- LIFO. When sales are recorded using the LIFO method, the most recent items of inventory are used to value COGS and are sold first.

- FIFO. When sales are recorded using the FIFO method, the oldest inventory–that was acquired first–is used up first.

- Average Cost. The average cost method produces results that fall somewhere between FIFO and LIFO. However, please note that if prices are decreasing, the opposite scenarios outlined above play out.

Why would a company have to pick LIFO or FIFO?

Why Would a Company Have to Pick LIFO or FIFO?

- Inventory FIFO. In inventory management, FIFO means that the oldest inventory items -- the ones purchased first -- are sold before newer items.

- Inventory LIFO. Although it is rare, there are companies that have to pick LIFO, rather than FIFO, to manage their inventory.

- Accounting Considerations. ...

- Accounting Alternatives. ...

Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

Which is a better method LIFO or FIFO?

FIFO assumes that cheaper items are sold first, generating a higher profit than LIFO. However, when the more expensive items are sold in later months, profit is lower. LIFO generates lower profits in early periods and more profit in later months. FIFO is the easier method to use, and most businesses stick with the FIFO method.

How to determine which shares to sell, FIFO or LIFO?

How to Determine Which Shares to Sell, FIFO or LIFO

- FIFO vs LIFO Stock Trades. The first-in, first-out method is the default way to decide which shares to sell. ...

- Tell Your Broker. If you plan to use any method besides FIFO, including LIFO, you must specifically direct your broker as to which shares to sell so that your taxes ...

- 2018 Tax Law Changes. ...

- 2017 Tax Law. ...

When would you use the FIFO method?

When Is First In, First Out (FIFO) Used? The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

Why would a company use LIFO instead of FIFO?

During times of rising prices, companies may find it beneficial to use LIFO cost accounting over FIFO. Under LIFO, firms can save on taxes as well as better match their revenue to their latest costs when prices are rising.

Is FIFO or LIFO better for inventory?

FIFO is more likely to give accurate results. This is because calculating profit from stock is more straightforward, meaning your financial statements are easy to update, as well as saving both time and money. It also means that old stock does not get re-counted or left for so long it becomes unusable.

When would you use the LIFO method?

The LIFO method is used in the COGS (Cost of Goods Sold) calculation when the costs of producing a product or acquiring inventory has been increasing. This may be due to inflation.

When might it be beneficial for a company to use the FIFO method?

If your inventory costs are going down as time goes on, FIFO will allow you to claim a higher average cost-per-piece on newer inventory, which can help you save money on your taxes. Additionally, FIFO does not require as much recordkeeping as LIFO, because it assumes that older items are gone.

Why LIFO is not recommended?

IFRS prohibits LIFO due to potential distortions it may have on a company's profitability and financial statements. For example, LIFO can understate a company's earnings for the purposes of keeping taxable income low. It can also result in inventory valuations that are outdated and obsolete.

Which method is best for inventory valuation?

When it comes to inventory accounting methods, most businesses use the FIFO method because it usually gives the most accurate picture of costs and profitability.

Why is LIFO more accurate?

LIFO inventory accounting increases record-keeping, because older inventory items may be kept on hand for several years, while under FIFO, those older items are sold first, so recordkeeping requirements are less.

Is FIFO or LIFO more accurate for cost of goods sold?

FIFO is considered to be the more transparent and trusted method of calculating cost of goods sold, over LIFO. Here's why. By its very nature, the “First-In, First-Out” method is easier to understand and implement.

Who Uses Last In First Out?

the United StatesLast in, first out (LIFO) is a method used to account for inventory. Under LIFO, the costs of the most recent products purchased (or produced) are the first to be expensed. LIFO is used only in the United States and governed by the generally accepted accounting principles (GAAP).

What type of companies use FIFO?

Many companies that sell perishable commodities such as food or flowers use FIFO inventory tracking. Given that inventory has a limited shelf life in these industries, the FIFO method reduces losses.

Why do some companies use LIFO?

Reason for Using LIFO Another reason for a company to use the LIFO cost flow assumption is to improve the matching of costs with sales. If the company had matched the old low costs using FIFO, the company would show a greater profit that was partly caused by merely holding some old inventory items.

Which is more complicated, LIFO or FIFO?

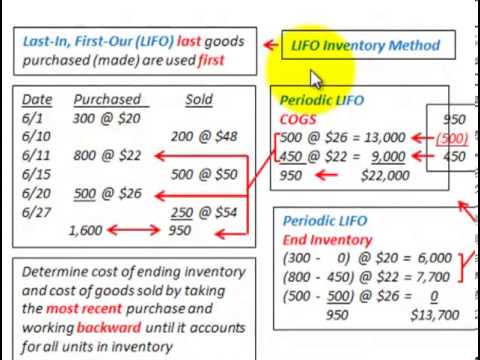

LIFO has much more complicated cost layers than FIFO does. Cost layers are a way to keep track of the inventory, purchasing expenses and profits. Here’s an example to further demonstrate cost layers.

Why is LIFO lower than FIFO?

1. Because of inflation, where costs and expenses continue to rise, LIFO will have a lower profit margin than that of FIFO. This is because there is little to no inflation gap to allow LIFO businesses to capitalize on their inventory.

What is FIFO valuation?

In the end, FIFO is the most widely recognized and accepted valuation method for inventory management. It’s safer, easier and is more advantageous in the long run that dealing with the confusion and potential profit loss of LIFO. Learn more about inventory management techniques to help you make a sound decision for your business. You can also brush up on your accounting skills in our finance and accounting for start-ups course.

