The first in first out (FIFO

FIFO

FIFO is an acronym for first in, first out, a method for organising and manipulating a data buffer, where the oldest entry, or 'head' of the queue, is processed first. It is analogous to processing a queue with first-come, first-served behaviour: where the people leave the queue in the order in …

How to determine the value of inventory using FIFO?

Calculate the value of the inventory sold during the period. Using FIFO, list the beginning inventory and the first shipments of inventory as being sold first. Using the earlier example with 60 ...

What is FIFO inventory costing and why use it?

It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company’s inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation. How Do You Calculate FIFO? What Are the Advantages of FIFO?

What are the objectives of inventory system?

The followings are the objectives of inventory management:

- To ensure continuous supply of materials spares and finished goods so that production should not suffer at any time and the customer’s demand should also be met.

- To avoid both overstocking and under-stocking of inventory. ADVERTISEMENTS:

- To maintain investment in inventories at the optimum level as required by the operational and sales activities.

What kind of inventory system does Best Buy use?

While we definitely think Ordoro is the best inventory system overall, Upserve, Cin7, Zoho Inventory, Stitch Labs, and Fishbowl all offer excellent inventory tracking and stock management solutions for different types of businesses. And if you’re in need of a quality inventory system on a budget, inFlow Inventory is a top pick too.

Why would you use FIFO method?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

Why would a company use FIFO instead of LIFO?

Reason for Using FIFO Instead of LIFO If a U.S. corporation's cost of inventory items are continuously increasing and the corporation has been experiencing operating losses and negative taxable income, the use of FIFO means matching its oldest/lower costs with its current sales.

Why do most companies prefer to use FIFO over LIFO in inventory management?

FIFO is more likely to give accurate results. This is because calculating profit from stock is more straightforward, meaning your financial statements are easy to update, as well as saving both time and money. It also means that old stock does not get re-counted or left for so long it becomes unusable.

When FIFO method is most suitable?

LIFO is a newer inventory cost valuation technique (accepted in the 1930s), which assumes that the newest inventory is sold first. LIFO gives a higher cost to inventory....Last-In, First-Out (LIFO)FIFO vs. LIFO - A ComparisonFIFOLIFOAssumes first items in inventory sold firstAssumes last items in inventory sold first5 more rows•May 21, 2021

Which industry uses FIFO method and why?

Industries That Use FIFO Here are the industries that often use the FIFO method: Grocery Stores. When inventory is perishable or expires. Companies that need to make sure they don't have old inventory.

What company uses FIFO?

Just to name a few examples, Dell Computer (NASDAQ:DELL) uses FIFO. General Electric (NYSE:GE) uses LIFO for its U.S. inventory and FIFO for international. Teen retailer Hot Topic (NASDAQ:HOTT) uses FIFO.

Why does FIFO increase net income?

FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet. As a result, FIFO can increase net income because inventory that might be several years old–which was acquired for a lower cost–is used to value COGS.

What is meant by FIFO and why is it important to proper food storage?

FIFO is “first in first out” and simply means you need to label your food with the dates you store them, and put the older foods in front or on top so that you use them first. This system allows you to find your food quicker and use them more efficiently.

Why is FIFO accounting used?

FIFO method of accounting saves time, and money spends in calculating the exact inventory cost that is being sold because the recording of inventory is done in the same order as they are purchased or produced. Easy to understand.

What are the disadvantages of FIFO accounting?

One of the biggest disadvantages of FIFO accounting method is inventory valuation during inflation, First In First Out method will result in higher profits, and thus will results in higher “Tax Liabilities” in that particular period. This may result in increased tax charges and higher tax-related cash outflows.

Which method of inventory valuation gives the most accurate calculation of the inventory and sales profit?

A business which is in the trading of perishable items generally sells the items which are purchased earliest first, FIFO method of inventory valuation generally gives the most accurate calculation of the inventory and sales profit. Other examples include retail businesses that sell foods or other products with an expiration date.

How are inventory costs reported?

Inventory costs are reported either on the balance sheet, or they are transferred to the income statement as an expense to match against sales revenue. When inventories are used up in production or are sold, their cost is transferred from the balance sheet to the income statement as cost of goods sold.

Is the first in first out method a good measure of inventory?

