FIFOs can be used for any of these purposes:

- Crossing clock domains

- Buffering data before sending it off chip (e.g. to DRAM or SRAM)

- Buffering data for software to look at at some later time

- Storing data for later processing

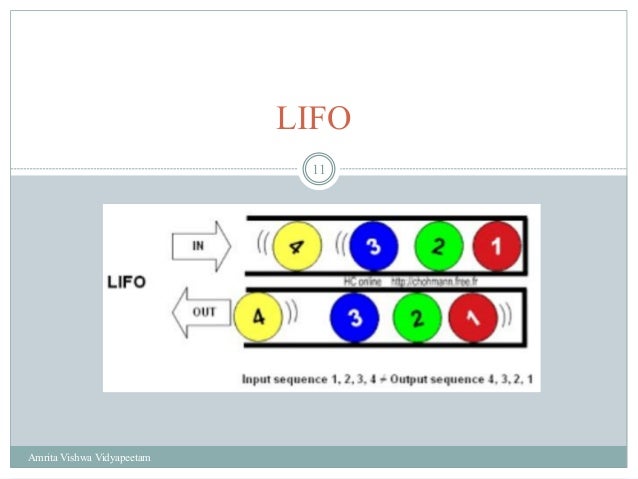

Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

Which companies use LIFO method?

To complete the election application, you will need to:

- Specify the goods to which the LIFO method will apply,

- Identify and describe the inventory method (s) you used in the prior year to value these goods, and

- Explain what goods the LIFO method will NOT be used for.

What does FIFO refer to?

Other Valuation Methods

- LIFO. The inventory valuation method opposite to FIFO is LIFO, where the last item purchased or acquired is the first item out.

- Average Cost Inventory. The average cost inventory method assigns the same cost to each item. ...

- Specific Inventory Tracing. ...

What is FIFO inventory management method and why use it?

The advantages to the FIFO method are as follows:

- The method is easy to understand, universally accepted and trusted.

- FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first). ...

- Less waste (a company truly following the FIFO method will always be moving out the oldest inventory first).

Where is FIFO and LIFO used?

FIFO (“First-In, First-Out”) assumes that the oldest products in a company's inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company's inventory have been sold first and uses those costs instead.

What is FIFO and when is it used?

FIFO stands for “First-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company's inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation.

When should a company use FIFO?

If your inventory costs are going down as time goes on, FIFO will allow you to claim a higher average cost-per-piece on newer inventory, which can help you save money on your taxes. Additionally, FIFO does not require as much recordkeeping as LIFO, because it assumes that older items are gone.

Why FIFO method is used?

FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet. As a result, FIFO can increase net income because inventory that might be several years old–which was acquired for a lower cost–is used to value COGS.

Where is LIFO used?

Last in, first out (LIFO) is a method used to account for inventory. Under LIFO, the costs of the most recent products purchased (or produced) are the first to be expensed. LIFO is used only in the United States and governed by the generally accepted accounting principles (GAAP).

What is FIFO in food service?

Foods kept frozen will remain safe, but can lose their quality over time. A great system to help with this is “FIFO.” FIFO is “first in first out” and simply means you need to label your food with the dates you store them, and put the older foods in front or on top so that you use them first.

Does Nike use FIFO?

Inventories are valued on a Ñrst-in, Ñrst-out (FIFO) basis. During the year ended May 31, 1999, the Company changed its method of determining cost for substantially all of its U.S. inventories from last-in, Ñrst-out (LIFO) to FIFO. See Note 11.

When FIFO method is most suitable?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

Do most companies use LIFO or FIFO?

Most companies prefer FIFO to LIFO because there is no valid reason for using recent inventory first, while leaving older inventory to become outdated. This is particularly true if you're selling perishable items or items that can quickly become obsolete.

Do grocery stores use LIFO or FIFO?

Companies That Benefit From LIFO Cost Accounting Virtually any industry that faces rising costs can benefit from using LIFO cost accounting. For example, many supermarkets and pharmacies use LIFO cost accounting because almost every good they stock experiences inflation.

Why is FIFO important in food?

FIFO helps food establishments cycle through their stock, keeping food fresher. This constant rotation helps prevent mold and pathogen growth. When employees monitor the time food spends in storage, they improve the safety and freshness of food. FIFO can help restaurants track how quickly their food stock is used.

What inventory method do restaurants use?

FIFO stands for first-in, first-out (FIFO), a popular principle of inventory valuation that many restaurants use. This technique assumes that the goods you purchase first are the goods you use (and sell) first.

Why is FIFO preferred?

The advantages to the FIFO method are as follows: The method is easy to understand, universally accepted and trusted. FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first).

What does FIFO mean in accounting?

FIFO stands for “First-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company’s inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation.

Why is the LIFO method understated?

