FIFO or LIFO: Which is Better?

- Rising vs. Falling Costs. ...

- Accuracy of Counting. If you want a more accurate cost, FIFO is better because it assumes that older less-costly items are most usually sold first.

- Profits and Taxes. Higher costs to a business mean a lower net income, which results in lower taxes. ...

- Selling Globally. ...

- Recordkeeping Requirements. ...

Can a company change from LIFO to FIFO?

Most companies switching from LIFO to FIFO choose to restate their historical financial statements as if the new method had been used all along. The income statement is affected from changes in cost of goods sold, and this affects all measures of earnings, such as operating income and net income. How does LIFO and FIFO affect financial statements?

Which companies use LIFO method?

To complete the election application, you will need to:

- Specify the goods to which the LIFO method will apply,

- Identify and describe the inventory method (s) you used in the prior year to value these goods, and

- Explain what goods the LIFO method will NOT be used for.

What are the disadvantages of the FIFO accounting method?

FIFO, Average Cost ... It is possible for some investors to use the average cost method of accounting, which averages the cost basis for all shares in the portfolio, and taxable gains are ...

How to calculate cost of goods sold using FIFO method?

Inputs:

- First of all, you just have to enter the quantity of each unit purchases

- Then, you have to add the quantity of the price/unit you purchased

- Also, the lifo fifo method calculator provides you with options of adding more purchases “one by one” or multiple

- Then, you have to enter the total units sold from your number of purchases

Why FIFO method is better than LIFO method?

FIFO is more likely to give accurate results. This is because calculating profit from stock is more straightforward, meaning your financial statements are easy to update, as well as saving both time and money. It also means that old stock does not get re-counted or left for so long it becomes unusable.

What are the advantages of using FIFO?

Advantages of FIFO method FIFO method saves money and time in calculating the exact cost of the inventory being sold because the cost will depend upon the most former cash flows of purchases to be used first. It is a simple concept which is easy to understand.

Is LIFO or FIFO more accurate?

FIFO is considered to be the more transparent and trusted method of calculating cost of goods sold, over LIFO.

What are the 5 main reasons for using FIFO?

5 Benefits of FIFO Warehouse StorageIncreased Warehouse Space. Goods can be packed more compactly to free up extra floor space in the warehouse.Warehouse Operations are More Streamlined. ... Keeps Stock Handling to a Minimum. ... Enhanced Quality Control. ... Warranty Control.

What are the pros and cons of FIFO?

FIFO vs. LIFO: Pros and ConsFIFOCOMPLEXITYLess complex. Minimal to no COGS fluctuation.INFLATIONLower COGS. Higher profits. Greater tax liability. Higher earnings and net worth appeal to investors.DEFLATIONHigher COGS. Lower profits. Reduced tax liability. Lower earnings and net worth may discourage investors.3 more rows

What is FIFO advantages and disadvantages?

This method is useful for materials which are subject to obsolescence and deterioration In periods of rising prices, the FIFO method produces higher profits and results in higher tax liability because lower cost is charged to production Conversely in periods of falling, prices.

Which inventory method is best?

The most popular inventory accounting method is FIFO because it typically provides the most accurate view of costs and profitability.

What are the advantages and disadvantages of FIFO and LIFO?

The companies that decide to use LIFO over FIFO most often do it for the tax advantages. However, there can also be tax liabilities. The advantages of LIFO are also its disadvantages as the only real purpose of instituting LIFO is to avoid paying higher taxes but this means profits are generally lower.

Why would a company change from LIFO to FIFO?

For this and other reasons, CPAs may be called upon to advise companies switching from LIFO to FIFO (first in, first out) or average cost. A change from LIFO to FIFO typically would increase inventory and, for both tax and financial reporting purposes, income for the year or years the adjustment is made.

Why would a company choose to use FIFO costing?

Companies must use FIFO for inventory if they are selling perishable goods such as food, which expires after a certain period of time. Companies selling products with relatively short demand cycles, such as designer fashion, also may have to pick FIFO to ensure they are not stuck with outdated styles in inventory.

Why use LIFO method?

It helps them match the latest costs of products with the sales revenue of the current period, and thus reduce tax liability.

Why is LIFO valuation not allowed?

Non-compliance with the IFRS (International Financial Reporting Standards) – The LIFO valuation method will not allow your business to operate internationally because it is banned by the IFRS due to reduced income tax figures.

