If prices are dropping, you should not use the FIFO method. Average cost, though, is great if you are operating in a period of relatively low or no inflation. If prices are stable, you might as well use the average cost method because it's much simpler to calculate.

What is the difference between FIFO and average method?

Difference between FIFO and average costing method: 1. Primary distinction: The primary difference between the two methods is the cost ascertained to the inventory that is dispatched or sold by a business. In FIFO method, the basic assumption followed is that inventory which is acquired first or enters the business first will be the first to exit.

What is the difference between price and average cost?

- First in first out: ($19 - $20) x 1,000 shares = - $1,000

- Last in first out: ($19 - $8) x 1,000 = $11,000

- High cost: ($19 - $20) x 1,000 shares = - $1,000

- Low cost: ($19 - $8) x 1,000 = $11,000

What is the difference between FIFO vs. LIFO?

- First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method.

- Last-in, first-out (LIFO) assumes the last inventory added will be the first sold.

- Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

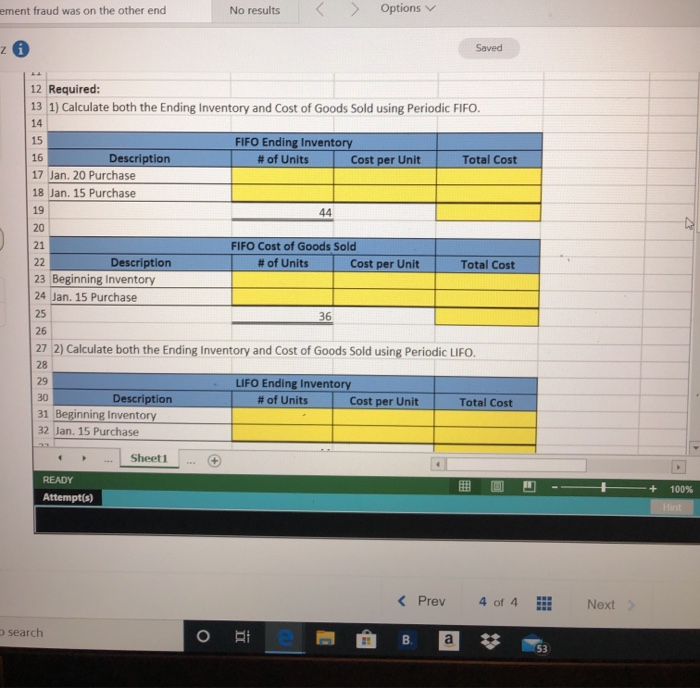

How to calculate cost of goods sold using FIFO method?

Inputs:

- First of all, you just have to enter the quantity of each unit purchases

- Then, you have to add the quantity of the price/unit you purchased

- Also, the lifo fifo method calculator provides you with options of adding more purchases “one by one” or multiple

- Then, you have to enter the total units sold from your number of purchases

Which is better FIFO LIFO or average cost?

Last In, First Out (LIFO) Generally speaking, FIFO is preferable in times of rising prices, so that the costs recorded are low, and income is higher. Contrarily, LIFO is preferable in economic climates when tax rates are high because the costs assigned will be higher and income will be lower.

Which is better FIFO or weighted average?

Impact on financial figures: In a time of decreasing inflation, the profit margins for a company will be higher under weighted average method as compared to FIFO method because the cost of goods sold will be an average figure under weighted average method which will be lower if costs are recorded under FIFO method.

Which inventory costing method is best?

FIFO in restaurants Of all inventory valuation methods, first-in, first-out is the most reliable indicator of inventory value for restaurants. Because this method corresponds inventory with its original cost, the calculated value of remaining goods is most accurate.

Why is FIFO more accurate?

FIFO is more likely to give accurate results. This is because calculating profit from stock is more straightforward, meaning your financial statements are easy to update, as well as saving both time and money. It also means that old stock does not get re-counted or left for so long it becomes unusable.

What is the main difference between weighted average cost method and FIFO method in process costing?

According to the Accounting for Management website, the main difference between the FIFO and weighted average method is in the treatment of beginning work-in-process or unfinished goods inventory. The weighted average method includes this inventory in computing process costs, while the FIFO method keeps it separate.

When would you use the FIFO method?

When Is First In, First Out (FIFO) Used? The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

Which inventory method is best for small business?

The specific identification method involves tracking every single piece of inventory by assigning it a specific cost, and adjusting the balances when inventory is sold and purchased. This method is suited to small businesses since it can provide them with more accurate numbers.

Which inventory method provides the highest profit and why?

Because FIFO has you subtract the cost of your oldest -- and therefore least expensive -- inventory from sales, your gross income is higher.