The value of remaining inventory, assuming it is not-perishable, is also understated with the LIFO method because the business is going by the older costs to acquire or manufacture that product. That older inventory may, in fact, stay on the books forever. Investors and banking institutions value FIFO because it is a transparent method ...

Why do investors value FIFO?

Investors and banking institutions value FIFO because it is a transparent method of calculating cost of goods sold. It is also easier for management when it comes to bookkeeping, because of its simplicity.

Is FIFO overstating profit?

A company also needs to be careful with the FIFO method in that it is not overstating profit. This can happen when product costs rise and those later numbers are used in the cost of goods calculation, instead of the actual costs.

Is the FIFO method legal?

Both are legal although the LIFO method is often frowned upon because bookkeeping is far more complex and the method is easy to manipulate.

What is a FIFO?

FIFOs are commonly used in electronic circuits for buffering and flow control between hardware and software. In its hardware form, a FIFO primarily consists of a set of read and write pointers, storage and control logic. Storage may be static random access memory (SRAM), flip-flops, latches or any other suitable form of storage.

What is a FIFO in a network?

Communication network bridges, switches and routers used in computer networks use FIFOs to hold data packets in route to their next destination. Typically at least one FIFO structure is used per network connection.

What is a synchronous FIFO?

Synchronicity. A synchronous FIFO is a FIFO where the same clock is used for both reading and writing. An asynchronous FIFO uses different clocks for reading and writing and they can introduce metastability issues.

When was the first FIFO implemented?

The first known FIFO implemented in electronics was by Peter Alfke in 1969 at Fairchild Semiconductor. Alfke was later a director at Xilinx .

What is FCFS in computer science?

FCFS is also the jargon term for the FIFO operating system scheduling algorithm, which gives every process central processing unit (CPU) time in the order in which it is demanded . FIFO's opposite is LIFO, last-in-first-out, where the youngest entry or "top of the stack" is processed first.

How does FIFO work?

In the process, FIFO enhances the net income as the cheaper older inventory will be used to confirm the current cost of the sold goods. However, the company will have to pay higher taxes for a higher income. The FIFO approach yields a higher value of the final stock, lesser cost of goods sold, and greater gross profit during inflation.

Why is FIFO important?

It is important to the businesses for the following reasons: Determines cost of goods sold. Provides exact numbers for budgets. Evaluating profitability.

What does FIFO mean in stock valuation?

FIFO in inventory valuation means the company sells the oldest stock first and calculates it COGS based on FIFO. Simply put, FIFO means the company sells the oldest stock first and the newest will be the last one to go for sale. This means, the cheapest stock will be sold first and the costliest stock will be the last;

Why is FIFO so efficient?

Cost-efficient and saves time: FIFO can help save a lot of time and money required to estimate the cost of the inventory being sold. This is because the cost directly depends on the foregoing cash flows of purchases that would be used first.

What is FIFO accounting?

FIFO is a method of accounting that assumes that the goods purchased first will be sold first, and it assumes the cost of these goods sold first. FIFO is a widely accepted method across the globe, owing to its efficacy in raising profits.

What is FIFO approach?

The FIFO approach yields a higher value of the final stock, lesser cost of goods sold, and greater gross profit during inflation. This is because in an inflationary market when FIFO is applied, the old stock cleared first leaves behind the costlier items in the balance sheet, to be sold at a higher price in the future.

What is FIFO in business?

Unlike LIFO which is used primarily in the US, FIFO finds approval across the globe. Logical and Easy to understand: FIFO method is easy to understand and convenient to apply for almost all organizations. With a cycle that runs from selling oldest to newest, this model works well for most businesses.

Why is FIFO used?

FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual financial health. Here’s everything you need to know to decide if the FIFO method is right for you.

What is the FIFO method?

Short for first in, first out, the FIFO method is a popular strategy for fulfilling customer orders and assigning costs to your sold inventory for accounting purposes. The first in, first out (or FIFO) method is a strategy for assigning costs to goods sold. Essentially, it means your business sells the oldest items in your inventory first—at least ...

What is FIFO accounting?

That being said, FIFO is primarily an accounting method for assigning costs to your goods sold. So you don’t necessarily have to actually sell your oldest products first—you just account for the cost of goods sold using the oldest numbers. In other words, when determining your business’s cost of goods sold (COGS), ...

What is the first in first out method?

The first in, first out (or FIFO) method is a strategy for assigning costs to goods sold. Essentially, it means your business sells the oldest items in your inventory first—at least on paper, anyway. FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual ...

Is FIFO better than LIFO?

FIFO is also more transparent and easier to use than LIFO. LIFO systems are easy to manipulate to make it look like your business is doing better than it is. But a FIFO system provides a more accurate reflection of the current value of your inventory. This is one of the reasons why the International Financial Reporting Standards (IFRS) Foundation requires businesses to use FIFO.

What is FIFO based on?

