Learn about FIFO and LIFO to help you decide.

- FIFO (first in, first out) inventory management seeks to sell older products first so that the business is less likely to lose money when the products expire or become obsolete.

- LIFO (last in, first out) inventory management applies to nonperishable goods and uses current prices to calculate the cost of goods sold.

- Both U.S. ...

How to determine which shares to sell, FIFO or LIFO?

How to Determine Which Shares to Sell, FIFO or LIFO

- FIFO vs LIFO Stock Trades. The first-in, first-out method is the default way to decide which shares to sell. ...

- Tell Your Broker. If you plan to use any method besides FIFO, including LIFO, you must specifically direct your broker as to which shares to sell so that your taxes ...

- 2018 Tax Law Changes. ...

- 2017 Tax Law. ...

How do companies report switching from LIFO to FIFO?

Your Top Offers

- FIFO vs. LIFO. ...

- Retrospective vs. Prospective. ...

- Change in Inventory Valuation Method Disclosure Requirements. Financial statements are required to disclose all significant changes in accounting policies. ...

- Federal Tax Changes. ...

What type of business would use LIFO?

- specific identification method

- FIFO

- weighted average method

How would FIFO and LIFO affect the income taxes paid?

The main difference between LIFO and FIFO is based on the assertion that the most recent inventory purchased is usually the most expensive. If that assertion is accurate, using LIFO will result in a higher cost of goods sold and less profit, which also directly affects the amount of taxes you’ll have to pay. What is LIFO?

When would you use the FIFO method?

When Is First In, First Out (FIFO) Used? The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

How do you choose between FIFO and LIFO?

FIFO or LIFO: Which is Better?If your inventory costs are going up, or are likely to increase, LIFO costing may be better because the higher cost items (the ones purchased or made last) are considered to be sold. ... If the opposite is true, and your inventory costs are going down, FIFO costing might be better.

When would LIFO be used?

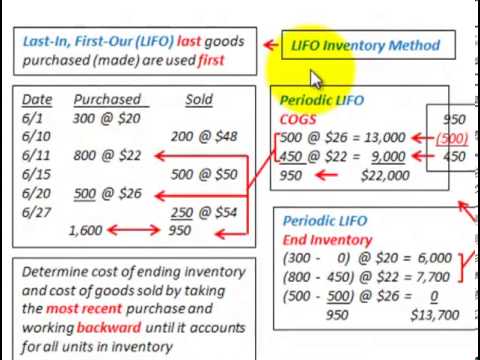

Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

Which inventory method is best?

The most popular inventory accounting method is FIFO because it typically provides the most accurate view of costs and profitability.

Which inventory valuation method is best?

When it comes to inventory accounting methods, most businesses use the FIFO method because it usually gives the most accurate picture of costs and profitability.

Why do companies use FIFO?

If your inventory costs are going down as time goes on, FIFO will allow you to claim a higher average cost-per-piece on newer inventory, which can help you save money on your taxes. Additionally, FIFO does not require as much recordkeeping as LIFO, because it assumes that older items are gone.

Why do companies prefer LIFO?

The primary reason that companies choose to use an LIFO inventory method is that when you account for your inventory using the “last in, first out” method, you report lower profits than if you adopted a “first in, first out” method of inventory, known commonly as FIFO.

Why would a company change from LIFO to FIFO?

For this and other reasons, CPAs may be called upon to advise companies switching from LIFO to FIFO (first in, first out) or average cost. A change from LIFO to FIFO typically would increase inventory and, for both tax and financial reporting purposes, income for the year or years the adjustment is made.

What is FIFO in accounting?

FIFO and LIFO are methods used in the cost of goods sold calculation. FIFO (“First-In, First-Out”) assumes that the oldest products in a company’s inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company’s inventory have been sold first ...

What is LIFO reserve?

The LIFO reserve is the amount by which a company’s taxable income has been deferred, as compared to the FIFO method. The remaining unsold 350 televisions will be accounted for in “inventory”.

Why are FIFO profits more accurate?

Although this may mean less tax for a company to pay under LIFO, it also means stated profits with FIFO are much more accurate because older inventory reflects the actual costs of that inventory. If profits are naturally high under FIFO, then the company becomes that much more attractive to investors.

Is LIFO more attractive than FIFO?

You can see how for Ted, the LIFO method may be more attractive than FIFO. This is because the LIFO number reflects a higher inventory cost, meaning less profit and less taxes to pay at tax time. The LIFO reserve in this example is $31,250.

Is LIFO legal in the US?

Under GAAP, LIFO is legal. Outside the United States, LIFO is not permitted as an accounting practice. This is why you’ll see some American companies use the LIFO method on their financial statements, and switch to FIFO for their international operations.

Why use FIFO vs LIFO?

FIFO vs. LIFO for flow of goods. Many companies choose to use FIFO because it more closely mimics the actual flow of goods in and out of inventory. It's considered a simpler system with less spoilage and waste of materials.

Why is FIFO higher than LIFO?

Because the cost of goods sold is usually higher under LIFO, this decreases a company's reported profits, which can lower the amount of tax liability. Conversely, FIFO valuations present a higher tax liability because the cost of goods sold is lower. Read more: FIFO Accounting: What It Is and What You Need To Know.

What is a fifo and a fifo?

While both FIFO and LIFO are a way to manage inventory, the marketable goods produced by a company usually dictate which method to choose. FIFO is typically used for perishable products like food and beverages or stock that may become obsolete if it isn't sold within a certain period of time. LIFO however is often used for products that aren't affected by the amount of time spent in inventory or where the flow of product fits the LIFO method.

How is FIFO inventory calculated?

FIFO inventory cost is calculated by determining the cost of the oldest stock and multiplying that amount by the number of items sold.

What is FIFO in inventory?

What is FIFO? First in, first out is a method to value inventory and calculate the cost of goods sold. FIFO items are the oldest products in an inventory because they were the first stock to be added after purchase or production. FIFO uses the principle that when items are acquired first, they are also sold first.

What is LIFO method?

Using the LIFO method, more recent stock can be valued higher than older goods when there is a price increase. LIFO works well using the matching principle, which is used to charge costs along with revenues during the same period of inventory calculations. Read more: A Guide To the Inflation Rate.

What is the last in first out approach?

Last in, first out is another way to manage inventory and calculate profits from goods. In this approach, businesses figure that the most recent inventory is the first sold. This means that older stock continues to sit for longer periods before being sold.

Why is LIFO so controversial?

The higher COGS under LIFO decreases net profits and thu s creates a lower tax bill for One Cup. This is why LIFO is controversial; opponents argue that during times of inflation, LIFO grants an unfair tax holiday for companies. In response, proponents claim that any tax savings experienced by the firm are reinvested and are of no real consequence to the economy. Furthermore, proponents argue that a firm's tax bill when operating under FIFO is unfair (as a result of inflation).

Why do companies use LIFO?

A final reason that companies elect to use LIFO is that there are fewer inventory write-downs under LIFO during times of inflation. An inventory write-down occurs when the inventory is deemed to have decreased in price below its carrying value .

How does LIFO work?

How Last in, First out (LIFO) Works. Under LIFO, a business records its newest products and inventory as the first items sold. The opposite method is FIFO, where the oldest inventory is recorded as the first sold. While the business may not be literally selling the newest or oldest inventory, it uses this assumption for cost accounting purposes.

Why is LIFO used?

When prices are rising, it can be advantageous for companies to use LIFO because they can take advantage of lower taxes. Many companies that have large inventories use LIFO, such as retailers or automobile dealerships.

What is LIFO for businesses?

Businesses that sell products that rise in price every year benefit from using LIFO. When prices are rising, a business that uses LIFO can better match their revenues to their latest costs.

What is the LIFO method?

Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first . This method is banned under the International Financial Reporting Standards ...

How many mugs does one cup sell in 2020?

In 2020, One Cup sells 250 mugs on the Internet. Under LIFO, COGS is equal to: the total cost of the 100 mugs purchased from the wholesaler in 2019, plus the cost of 100 mugs purchased in 2018, plus the cost of 50 of the 100 mugs purchased in 2017.

Why use LIFO or FIFO?

The LIFO method for financial accounting may be used over FIFO when the cost of inventory is increasing, perhaps due to inflation. Using FIFO means the cost of a sale will be higher because the more expensive items in inventory are being sold off first.

What is the difference between FIFO and LIFO?

The FIFO (“First-In, First-Out”) method means that the cost of a company’s oldest inventory is used in the COGS (Cost of Goods Sold) calculation. LIFO (“Last-In, First-Out”) means that the cost of a company’s most recent inventory is used instead. Here’s What We’ll Cover:

What does FIFO mean in accounting?

FIFO is an acronym. It stands for “First-In, First-Out” and is used for cost flow assumption purposes. Cost flow assumptions refers to the method of moving the cost of a company’s product out of its inventory to its cost of goods sold. Inventory refers to:

What is the LIFO method?

Recordkeeping. If you choose to use the LIFO method of inventory valuation, you will need a recordkeeping system that allows you to determine when you access older “layers” of inventory and then apply the cost of that older inventory accurately.

What does FIFO mean in inventory?

FIFO stands for “first in, first out” and assumes the first items entered into your inventory are the first ones you sell. LIFO, also known as “last in, first out,” assumes the most recent items entered into your inventory will be the ones to sell first. The inventory valuation method you choose will depend on your tax situation, ...

What is inventory flow?

Inventory flow: Most businesses sell the oldest items in stock first. Think of a grocery store or a clothing boutique: In both of these types of businesses, stock loses its value with time, and so the older items are pushed to the front of the shelves to help them sell quicker.

Can you use LIFO or FIFO valuation?

Inventory flow. For spools of craft wire, you can reasonably use either LIFO or FIFO valuation. For perishable goods — like groceries — or other items that lose their value with time, using LIFO valuation doesn’t make sense because you will always try to sell older inventory first.

Can you use LIFO for inventory?

You can choose to value all your inventory using LIFO, or you can use LIFO just for certain goods you carry. Once you elect to use LIFO for your inventory valuation, you cannot switch back to FIFO or another inventory valuation method without express permission from the IRS. To request a change in inventory valuation from the IRS, ...

Is LIFO more onerous than FIFO?

Recordkeeping: When comparing FIFO vs. LIFO, the recordkeeping requirements for LIFO are typically more onerous than those for FIFO. This is because the inventory in a business that uses LIFO is “layered,” meaning older inventory can be held for long periods of time.

Is LIFO valuation allowed?

Reporting requirements. If you are looking to do business internationally, you must keep IFRS requirements in mind. LIFO valuation is not allowed under these standards. If you plan to do business outside of the U.S., choose FIFO or another inventory valuation method instead. Back to top.

Why use LIFO over FIFO?

The advantages of LIFO are also its disadvantages as the only real purpose of instituting LIFO is to avoid paying higher taxes but this means profits are generally lower.

What is FIFO in inventory management?

FIFO. The first in first out method of inventory management explains the order in which inventory is purchased and then sold. When a business utilizes the FIFO method, they sell the products that they received first before selling the products they received last.

Why is LIFO so hard to find investors?

2. Because of LIFO’s generally lower reported profits, businesses utilizing this valuation of inventory can have a harder time finding investors. Individuals and businesses looking to invest their money are usually looking for companies that show substantial profit growth over a period of time.

Why do accountants have to write off obsolete inventory?

Because FIFO makes sure that the oldest items in stock are used or sold before they are deemed obsolete companies can save money. 2.

What are the advantages and disadvantages of LIFO?

Like mentioned above, LIFO most often means lower profits for the company, but when you report lower profits, you don’t have to pay as many income taxes. This allows the business to have more cash-in-hand to use for investment opportunities or to purchase more inventory. Disadvantages.

What happens when a company uses FIFO?

When companies use FIFO they will constantly have an updated reflection of the current market prices for the items in their inventory. This happens as older products are taken from the inventory stock to be sold, the newer inventory is left on the books for the end of the month.

What is the cost of goods?

The cost of goods is the price you pay to obtain your inventory and when the cost of goods is low and the market value high – you’ll enjoy a nice profit margin. Likewise, the contrary can be true.

Why is LIFO used?

LIFO is well used in inventory accounting to increase the cost of goods sold by a company. It is also used to reduce net profits, which can then reduce corporate tax liability. So, it is not surprising that LIFO is much more desirable when the corporate tax rate is higher.

What is a LIFO?

LIFO and FIFO are the two most common inventory methods that are used by a company. The goal is to properly account for cost of purchased inventory on the balance sheet. Generally, a business can calculate its inventory either directly or through profits shown in the income statement and the cash flow statement.

What is LIFO in accounting?

LIFO or "last-in, first-out" is a method of accounting for inventory that assumes an inventory unit which is bought first will come out last. It also means that the first unit to be sold is the last inventory that comes into the warehouse. Under LIFO, if there is the last units of inventory purchased were bought at the highest price, ...

What are the advantages of LIFO?

There are several advantages of LIFO for inventory accounting method: 1) Easy to compare current costs with current income, 2) If prices increase then the price of goods becomes conservative, 3) Operating profit is not affected by profit or loss from price fluctuations, 4) More tax savings.

What does FIFO mean in warehouse?

FIFO (First-In, First-Out) As the name suggests, FIFO means the first entry comes out first. This method assumes that the first units to enter warehouse are sold first. So, the oldest items are sold first. This system is usually used by companies with perishable inventory.

Which takes the most investment of funds?

Inventory usually takes the most investment of funds. One way to calculate the profits generated by a company is to track sales revenues and all the costs involved in producing the goods.

What is LIFO method?

The LIFO method is one that you have to elect affirmatively with your broker. The main benefit of the LIFO method is that the shares that you've owned for the shortest period of time tend to be the ones that have the smallest taxable gain, and so you can make a sale without incurring a large tax bill. However, because the LIFO method involves the ...

What does FIFO mean in stock?

FIFO and LIFO are acronyms that, in this case, relate to the stock you decide to sell. FIFO stands for first in, first out, while LIFO stands for last in, first out. What this means is that if you use the FIFO method, then a sale of stock will be allocated to the shares you bought earliest.

What is FIFO in tax?

The FIFO method is the default for the IRS, and so if you don't specify a method with your broker when you sell shares, you'll automatically be treated as if you had elected FIFO treatment. The main benefit of the FIFO method is that by using the shares you acquired first, you're more likely to get long-term capital gains treatment ...

What is the disadvantage of FIFO method?

The disadvantage of the FIFO method, however, is that because stock prices tend to rise over time, the shares you bought first will typically have the lowest cost basis. That means that your taxable gain could be higher than it would be on other shares you've owned for a shorter period of time.