What are the pros and cons of FIFO?

FIFO vs. LIFO: Pros and ConsFIFOCOMPLEXITYLess complex. Minimal to no COGS fluctuation.INFLATIONLower COGS. Higher profits. Greater tax liability. Higher earnings and net worth appeal to investors.DEFLATIONHigher COGS. Lower profits. Reduced tax liability. Lower earnings and net worth may discourage investors.3 more rows

What are the advantages and disadvantages of FIFO method?

This method is useful for materials which are subject to obsolescence and deterioration In periods of rising prices, the FIFO method produces higher profits and results in higher tax liability because lower cost is charged to production Conversely in periods of falling, prices.

What is the disadvantage of average cost pricing?

Average Cost Method Inventory Disadvantages It means that such items are not identical and their prices can have significant differences. Can affect reporting – If the cost of a stocked item fluctuates, it can lead to errors in reported sales profit.

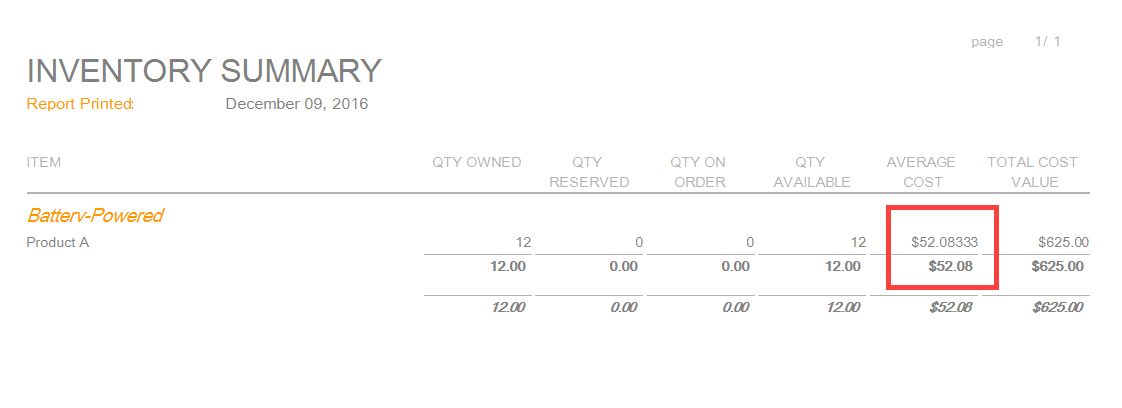

What is FIFO and average cost?

FIFO and average cost are two methods of valuing inventory. Choosing the right method for your small business could potentially allow you to book thousands of dollars in additional or earlier profits. The main distinction between the FIFO – or first-in, first-out – and average cost method is the way each accounting option calculates inventory and cost of goods sold. Using the right method can help ensure that your small business meets customer needs by having products available when customers want them while maximizing profits.

What is FIFO in warehouse?

FIFO involves selling the oldest items or those that have been in the warehouse the longest first, hence the term, first-in, first-out. The average cost method, which is sometimes called the weighted average cost, is calculated by dividing the total cost of goods in your inventory by the total number of items available for sale.

Why use the average cost method?

Average cost, though, is great if you are operating in a period of relatively low or no inflation. If prices are stable, you might as well use the average cost method because it's much simpler to calculate. However, if prices are fluctuating, either up or down, you do not want to use the average cost method because it could potentially cost you ...

Does FIFO increase profits?

In an inflationary period, FIFO leads to higher profits, because you are selling goods that cost you less when you purchased them compared to more recent items that you purchased at a higher per-unit price. The effect is the opposite in a deflationary period. If prices are dropping, you should not use the FIFO method.

Does FIFO have inventory control?

Note that with FIFO you don't have to use or resell the oldest bags of cement first: FIFO is a cost-accounting method, not an inventory-control method. You're simply taking note that you purchased X number of bags at a lower price. Average cost, by contrast, is just that – the average cost for all of the bags of cement, ...

What is the difference between average costing and FIFO costing?

The basic difference between the average costing and FIFO costing method concerns the treatment of beginning work in process inventory. The averaging method adds beginning work in process inventory costs to the preceding department’s materials, labor and factory overhead costs incurred during a period. Unit costs are determined by dividing these costs by equivalent production figures. Units and costs are transferred to the next department as one cumulative figure.

What are the disadvantages of FIFO costing?

The principle disadvantage of FIFO costing is that if several unit cost figures are used at the same time, extensive detail is required within the cost of production report. which can lead to complex procedures and even inaccuracy. Whether the extra detail yields more representative unit costs than the average costing method is debatable, especially in a firm using process costing where production is continuous and more or less uniform and appreciable fluctuations in unit costs are not expected to develop. Under such conditions, the average costing method leads to more satisfactory cost computations.

How does FIFO work?

The FIFO method retains the beginning work in process inventory cost as a separate figure. Costs necessary to complete the beginning work in process units are added to this total cost. The sum of these two costs totals is transferred to the next department. Units started and finished during the period have their own unit cost which is usually different from the completed unit cost of the units in process at the beginning of the period. The FIFO method thus separately identifies for management the current period unit cost originating in a department. Unfortunately, the costs are averaged out in the next department, resulting in a loss of much of the value associated with the use of the FIFO method.

What is the last in first out accounting method?

With this accounting technique, the costs of the oldest products will be reported as inventory. It should be understood that, although LIFO matches the most recent costs with sales on the income statement, the flow of costs does not necessarily have to match the flow of the physical units.

How to use weighted average model?

To use the weighted average model, one divides the cost of the goods that are available for sale by the number of those units still on the shelf. This calculation yields the weighted average cost per unit—a figure that can then be used to assign a cost to both ending inventory and the cost of goods sold.

What is the weighted average method?

When it comes time for businesses to account for their inventory, they typically use one of three different primary accounting methodologies: the weighted average method, the first in, first out (FIFO) method, or the last in, first out (LIFO) method. The weighted average method is most commonly employed when inventory items are so intertwined ...

Does LIFO match the flow of costs?

It should be understood that, although LIFO matches the most recent costs with sales on the income statement, the flow of costs does not necessarily have to match the flow of the physical units. Generally speaking, FIFO is preferable in times of rising prices, so that the costs recorded are low, and income is higher.

What is the difference between FIFO and FIFO?

Primary distinction: The primary difference between the two methods is the cost ascertained to the inventory that is dispatched or sold by a business. In FIFO method, the basic assumption followed is that inventory which is acquired first or enters the business first will be the first to exit.

What is the difference between FIFO and Weighted Average?

The inventory will be excluded from a business based on an average cost of all goods present in a business. FIFO method will report higher profits if inflation is rising and vice versa. Weighted average method will report higher profits if inflation is decreasing and vice versa.

What is weighted average method?

In weighted average method, the inventory will be dispatched on the basis of a weighted average of costs of all the inventory present in a business at the time of dispatch. It means that for every dispatch a new cost will be calculated and allocated to the inventory if the business follows a perpetual system of inventory valuation which is more ...

How does inventory valuation affect financial figures?

Impact on financial figures: The method of inventory valuation can affect the important financial figures of a company especially revenues and profits. In a time of rising inflation, the profits for a company will be shown increased under FIFO method as compared to weighted average method, because the goods will be sold on higher prices but ...

What is FIFO in inventory?

FIFO is an inventory valuation method in which inventory is dispatched on a first-in-first-out basis. So, inventory acquired/manufactured first is dispatched first, thus following a chronological order.

Why is FIFO important?

Inventory valuation is important because it affects many other vital figures especially those written in the financial statements of a business e.g. cost of goods sold, gross profit, the value of closing inventory mentioned in total assets etc.

Is FIFO easier to implement than weighted average?

FIFO method is easier to implement as it is easily understandable by the management of a company while the implementation of weighted average method for inventory valuation is more tedious and time consuming exercise. Although, the idea of weighted average method can be understood easily there are increased chances of errors while applying it in real life.

What is accurate FIFO?

Accurate reports – With FIFO, your balance sheet will show the exact prices you paid to purchase the inventory.

What is FIFO in accounting?

FIFO – According to FIFO, or First in, First out, the oldest inventory items are sold first. As a result, the oldest cost of an item in inventory is removed. Then this cost appears on the income statement as part of the cost of goods sold. For example, a clothes store purchased 200 pairs of jeans at a cost of $ 10 per pair.

Why is LIFO valuation not allowed?

Non-compliance with the IFRS (International Financial Reporting Standards) – The LIFO valuation method will not allow your business to operate internationally because it is banned by the IFRS due to reduced income tax figures.

What is FIFO and LIFO?

FIFO and LIFO are two methods of inventory valuation.

Why use LIFO method?

It helps them match the latest costs of products with the sales revenue of the current period, and thus reduce tax liability.

Why is it so difficult to report inventory?

Difficult reporting – If you have high inventory turnover, with prices that rise and fall over time, then your stock valuation will not reflect the prices that you actually paid. As a result, your procurement and merchandising teams will never know exactly how much money you have held up in inventory.

Is it good to have fluctuating prices?

Not good in case of fluctuating prices – If your business places many orders for products that have fluctuating prices, it can become difficult to manage the inventory and respective prices of each new shipment.