Use of First In First Out method is not a suitable measure of inventory in times of “ hyperinflation .”. During such times, there is no particular pattern of inflation, which may result in prices of goods to inflate drastically.

Does inflation increase operating expenses?

Normally in an inflationary environment, prices are always rising, which will cause an increase in operating expenses, but with FIFO accounting, the same inflation will cause an increase in ending inventory.

What is the difference between LIFO and FIFO?

Under FIFO, the cost of goods sold will be lower and the closing inventory will be higher. However, in times of falling prices, the opposite will hold. 2 . FIFO is the default method of determining inventory value.

What is FIFO in 2021?

Updated February 07, 2021. FIFO is one of several ways to calculate the cost of inventory in a business. The other common inventory calculation methods are LIFO (last-in, first-out) and average cost. FIFO, which stands for "first-in, first-out," is an inventory costing method that assumes that the first items placed in inventory are the first sold.

What is specific identification?

Instead of using FIFO, some businesses use one of these other inventory costing methods : Specific identification is used when specific items can be identified. For example, the cost of antiques or collectibles, fine jewelry, or furs can be determined individually, usually through appraisals.

Is inventory cost deductible on taxes?

Like other legitimate business costs, the cost of the products you buy to resell can be deducted from your business income to reduce your taxes.

What is the benefit of using FIFO?

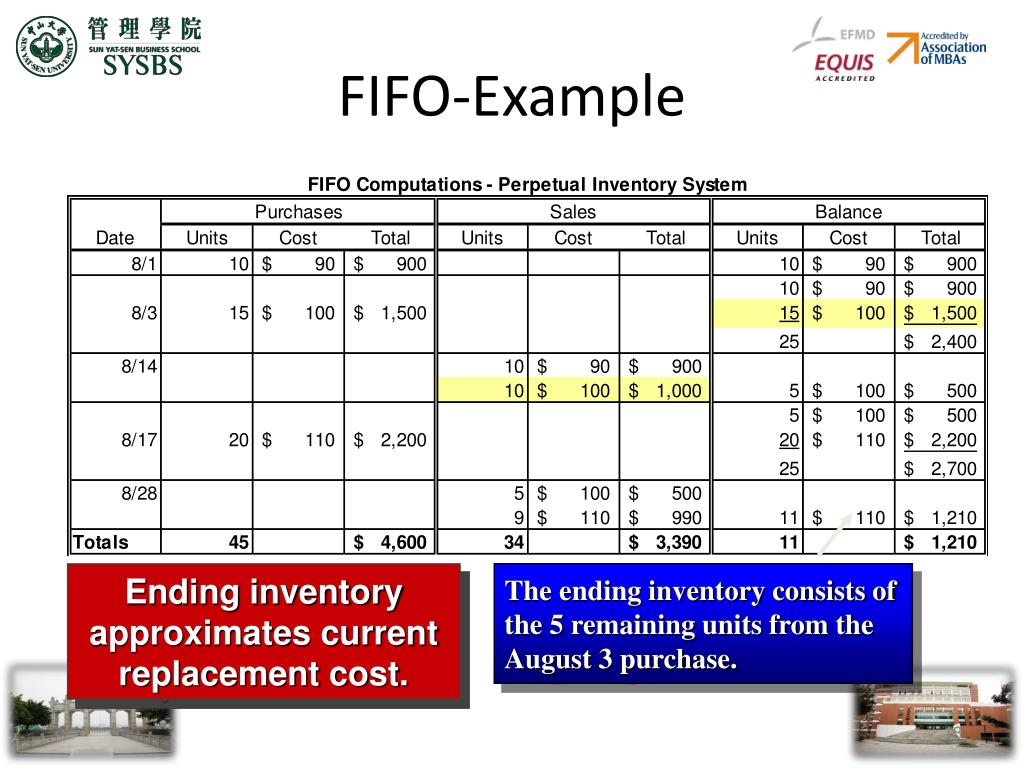

1. Better valuation of inventory . By using FIFO, the balance sheet shows a better approximation of the market value of inventory. The latest costs for manufacturing or acquiring the inventory are reflected in inventory, and therefore, the balance sheet reflects the approximate current market value.

What is FIFO expense?