What is FIFO in inventory management?

FIFO. The first in first out method of inventory management explains the order in which inventory is purchased and then sold. When a business utilizes the FIFO method, they sell the products that they received first before selling the products they received last.

What are the disadvantages of LIFO?

2. The second disadvantage would be clerical errors. When inventory prices are always in flux it can become cumbersome to correctly record cost of goods, selling price of goods and any discrepancy that may occur because of rising or falling market prices. With last in first out, the last batch of goods purchased is the first batch of goods being sold so the likelihood of a price change is low. However, LIFO has many cost layers and can become quite confusing to record correctly. There is more to this but see LIFO disadvantages below.

Why is LIFO so hard to find investors?

2. Because of LIFO’s generally lower reported profits, businesses utilizing this valuation of inventory can have a harder time finding investors. Individuals and businesses looking to invest their money are usually looking for companies that show substantial profit growth over a period of time.

Why do accountants use FIFO?

Accountants have to write off what’s called obsolete inventory after a certain amount of time goes by and the product is not used or sold. Because FIFO makes sure that the oldest items in stock are used or sold before they are deemed obsolete companies can save money.

What is a FIFO?

FIFO is mostly recommended for businesses that deal in perishable products. The approach provides such ventures with a more accurate value of their profits and inventory. FIFO is not only suited for companies that deal with perishable items but also those that don’t fall under the category.

Why Use FIFO?

The biggest advantage of FIFO lies in its simplicity. It is easy to use, generally accepted and trusted, and it follows the natural physical flow of inventory.

How does LIFO work?

Apart from reducing the tax liability, using the LIFO technique offers other benefits, such as: 1 It complies better with the matching principle, as it charges costs with the revenues of a similar period 2 Reduces the likelihood of write-downs of inventory if their fair market value has decreased 3 In some industries, it conforms with the actual physical flow of inventory, such as in extraction industries (i.e., coal, oil and gas)

What is LIFO system?

The LIFO system is founded on the assumption that the latest items to be stored are the first items to be sold. It is a recommended technique for businesses dealing in products that are not perishable or ones that don’t face the risk of obsolescence.

What does FIFO mean in accounting?

It means that the inventory will be of higher value.

Why is LIFO used in inflationary periods?

Whenever there are price increases, such as in an inflationary period, the LIFO method has the impact of recording the sale of higher-priced items first while the cheaper, older products are maintained as stock . Doing so causes a firm’s cost of goods sold to increase and the net income to decrease. Both aspects help to minimize the company’s tax liability

Which accounting system allows LIFO?

The International Financial Reporting Standards – IFRS – only allows FIFO accounting, while the Generally Accepted Accounting Principles – GAAP – in the U.S. allows companies to choose between LIFO or FIFO accounting.

Benefits

Summary

Use

- The first in first out method of inventory management explains the order in which inventory is purchased and then sold. When a business utilizes the FIFO method, they sell the products that they received first before selling the products they received last. FIFO is the most popular method of inventory management as its easier to use than its last in first out counterpart and its more practical especially when regarding perishable goods.

Example

- For example, when you go grocery shopping you may notice that perishable goods, like milk, have expiration or sell by dates on them. All grocery stores apply the FIFO inventory management method to overseeing their goods. Because of this, youll notice that the milk in the front of the shelf will have an earlier expiration date than the milk on the back of the shelf. This happens because the milk with the earlier expiration date was bought by the groce…

Issues

- 1. I think one of the biggest disadvantages to FIFO is the inconsistent prices given to clients. For example, if youre buying that same batch of dog food for $4,000 and the next month you have to spend $6,000, youre obviously going to have to increase your asking price a bit or your profit margin shrinks. Repeat clients may find this challenging at times but they should also understand the ebb and flow of the market.

Criticisms

- The last in first out method may seem counter-intuitive to some. And for most, it is. In fact its only allowed in the US and its banned by the International Financial Reporting Standards (IFRS). Last in first out is the opposite of FIFO in that the last items acquired by the business are the first ones sold. Most businesses could never implement LIFO because they would lose out on money due to spoiled goods and would experience lower profit…

Cost

- LIFO has much more complicated cost layers than FIFO does. Cost layers are a way to keep track of the inventory, purchasing expenses and profits. Heres an example to further demonstrate cost layers. 3. Due to the complexities of LIFO cost layers, accountants can have a difficult time accurately recording costs and expenses. This is especially true of large businesses that have many operations that implement different inventory management t…

Advantages

- 1. Because of inflation, where costs and expenses continue to rise, LIFO will have a lower profit margin than that of FIFO. This is because there is little to no inflation gap to allow LIFO businesses to capitalize on their inventory.

Risks

- 2. Because of LIFOs generally lower reported profits, businesses utilizing this valuation of inventory can have a harder time finding investors. Individuals and businesses looking to invest their money are usually looking for companies that show substantial profit growth over a period of time. With LIFO, profits will rise with inflation but they will not reflect the kind of healthy business investors are seeking.

Results

- In the end, FIFO is the most widely recognized and accepted valuation method for inventory management. Its safer, easier and is more advantageous in the long run that dealing with the confusion and potential profit loss of LIFO. Learn more about inventory management techniques to help you make a sound decision for your business. You can also brush up on your accounting skills in our finance and accounting for start-ups course.