What is FIFO in accounting?

FIFO – According to FIFO, or First in, First out, the oldest inventory items are sold first. As a result, the oldest cost of an item in inventory is removed. Then this cost appears on the income statement as part of the cost of goods sold. For example, a clothes store purchased 200 pairs of jeans at a cost of $ 10 per pair.

What happens if you lower your COGS?

Higher income tax liability – Lower COGS figures result in inflated profits. This can lead to a higher income tax expense, reducing the cash flow of your organization and potentially weakening the financial position of the business for the next accounting period.

Does FIFO increase inventory?

Increased inventory value and net income – During inflation, FIFO increases the value of your inventory, because the inventory that you’re buying next is more expensive. It also increases your net income, because your older items with lower COGS would now be a smaller percentage of your sales price.

Does LIFO comply with matching principle?

Compliance with the matching principle – Unlike FIFO, LIFO complies with the matching principle, because the revenues and costs are recorded in the same period. As a result, both revenue and costs are recorded with the most recent values.

What is FIFO in inventory?

First-In, First-Out (FIFO) Under FIFO, it's assumed that the inventory that is the oldest is being sold first. The FIFO method is the standard inventory method for most companies. FIFO gives a lower-cost inventory because of inflation; lower-cost items are usually older.

How long does it take to change to LIFO?

If you filed your business tax return for the year when you want to use LIFO, you can make the election by filing an amended tax return within 12 months of the date you filed the original return. 8. Once you change to the LIFO method, you can't go back to FIFO unless the IRS gives you specific permission.

What is less inventory at the end of the year?

Less inventory at the end of the year. 1. The cost of beginning and ending inventory is an important factor in COGS. To determine this cost, the value (cost) of inventory that is sold during the year must be calculated by some reasonable method that is common to all businesses.

Is LIFO costing better than FIFO costing?

If your inventory costs are going up, or are likely to increase, LIFO costing may be better because the higher cost items (the ones purchased or made last) are considered to be sold. This results in higher costs and lower profits. If the opposite is true, and your inventory costs are going down, FIFO costing might be better.

Does the IRS like LIFO?

As you might guess, the IRS doesn't like LIFO valuation, because it usually results in lower profits (less taxable income). But the IRS does allow businesses to use LIFO accounting, requiring an application, on Form 970 . If your business decides to change from FIFO to LIFO, you must file an application to use LIFO by sending Form 970 to the IRS. ...

What is FIFO vs LIFO?

FIFO is a more realistic and logical approach of inventory valuation compared to LIFO. There is a risk of stocks, getting obsolete and outdated in case of LIFO, as goods are used from old stock, this risk can be reduced if FIFO is used. Unlike LIFO, record maintenance is easier in FIFO, as several layering is less.

Why use LIFO method?

So ultimately, the benefit of using the LIFO method for a company is that it can report a lower Net Income and hence defer its tax liabilities during the times of high inflation.

What is FIFO in accounting?

FIFO is the globally and widely used method for inventory valuation. While US GAAP allows adopting LIFO as well as FIFO, but in the international scenarios, FIFO is widely used, and IFRS restricts the use of LIFO for inventory valuation. Under LIFO, stock in hand represents the oldest stock, while in FIFO, stock in hand represents the latest stock.

Why is the LIFO method not attractive?

Investment potential. Using the LIFO method may not attract potential investors, as the use of LIFO leads to lower net income. Using the FIFO method helps the investors to understand the current scenario. It helps to attract investors.

What does LIFO mean in stock?

LIFO stands for Last In, First Out, which implies that the inventory which was added last to the stock will be removed from the stock first. So the inventory will leave the stock in an order reverse of that in which it was added to the stock.

What happens if you use LIFO?

If LIFO is used, only old inventory will remain in stock, and its purchase price will have a lesser chance of going below its carrying value. Carrying Value Carrying value is the book value of assets in a company's balance sheet, computed as the original cost less accumulated depreciation/impairments.

Is inventory expensed the same as FIFO?

Hence, whether you use the LIFO method or FIFO method, the value of the inventory expensed or even that in stock will also come out to be the same in any case. But since inflation is a reality, the value of inventory comes out to be something when we use FIFO, and it comes out to be something else when we use LIFO.

Why are FIFO profits more accurate?

Although this may mean less tax for a company to pay under LIFO, it also means stated profits with FIFO are much more accurate because older inventory reflects the actual costs of that inventory. If profits are naturally high under FIFO, then the company becomes that much more attractive to investors.

What is FIFO in accounting?

FIFO and LIFO are methods used in the cost of goods sold calculation. FIFO (“First-In, First-Out”) assumes that the oldest products in a company’s inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company’s inventory have been sold first ...

What is LIFO reserve?

The LIFO reserve is the amount by which a company’s taxable income has been deferred, as compared to the FIFO method. The remaining unsold 350 televisions will be accounted for in “inventory”.

Is LIFO more attractive than FIFO?

You can see how for Ted, the LIFO method may be more attractive than FIFO. This is because the LIFO number reflects a higher inventory cost, meaning less profit and less taxes to pay at tax time. The LIFO reserve in this example is $31,250.

Is LIFO legal in the US?

Under GAAP, LIFO is legal. Outside the United States, LIFO is not permitted as an accounting practice. This is why you’ll see some American companies use the LIFO method on their financial statements, and switch to FIFO for their international operations.

Why use LIFO over FIFO?

The advantages of LIFO are also its disadvantages as the only real purpose of instituting LIFO is to avoid paying higher taxes but this means profits are generally lower.

Why is LIFO so hard to find investors?

2. Because of LIFO’s generally lower reported profits, businesses utilizing this valuation of inventory can have a harder time finding investors. Individuals and businesses looking to invest their money are usually looking for companies that show substantial profit growth over a period of time.

What is FIFO in inventory management?

FIFO. The first in first out method of inventory management explains the order in which inventory is purchased and then sold. When a business utilizes the FIFO method, they sell the products that they received first before selling the products they received last.

What are the advantages and disadvantages of LIFO?

Like mentioned above, LIFO most often means lower profits for the company, but when you report lower profits, you don’t have to pay as many income taxes. This allows the business to have more cash-in-hand to use for investment opportunities or to purchase more inventory. Disadvantages.

What happens when a company uses FIFO?

When companies use FIFO they will constantly have an updated reflection of the current market prices for the items in their inventory. This happens as older products are taken from the inventory stock to be sold, the newer inventory is left on the books for the end of the month.

Why do accountants have to write off obsolete inventory?

Because FIFO makes sure that the oldest items in stock are used or sold before they are deemed obsolete companies can save money. 2.

Why do companies use FIFO or LIFO?

Most companies naturally prefer the FIFO inventory accounting method over LIFO because there is typically no valid reason to use recent inventory first, while leaving older inventory to age on the shelf. This is particularly true of perishable items, and items that rapidly become obsolete.

Why is LIFO important?

LIFO, on the other hand, is only strategically valuable during times of inflation, as goods sold first are also typically the most expensive. This increases the cost of goods sold, and reduces profits, which also reduces income tax liability.

What is LIFO accounting?

Ultimately, the choice between FIFO and LIFO inventory accounting methods will be based on the needs of your business, and how it operates.

What is a LIFO?

LIFO and FIFO are the most common methods of inventory valuation for product-oriented businesses. Though each has its pros and cons, an understanding of how FIFO and LIFO work with your inventory accounting system will help you decide which method is best for your business.

What is FIFO in inventory?

The first in, first out (FIFO) inventory management system is most commonly used by businesses carrying physical inventory, and operates under the assumption that the first items added to inventory will be the first ones sold. Conversely, LIFO assumes the last items placed in inventory will be the first to be sold.

Why do pharmacies use LIFO?

LIFO can appeal to companies looking to reduce their tax liability, and may be a better choice in certain scenarios, such as: businesses with steeply rising costs – Supermarkets and pharmacies typically use LIFO because their products are sensitive to inflation.

What industries use LIFO?

companies that use physical LIFO – Certain industries, like lumber and mining, stack the newest inventory items on top of older ones. businesses that face inventory write-downs during inflation – Examples include the fashion and agricultural industries that carry inventory that spoils, is easily damaged, or is vulnerable to obsolescence.

What is the difference between FIFO and LIFO?

It then uses these production costs. Whilst the FIFO definition means first in, first out. In this case, the oldest products in the inventory have been sold first.

Why is LIFO good?

LIFO is beneficial for those wanting to keep tax costs down. It can work well for retail firms who want to work with trends and quickly sell items that are in fashion now. Or for places like supermarkets who want to deal with the fluctuating prices of food.

Why use LIFO method?

It’s a great method to use when stock is always changing costs, or if you have perishable goods coming in. This is because it matches the latest costs of products. However, when stock is looking old or needs shifting, it can be hard to use the LIFO method to calculate profit. For yourself, or for tax purposes.

What is the meaning of LIFO in stock?

These acronyms may sound like a couple of kid’s TV characters, but actually, they’re great ways of calculating the unit costs of goods that have been sold. The LIFO definition stands for last in, first out.

What does "less profit" mean?

Less profit does mean less tax, though. Deflation may mean less profit. – If everything is based on the last item sold, then you will not be getting as much gross profit on this item. However, if you buy an item for cheap and manage to sell it on at a higher rate, then you will be making more profit.

Does FIFO mean there is fluctuation?

There isn’t as much fluctuation. – In using a FIFO method, costs of goods tend to stay the same. It’s simple to keep track of your overall inventory balance, as well as make cost flow assumptions. Obviously, there may be times when prices change, such as with inflation and deflation.

Does inflation affect FIFO?

But, due to the natural turn over of items, FIFO is a much smoother process for record-keeping. Inflation will affect your tax. – This can work in your favor as the initial cost of inventory will be lower, whilst the selling price will be higher.

Why use FIFO instead of LIFO?

Reason for Using FIFO Instead of LIFO. If a U.S. corporation's cost of inventory items are continuously increasing and the corporation has been experiencing operating losses and negative taxable income, the use of FIFO means matching its oldest/lower costs with its current sales. The result is a larger gross profit and a positive operating income.

Why use LIFO?

Reason for Using LIFO. If a U.S. corporation's costs of inventory items are continuously increasing, a profitable U.S. corporation will have lower income tax payments with LIFO. This results from matching the most recent higher costs of its items to the most recent sales. (The higher cost of goods sold means lower net income ...

What is a fifo?

Definitions of FIFO and LIFO. FIFO and LIFO are two of the cost flow assumptions used by U.S. companies with inventory items. FIFO moves the first/oldest costs from inventory and reports them as the cost of goods sold and leaves the last/more recent costs in inventory. LIFO moves the latest/more recent costs from inventory and reports them as ...

Definitions of FIFO and LIFO Methods

LIFO vs. FIFO Example

FLFO vs. LIFO Infographics

Why Is There More Than One Method For Inventory Cost Accounting?

LIFO vs. FIFO – Which Is Preferred?

Key Differences

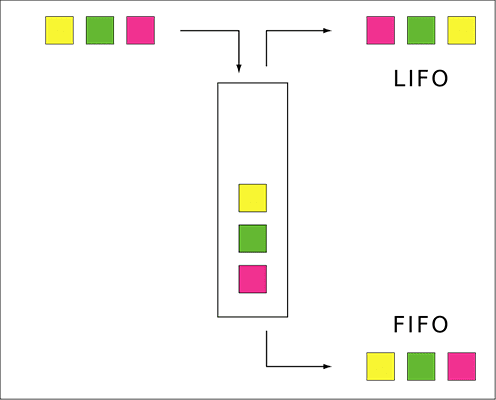

- In LIFO, the goods purchased or produced last are distributed first, and in FIFO, the goods purchased or produced first are distributed first.

- FIFO is the globally and widely used method for inventory valuation. While US GAAP allows adopting LIFO and FIFO, in international scenarios, FIFO is widely used, and IFRS restricts the use of LIFO...

- In LIFO, the goods purchased or produced last are distributed first, and in FIFO, the goods purchased or produced first are distributed first.

- FIFO is the globally and widely used method for inventory valuation. While US GAAP allows adopting LIFO and FIFO, in international scenarios, FIFO is widely used, and IFRS restricts the use of LIFO...

- Under LIFO, stock in hand represents the oldest stock, while in FIFO, stock in hand represents the latest stock.

- In an inflationary economy, using LIFO leads to lower profit figures and helps in tax savings, while using FIFO leads to higher profit and a huge tax burden.

Advantages of LIFO

Advantages of FIFO

Conclusion

Recommended Articles