With FIFO, however, each piece of inventory sold is based on the constantly changing price of each batch – meaning that once your oldest batch is all sold in the system, your COGS is recalculated and your inventory price-per-piece changes.

What is FIFO accounting?

FIFO is the only IRS-approved method of inventory accounting that doesn’t come with restrictions and additional guidelines. That means it’s a common method of accounting for most businesses, and that’s why ERPLY includes FIFO accounting practices built right into the system. The only thing you have to do to set up FIFO accounting is to set the correct price for inventory products. After that, your orders in the system will automatically calculate everything else you need for FIFO accounting. Additionally, as each product is sold, it will be recorded at the correct price point for FIFO accounting, so you already have the numbers you need when it’s time to file your taxes.

Why does ERPLY use FIFO?

The ERPLY POS uses FIFO for inventory accounting, primarily because it is one of the most accurate methods for calculating inventory cost. The FIFO principle comes into play in many of the functions in the ERPLY system, including setting product costs, setting wholesale prices, and setting warehouse prices.

Is FIFO required by the IRS?

For some businesses, FIFO is the only method allowed by the IRS. If your business has international locations, for example, FIFO is required by the government on tax reporting. But there are other reasons to use FIFO that can be a benefit to your business.

Does FIFO require record keeping?

Additionally, FIFO does not require as much recordkeeping as LIFO, because it assumes that older items are gone.

Does FIFO work for ERPLY?

However, if you do keep a perpetual inventory, such as the automatic inventory system of ERPLY, FIFO will still work very well for you. In this system, inventory is automatically removed from your accounting system, and the cost per piece of inventory (calculated based on the oldest price in your system) is automatically recorded. In this way, you are still calculating your costs based on FIFO, but you are able to keep a closer eye on your inventory at any given moment.

What is a FIFO used for?

And they are very handy! FIFOs can be used for any of these purposes: Crossing clock domains. Buffering data before sending it off chip (e.g. to DRAM or SRAM) Buffering data for software to look at at some later time. Storing data for later processing. YouTube.

What is a FIFO?

A FIFO can be thought of a one-way tunnel that cars can drive through. At the end of the tunnel is a toll with a gate. Once the gate opens, the car can leave the tunnel. If that gate never opens and more cars keep entering the tunnel, eventually the tunnel will fill up with cars. This is called FIFO Overflow and in general it's not a good thing.

What are the rules of FIFO?

The two rules of FIFOs: FIFOs themselves can be made up of dedicated pieces of logic inside your FPGA or ASIC or they can be created from Flip-Flops (distributed registers). Which one of these two the synthesis tools will use is entirely dependent on the FPGA vendor that you are using and how you structure your code.

Is a FIFO overflow a good thing?

This is called FIFO Overflow and in general it's not a good thing. How deep the FIFO is can be thought of as the length of the tunnel. The deeper the FIFO, the more data can fit into it before it overflows. FIFOs also have a width, which represents the width of the data (in number of bits) that enters the FIFO.

What is FIFO in accounting?

The First-In, First-Out (FIFO) method assumes that the first unit making its way into inventory–or the oldest inventory–is the sold first. For example, let's say that a bakery produces 200 loaves of bread on Monday at a cost of $1 each, and 200 more on Tuesday at $1.25 each. FIFO states that if the bakery sold 200 loaves on Wednesday, the COGS ( on the income statement) is $1 per loaf because that was the cost of each of the first loaves in inventory. The $1.25 loaves would be allocated to ending inventory ( on the balance sheet ).

Why is FIFO better than COGS?

FIFO can be a better indicator of the value for ending inventory because the older items have been used up while the most recently acquired items reflect current market prices. For most companies, FIFO is the most logical choice since they typically use their oldest inventory first in the production of their goods, which means the valuation of COGS reflects their production schedule.

Why is LIFO not accurate?

As a result, LIFO doesn't provide an accurate or up-to-date value of inventory because the valuation is much lower than inventory items at today's prices.

Why would COGS be higher under LIFO?

In an inflationary environment, the current COGS would be higher under LIFO because the new inventory would be more expensive. As a result, the company would record lower profits or net income for the period. However, the reduced profit or earnings means the company would benefit from a lower tax liability.

What is LIFO method?

LIFO. When sales are recorded using the LIFO method, the most recent items of inventory are used to value COGS and are sold first. In other words, the older inventory, which was cheaper, would be sold later.

What is the first in first out method?

The First-In, First-Out (FIFO) method assumes that the oldest unit of inventory is the sold first. LIFO is not realistic for many companies because they would not leave their older inventory sitting idle in stock. FIFO is the most logical choice since companies typically use their oldest inventory first in the production of their goods.

When sales are recorded using the FIFO method, what is the oldest inventory?

When sales are recorded using the FIFO method, the oldest inventory–that was acquired first–is used up first. FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet.