The FIFO method of accounting saves time and money spent calculating the exact inventory cost of being sold because the recording of inventory is done in the same order as purchased or produced. Easy to understand.

How to determine the value of inventory using FIFO?

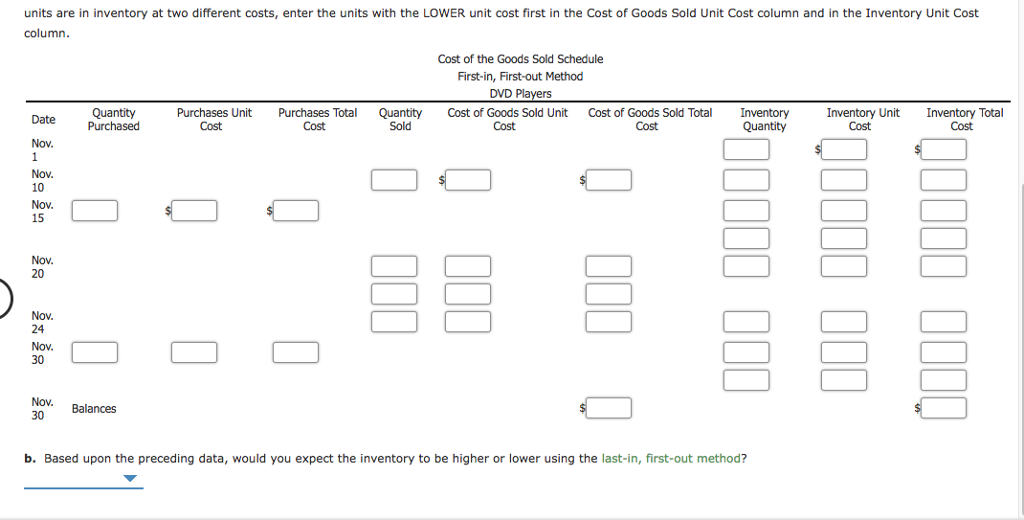

Calculate the value of the inventory sold during the period. Using FIFO, list the beginning inventory and the first shipments of inventory as being sold first. Using the earlier example with 60 ...

Which is a better method LIFO or FIFO?

FIFO assumes that cheaper items are sold first, generating a higher profit than LIFO. However, when the more expensive items are sold in later months, profit is lower. LIFO generates lower profits in early periods and more profit in later months. FIFO is the easier method to use, and most businesses stick with the FIFO method.

How to calculate cost of goods sold using FIFO method?

Inputs:

- First of all, you just have to enter the quantity of each unit purchases

- Then, you have to add the quantity of the price/unit you purchased

- Also, the lifo fifo method calculator provides you with options of adding more purchases “one by one” or multiple

- Then, you have to enter the total units sold from your number of purchases

What are the advantages and disadvantages of FIFO?

Advantages: (i) Since materials issued for production are at the original cost, the inventory reflects the current market price, (ii) Profit and Loss Account and the Balance Sheet satisfactorily represent the actual conditions, (iii) When the price level is declining, the FIFO method shows a lower profit for income tax implications, (iv) Next ...

Why is FIFO important in inventory management?

The FIFO method in warehousing and fulfillment That makes it more likely that all the stock will be sold before the expiration dates so that the store won't lose money and food won't spoil. In an eCommerce fulfillment center, businesses that use a FIFO model for physical inventory flow rotate incoming inventory.

Why is FIFO more accurate?

FIFO is more likely to give accurate results. This is because calculating profit from stock is more straightforward, meaning your financial statements are easy to update, as well as saving both time and money. It also means that old stock does not get re-counted or left for so long it becomes unusable.

Which inventory method is best and why?

The most popular inventory accounting method is FIFO because it typically provides the most accurate view of costs and profitability.

What are 5 benefits of FIFO?

5 Benefits of FIFO Warehouse StorageIncreased Warehouse Space. Goods can be packed more compactly to free up extra floor space in the warehouse.Warehouse Operations are More Streamlined. ... Keeps Stock Handling to a Minimum. ... Enhanced Quality Control. ... Warranty Control.

Why is FIFO important?

FIFO helps food establishments cycle through their stock, keeping food fresher. This constant rotation helps prevent mold and pathogen growth. When employees monitor the time food spends in storage, they improve the safety and freshness of food. FIFO can help restaurants track how quickly their food stock is used.

Which inventory valuation method is best?

As higher cost items are considered sold, it results in higher costs and lower profits. In case your inventory costs are falling, FIFO might be the best option for you. For a more accurate cost, use the FIFO method of inventory valuation as it assumes the older items that are less costly are the ones sold first.

Why would a company use FIFO instead of LIFO?

Reason for Using FIFO Instead of LIFO If a U.S. corporation's cost of inventory items are continuously increasing and the corporation has been experiencing operating losses and negative taxable income, the use of FIFO means matching its oldest/lower costs with its current sales.

What is FIFO inventory management?

FIFO (first in, first out) inventory management seeks to sell older products first so that the business is less likely to lose money when the products expire or become obsolete. LIFO (last in, first out) inventory management applies to nonperishable goods and uses current prices to calculate the cost of goods sold.

What are the advantages and disadvantages of FIFO and LIFO systems?

The companies that decide to use LIFO over FIFO most often do it for the tax advantages. However, there can also be tax liabilities. The advantages of LIFO are also its disadvantages as the only real purpose of instituting LIFO is to avoid paying higher taxes but this means profits are generally lower.

Last vs. First

First, let’s define what FIFO is by understanding what it is not. The alternative approach to inventory management and valuation is last-in-first-out, or LIFO, where the assumption is that the inventory you have purchased most recently is in turn the inventory that you will sell first.

High Transparency

While both FIFO and LIFO are sanctioned under the United States’ generally accepted accounting principles, or GAAP, opting for FIFO will make your life and the lives of your associated tax professionals much easier.

Examples of FIFO

Having explained LIFO, let’s give an example of FIFO. Let’s say now that you are in the candle business, producing and selling a variety of scented candles. In January, you buy your bulk wax, fragrances, and glass jars, paying $5000 in total for your supplies.

Putting FIFO Into Practice

FIFO management doesn’t have to exist solely on paper. It may be genuinely beneficial to sell your oldest inventory before you sell more recent arrivals. To this end, you can expand your FIFO method from the theoretical to the tangible with further organizational strategies.

Which Businesses Benefit Most From FIFO?

If you’re outside the United States where the LIFO method is not an option, the answer is “all of them.” But if you have the choice between FIFO and LIFO, there are instances in which going first-in-first-out is particularly advantageous.

Update from April 2021

It's easy for small mistakes to be made during inventory control. But these mistakes can be costly. Sometimes problems can be easily avoided with a solution as simple as color coding during inventory management. We are offer many different products for you to choose from.

What is the FIFO method?

Short for first in, first out, the FIFO method is a popular strategy for fulfilling customer orders and assigning costs to your sold inventory for accounting purposes. The first in, first out (or FIFO) method is a strategy for assigning costs to goods sold. Essentially, it means your business sells the oldest items in your inventory first—at least ...

What is FIFO accounting?

That being said, FIFO is primarily an accounting method for assigning costs to your goods sold. So you don’t necessarily have to actually sell your oldest products first—you just account for the cost of goods sold using the oldest numbers. In other words, when determining your business’s cost of goods sold (COGS), ...

What is the first in first out method?

The first in, first out (or FIFO) method is a strategy for assigning costs to goods sold. Essentially, it means your business sells the oldest items in your inventory first—at least on paper, anyway. FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual ...

Why is FIFO used?

FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual financial health. Here’s everything you need to know to decide if the FIFO method is right for you.

Is inflation a good thing?

In a FIFO system, inflation allows you to sell your items for a higher price compared to what you paid. That results in a higher profit margin for your business, which is good for your investors and your business’s overall health.

Is FIFO better than LIFO?

FIFO is also more transparent and easier to use than LIFO. LIFO systems are easy to manipulate to make it look like your business is doing better than it is. But a FIFO system provides a more accurate reflection of the current value of your inventory. This is one of the reasons why the International Financial Reporting Standards (IFRS) Foundation requires businesses to use FIFO.

Why is FIFO accounting used?

FIFO method of accounting saves time, and money spends in calculating the exact inventory cost that is being sold because the recording of inventory is done in the same order as they are purchased or produced. Easy to understand.

What are the disadvantages of FIFO accounting?