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

What is the term for the days required for a business to receive inventory, sell the inventory, and collect cash from

It considers the cost of goods sold, relative to its average inventory for a year or in any a set period of time. Operating Cycle. Operating Cycle An Operating Cycle (OC) refers to the days required for a business to receive inventory, sell the inventory, and collect cash from the sale.

Can you use LIFO in Canada?

Therefore, we can see that the balances for COGS and inventory depend on the inventory valuation method. For income tax purposes in Canada, companies are not permitted to use LIFO. However, US companies are able to use FIFO or LIFO.

Why is FIFO used?

FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual financial health. Here’s everything you need to know to decide if the FIFO method is right for you.

What is FIFO accounting?

That being said, FIFO is primarily an accounting method for assigning costs to your goods sold. So you don’t necessarily have to actually sell your oldest products first—you just account for the cost of goods sold using the oldest numbers. In other words, when determining your business’s cost of goods sold (COGS), ...

What is the FIFO method?

Short for first in, first out, the FIFO method is a popular strategy for fulfilling customer orders and assigning costs to your sold inventory for accounting purposes. The first in, first out (or FIFO) method is a strategy for assigning costs to goods sold. Essentially, it means your business sells the oldest items in your inventory first—at least ...

What is the first in first out method?

The first in, first out (or FIFO) method is a strategy for assigning costs to goods sold. Essentially, it means your business sells the oldest items in your inventory first—at least on paper, anyway. FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual ...

Is FIFO better than LIFO?

FIFO is also more transparent and easier to use than LIFO. LIFO systems are easy to manipulate to make it look like your business is doing better than it is. But a FIFO system provides a more accurate reflection of the current value of your inventory. This is one of the reasons why the International Financial Reporting Standards (IFRS) Foundation requires businesses to use FIFO.

What is FIFO in business?

Unlike LIFO which is used primarily in the US, FIFO finds approval across the globe. Logical and Easy to understand: FIFO method is easy to understand and convenient to apply for almost all organizations. With a cycle that runs from selling oldest to newest, this model works well for most businesses.

What is FIFO accounting?

FIFO is a method of accounting that assumes that the goods purchased first will be sold first, and it assumes the cost of these goods sold first. FIFO is a widely accepted method across the globe, owing to its efficacy in raising profits.

How does FIFO work?

In the process, FIFO enhances the net income as the cheaper older inventory will be used to confirm the current cost of the sold goods. However, the company will have to pay higher taxes for a higher income. The FIFO approach yields a higher value of the final stock, lesser cost of goods sold, and greater gross profit during inflation.

What does FIFO mean in stock valuation?

FIFO in inventory valuation means the company sells the oldest stock first and calculates it COGS based on FIFO. Simply put, FIFO means the company sells the oldest stock first and the newest will be the last one to go for sale. This means, the cheapest stock will be sold first and the costliest stock will be the last;

Why is FIFO so efficient?

Cost-efficient and saves time: FIFO can help save a lot of time and money required to estimate the cost of the inventory being sold. This is because the cost directly depends on the foregoing cash flows of purchases that would be used first.

Why is FIFO important?

It is important to the businesses for the following reasons: Determines cost of goods sold. Provides exact numbers for budgets. Evaluating profitability.

What is FIFO approach?

The FIFO approach yields a higher value of the final stock, lesser cost of goods sold, and greater gross profit during inflation. This is because in an inflationary market when FIFO is applied, the old stock cleared first leaves behind the costlier items in the balance sheet, to be sold at a higher price in the future.

What is the advantage of FIFO method?

The first in first out (FIFO) method of inventory valuation has the following advantages for business organization: FIFO method saves money and time in calculating the exact cost of the inventory being sold because the cost will depend upon the most former cash flows of purchases to be used first.

Why does FIFO show increased gross and net profits?

This is because the “cost of sales” consists of figure of inventory and as first inventories will have less cost than recent inventories during inflation, the profits reported would be higher.

What is the first in first out method of inventory valuation?

