for higher after-tax earnings due to the higher cost of goods.

How does LIFO work?

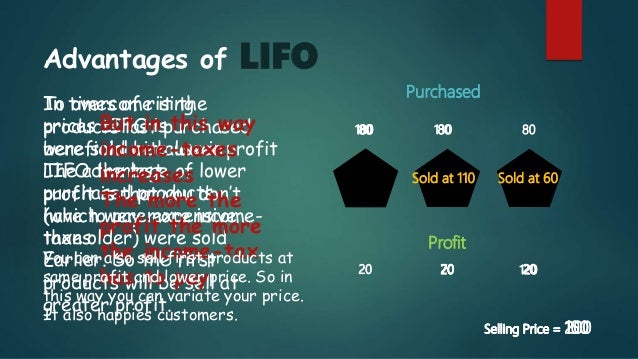

As an example of how LIFO works, suppose a website development company purchases a plugin for $30 and then sells the finished product for $50. However, several months later, that asset has increased in price to $35. When the company calculates its profits, it would use the most recent price of $35. In tax statements, it would then appear as if the company made a profit of only $15. By using LIFO, a company would appear to be making less money than it actually did and, therefore, have to report less in taxes.

Is LIFO a FIFO?

This increases the comparability of LIFO and FIFO firms. In general, both U.S. and international standards are moving away from LIFO. Many U.S.-based companies have switched to FIFO, and some companies still use LIFO within the United States as a form of inventory management but translate it to FIFO for tax reporting.

Does LIFO have to be converted to FIFO?

Because of the current discrepancy, however, U.S.-based companies that use LIFO must convert their statements to FIFO in the footnotes of their financial statements. This difference is known as the LIFO reserve and is calculated between the cost of goods sold under LIFO and FIFO, Melwani said.

Why use FIFO?

When using FIFO, you’ll have to more accurately display what you paid for the oldest inventory, whether that be more or less . Profits will often seem higher when using FIFO, which is more attractive to investors.

Why is FIFO important?

The FIFO method will help you to maximize profits on your inventory without having to risk as many variables. As you’d probably guess, based on the pros and cons, FIFO makes sense for many more business models and is seen to be more of an industry standard.

What is the opposite of LIFO?

The FIFO method is opposite to LIFO in that, the items that have been in your warehouse the longest would be sold first. This is a standard method at grocery stores and other similar suppliers where products will deteriorate or expire with age.

What is the LIFO method?

The LIFO method uses the practice of taking the items that were last received into your warehouse and selling them or shipping them first. So, selling or shipping the newest, most recent items first. When using the LIFO method, you’ll more easily be able to manipulate financial statements and tax documents in your favor.

Is LIFO compatible with IFRS?

Not compatible with the IFRS (International Financial Reporting Standards) accounting method. Lower earnings which can discourage investors. As you can see, there are quite a few variables that determine whether your warehouse will see success using the LIFO to manage inventory within the warehouse.

Why use FIFO instead of LIFO?

Reason for Using FIFO Instead of LIFO. If a U.S. corporation's cost of inventory items are continuously increasing and the corporation has been experiencing operating losses and negative taxable income, the use of FIFO means matching its oldest/lower costs with its current sales. The result is a larger gross profit and a positive operating income.

Why use LIFO?

Reason for Using LIFO. If a U.S. corporation's costs of inventory items are continuously increasing, a profitable U.S. corporation will have lower income tax payments with LIFO. This results from matching the most recent higher costs of its items to the most recent sales. (The higher cost of goods sold means lower net income ...

What is a fifo?

Definitions of FIFO and LIFO. FIFO and LIFO are two of the cost flow assumptions used by U.S. companies with inventory items. FIFO moves the first/oldest costs from inventory and reports them as the cost of goods sold and leaves the last/more recent costs in inventory. LIFO moves the latest/more recent costs from inventory and reports them as ...

Why use LIFO or FIFO?

The LIFO method for financial accounting may be used over FIFO when the cost of inventory is increasing, perhaps due to inflation. Using FIFO means the cost of a sale will be higher because the more expensive items in inventory are being sold off first.

What is the difference between FIFO and LIFO?

During periods of inflation, FIFO maximizes profits as older, cheaper inventory is used as cost of goods sold; in contrast, LIFO maximizes profits during periods of deflation. Since newest items are sold first, the oldest items may remain in the inventory for many years. Fluctuations Only the newest items remain in the inventory and ...

What is FIFO accounting?

First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last. An alternative to FIFO, LIFO is an accounting method in which assets purchased or acquired last are disposed of first.

What is LIFO reserve?

The LIFO reserve is a contra-asset or asset reduction account that companies use to adjust downward the cost of inventory carried at FIFO to LIFO. Many companies use dollarvalue LIFO, since this method applies inflation factors to “inventory pools” rather than adjusting individual inventory items.

What does FIFO mean in inventory?

FIFO stands for First In, First Out, which means the goods that are unsold are the ones that were most recently added to the inventory. Conversely, LIFO is Last In, First Out, which means goods most recently added to the inventory are sold first so the unsold goods are ones that were added to the inventory the earliest.

Why does LIFO show the largest cost of goods sold?

During periods of inflation, LIFO shows the largest cost of goods sold of any of the costing methods because the newest costs charged to cost of goods sold are also the highest costs.

What is the LIFO method?

The LIFO method assumes that the most recent products added to a company’s inventory have been sold first. The costs paid for those recent products are the ones used in the calculation. The “Last In, First Out” inventory method has been hotly debated at the federal level.

Why use LIFO?

In the U.S., accountants often cite LIFO as the preferred method when products' costs are changing. The reason is the matching of the latest costs of products with the sales revenues of the current period . U.S. tax rules also allow for either FIFO or LIFO, but require that the same cost flow assumption be used on both the company's tax return ...

Does FIFO require the same cost flow assumption?

tax rules also allow for either FIFO or LIFO, but require that the same cost flow assumption be used on both the company's tax return and on the company's financial statements.

What Is FIFO, and How Does It Work?

What Is LIFO, and How Does It Work?

- The last in, first out method of inventory entails using current prices to calculate the cost of goods sold, as opposed to using what was paid for the inventory already in stock. If the price of such goods has increased since the initial purchase, the cost of goods sold will be higher and thereby reduce profits and tax burdens. Nonperishable commodities – like petroleum, metals and chemi…

FIFO and LIFO Similarities and Differences

- FIFO and LIFO are quite different inventory management techniques. However, they are similar in one regard: Both depend on the product remaining the same, with price being the only fluctuating element. FIFO and LIFO influence a company’s earnings on paper. FIFO is most successful when used in an industry in which the price of a product remains stea...

Restrictions on The Use of LIFO

- LIFO is banned by International Financial Reporting Standards (IFRS), a set of common rules for accountants who work across international borders. While many nations have adopted IFRS, the United States still operates under the guidelines of generally accepted accounting principles (GAAP). If the United States were to ban LIFO, the country would clear an obstacle to adopting IF…