One of the biggest disadvantages of FIFO accounting method is inventory valuation during inflation, First In First Out method will result in higher profits, and thus will results in higher “Tax Liabilities” in that particular period. This may result in increased tax charges and higher tax-related cash outflows.

Which method of inventory valuation gives the most accurate calculation of the inventory and sales profit?

A business which is in the trading of perishable items generally sells the items which are purchased earliest first, FIFO method of inventory valuation generally gives the most accurate calculation of the inventory and sales profit. Other examples include retail businesses that sell foods or other products with an expiration date.

How are inventory costs reported?

Inventory costs are reported either on the balance sheet, or they are transferred to the income statement as an expense to match against sales revenue. When inventories are used up in production or are sold, their cost is transferred from the balance sheet to the income statement as cost of goods sold.

Is the first in first out method a good measure of inventory?

Use of First In First Out method is not a suitable measure of inventory in times of “ hyperinflation .”. During such times, there is no particular pattern of inflation, which may result in prices of goods to inflate drastically.

Does inflation increase operating expenses?

Normally in an inflationary environment, prices are always rising, which will cause an increase in operating expenses, but with FIFO accounting, the same inflation will cause an increase in ending inventory.

What does FIFO mean?

FIFO Meaning, Importance and Example. For any company, there are two possible inventory valuation methods, LIFO and FIFO. Where LIFO stands for last in first out, FIFO, on the other hand, stands for First in first out. In the LIFO method, you sell the latest goods first, and in FIFO, you sell the oldest inventory first.

Does FIFO always give exact cost?

Firstly as prices of the oldest stock will be used to calculate the Cost of goods sold in present times, FIFO does not always give exact cost calculations. Secondly, there is no tax benefit by using FIFO, unlike LIFO, as valuation leads to higher income tax and low cash flow.

What is FIFO in retail?

The FIFO method is typically used to manage perishable product stock, with an expiry date, with the most common being food, medicine and cosmetic products. It is also a common management method for companies that store products that may become obsolete or “go out of style” relatively quickly, such as technological products (home appliances, ...

What is the goal of FIFO?

The ultimate goal of FIFO is to achieve an excellent stock turnover in the warehouse, giving priority to the output of products that have been stored the longest and can spoil or become obsolete.

What is FIFO storage?

High-density semi-automatic storage system which uses motorised pallet shuttles that transport the load autonomously inside the racking, from the loading position to the last available position at the back. To implement the FIFO method, you must load the goods on one side and unload them on the other.

Why is FIFO a good valuation method?

For businesses that need to impress investors, this becomes an ideal method of valuation, until the higher tax liability is considered. Because FIFO results in a lower recorded cost per unit, it also records a higher level of pretax earnings. And with higher profits, companies will likewise face higher taxes.

What is the difference between FIFO and LIFO?

FIFO (first in, first out) inventory management seeks to sell older products first so that the business is less likely to lose money when the products expire or become obsolete. LIFO (last in , first out) inventory management applies to nonperishable goods and uses current prices to calculate the cost of goods sold.

How are FIFO and LIFO similar?

However, they are similar in one regard: Both depend on the product remaining the same, with price being the only fluctuating element. FIFO and LIFO influence a company's earnings on paper.

What is LIFO in accounting?

The principle of LIFO is highly dependent on how the price of goods fluctuates based on the economy . If a company holds inventory for a long time, holding on to products may prove quite advantageous in hedging profits for taxes. LIFO allows for higher after-tax earnings due to the higher cost of goods.

How does LIFO work?

As an example of how LIFO works, suppose a website development company purchases a plugin for $30 and then sells the finished product for $50. However, several months later, that asset has increased in price to $35. When the company calculates its profits, it would use the most recent price of $35. In tax statements, it would then appear as if the company made a profit of only $15. By using LIFO, a company would appear to be making less money than it actually did and, therefore, have to report less in taxes.

What is the principle of first in first out inventory?

Companies operating on the principle of first in, first out value inventory on the assumption that the first goods purchased for resale become the first goods sold. In some cases, this may not be true, as some companies stock both new and old items.

Is LIFO a FIFO?

This increases the comparability of LIFO and FIFO firms. In general, both U.S. and international standards are moving away from LIFO. Many U.S.-based companies have switched to FIFO, and some companies still use LIFO within the United States as a form of inventory management but translate it to FIFO for tax reporting.