The first in first out (FIFO) method of inventory valuation has the following advantages for business organization: 1 FIFO method saves money and time in calculating the exact cost of the inventory being sold because the cost will depend upon the most former cash flows of purchases to be used first. 2 It is a simple concept which is easy to understand. Even a layman can grab the idea with little explanation. The managers with little to no accounting information would be able to understand it easily. 3 It is a fairly practical approach to use, as sometimes it becomes difficult to identify the costs of the products sold at the point of sale and FIFO rectifies the matter. 4 It is a widely used and accepted approach of valuation which increases its comparability and consistency. 5 It makes manipulation of the income reported in financial statements difficult, as under FIFO policy there remains no vagueness about the values to be used in cost of sales figure of profit/loss statement. 6 FIFO will show increased gross and net profits in times of increasing prices of goods.#N#Cost of sales = opening stock + Purchases – closing stock#N#This is because the “cost of sales” consists of figure of inventory and as first inventories will have less cost than recent inventories during inflation, the profits reported would be higher.

What are the disadvantages of using a FIFO valuation method?

The major disadvantages of using a FIFO inventory valuation method are given below: One of the biggest disadvantage of FIFO approach of valuation for inventory/stock is that in the times of inflation it results in higher profits, due to which higher “Tax Liabilities” incur . It can result in increased cash out flows in relation to tax charges.

Why is FIFO not appropriate?

FIFO will not be an appropriate measure if the materials/goods purchased have fluctuating price patterns, because this can result in misstated profits for the same period as different costs of same goods during that same period are recorded.

Is FIFO a measure of hyperinflation?

FIFO may not be a suitable measure in times of “hyper inflation”. In such times there exist no reasonable pattern of inflation and prices of goods could inflate drastically.

What is a fifo?

Definitions of FIFO and LIFO. FIFO and LIFO are two of the cost flow assumptions used by U.S. companies with inventory items. FIFO moves the first/oldest costs from inventory and reports them as the cost of goods sold and leaves the last/more recent costs in inventory. LIFO moves the latest/more recent costs from inventory and reports them as ...

Why use FIFO instead of LIFO?

Reason for Using FIFO Instead of LIFO. If a U.S. corporation's cost of inventory items are continuously increasing and the corporation has been experiencing operating losses and negative taxable income, the use of FIFO means matching its oldest/lower costs with its current sales. The result is a larger gross profit and a positive operating income.

Why use LIFO?

Reason for Using LIFO. If a U.S. corporation's costs of inventory items are continuously increasing, a profitable U.S. corporation will have lower income tax payments with LIFO. This results from matching the most recent higher costs of its items to the most recent sales. (The higher cost of goods sold means lower net income ...

Why is FIFO a good valuation method?

For businesses that need to impress investors, this becomes an ideal method of valuation, until the higher tax liability is considered. Because FIFO results in a lower recorded cost per unit, it also records a higher level of pretax earnings. And with higher profits, companies will likewise face higher taxes.

What is the difference between FIFO and LIFO?

FIFO (first in, first out) inventory management seeks to sell older products first so that the business is less likely to lose money when the products expire or become obsolete. LIFO (last in , first out) inventory management applies to nonperishable goods and uses current prices to calculate the cost of goods sold.

How are FIFO and LIFO similar?

However, they are similar in one regard: Both depend on the product remaining the same, with price being the only fluctuating element. FIFO and LIFO influence a company's earnings on paper.

What is LIFO in accounting?

The principle of LIFO is highly dependent on how the price of goods fluctuates based on the economy . If a company holds inventory for a long time, holding on to products may prove quite advantageous in hedging profits for taxes. LIFO allows for higher after-tax earnings due to the higher cost of goods.

How does LIFO work?

As an example of how LIFO works, suppose a website development company purchases a plugin for $30 and then sells the finished product for $50. However, several months later, that asset has increased in price to $35. When the company calculates its profits, it would use the most recent price of $35. In tax statements, it would then appear as if the company made a profit of only $15. By using LIFO, a company would appear to be making less money than it actually did and, therefore, have to report less in taxes.

What is the principle of first in first out inventory?

Companies operating on the principle of first in, first out value inventory on the assumption that the first goods purchased for resale become the first goods sold. In some cases, this may not be true, as some companies stock both new and old items.

Is LIFO a FIFO?

This increases the comparability of LIFO and FIFO firms. In general, both U.S. and international standards are moving away from LIFO. Many U.S.-based companies have switched to FIFO, and some companies still use LIFO within the United States as a form of inventory management but translate it to FIFO for tax reporting.

What is FIFO accounting?

The Bottom Line. First-in, first-out (FIFO) is a popular and GAAP -approved accounting method that companies use to calculate and value their inventory —which, of course, ultimately impacts their earnings. FIFO has several strong points. But it also has drawbacks, most of them related to inflation. Let's look at the disadvantages ...

How does FIFO work?

In the manufacturing world, first-in, first-out (FIFO) is an inventory management/valuation system used during an accounting period to assign costs to a company's goods (including raw materials, goods that are in production, and finished goods that ready for sale). As its name implies, FIFO assumes the first ...

What is the opposite of FIFO?

One alternative accounting method to FIFO is LIFO ( last-in, first-out ). As the name implies, this approach is the opposite of FIFO: The LIFO method assumes goods manufactured or purchased last during a period are the first sold. So, under LIFO, the most recent products are the first to be expensed as cost of goods sold (COGS), which means the lower cost of older products will be reported as ending inventory.

What are the advantages of FIFO?

FIFO has several advantages as an accounting system. Among them: 1 It's easy to understand and use—in fact, it's one of the most widely applied accounting methods out there, both in the U.S. and abroad. 2 It makes it difficult to manipulate figures and income—the cost attached to the unit sold is always the oldest cost. 3 It aligns the expected cost flow with the logical, physical flow of goods (in our example, we sold our older muffins first, remember), offering businesses a truer picture of inventory costs. 4 It's a better indicator of the worth of the ending inventory—the balance sheet amount is likely to approximate the current market value.

Why does LIFO show the largest cost of goods sold?

During periods of inflation, LIFO shows the largest cost of goods sold because the newest costs charged to COGS are also the highest costs. The larger the cost of goods sold, the smaller the net income—and the smaller the tax liability.

What does FIFO mean?

As its name implies, FIFO assumes the first inventory manufactured or purchased during a period is sold first, while the inventory manufactured or produced last is sold last. It's kind of like milk in a grocery store. The milk the store buys first is pushed to the front of the shelf and sold first.

How does FIFO affect net income?

As a result, FIFO can increase net income and inflate profits, because inventory that might be several years old, which was acquired or produced for a lower cost is used to value your expenses.

Why Value Inventory?

Inventory Costing Explained

- The calculation of inventory cost is an important part of filing your business tax return. Like other legitimate business costs, the cost of the products you buy to resell can be deducted from your business income to reduce your taxes. At the beginning of the year, you have an initial inventory of products in various stages of completion or ready to be sold. During the year, you buy more inve…

Calculating Inventory Cost Using FIFO

- Here is how inventory cost is calculated using the FIFO method: Assume a product is made in three batches during the year. The costs and quantity of each batch are: 1. Batch 1: Quantity 2,000 pieces, Cost to produce $8000 2. Batch 2: Quantity 1,500 pieces, Cost to produce $7000 3. Batch 3: Quantity 1,700 pieces, Cost to produce $7700 4. Total produced: 5,200 pieces. Total cost $22,…

Other Costing Methods

- Instead of using FIFO, some businesses use one of these other inventory costing methods: 1. Specific identificationis used when specific items can be identified. For example, the cost of antiques or collectibles, fine jewelry, or furs can be determined individually, usually through appraisals. 2. LIFO costing ("last-in, first-out") considers the la...

Example of First-In, First-Out

FIFO vs. LIFO

- To reiterate, FIFO expenses the oldest inventories first. In the following example, we will compare FIFO to LIFO (last in first out)Last-In First-Out (LIFO)The Last-in First-out (LIFO) method of inventory valuation is based on the practice of assets produced or acquired last being the first to be. LIFO expenses the most recent costs first. Consider the same example above. Recall that un…

Impact of FIFO Inventory valuation Method on Financial Statements

- Recall the comparison example of First-In First-Out and LIFO. The two methods yield different inventory and COGS. Now it is important to consider the impact of using FIFO on a company’s financial statements?

Key Takeaways from First-In First-Out

- FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold.

- It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system.

- It provides a poor matching of revenue with expenses.

Related Reading

- CFI is a global provider of financial analyst training and career advancement for finance professionals, including the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll t…