Examples of situations where you might use FIFO queues include the following:

- To make sure that user-entered commands are run in the right order.

- To display the correct product price by sending price modifications in the right order.

- To prevent a student from enrolling in a course before registering for an account.

Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

Why does Amazon use FIFO?

Summary

- Amazon recently hit an all-time high after rumors of the potential launch of its own shopping channel.

- Valuation analysis can provide useful information, but for some companies, it's better to use one method over another.

- In the case of Amazon, 'price to cash flow' is a better valuation metric than price/earnings.

What does FIFO stand for?

First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last.

What is the difference between FIFO vs. LIFO?

- First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method.

- Last-in, first-out (LIFO) assumes the last inventory added will be the first sold.

- Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

What are the 5 main reasons for using FIFO?

5 Benefits of FIFO Warehouse StorageIncreased Warehouse Space. Goods can be packed more compactly to free up extra floor space in the warehouse.Warehouse Operations are More Streamlined. ... Keeps Stock Handling to a Minimum. ... Enhanced Quality Control. ... Warranty Control.

Why should FIFO be used?

If your inventory costs are going down as time goes on, FIFO will allow you to claim a higher average cost-per-piece on newer inventory, which can help you save money on your taxes. Additionally, FIFO does not require as much recordkeeping as LIFO, because it assumes that older items are gone.

When should you not use FIFO?

1: Batch Processing If you are moving or processing your parts in boxes or batches, then it will be difficult to maintain a FiFo within the box. It is possible using some creative numbering scheme, but unless there is a compelling reason to do so, the effort is not worth the benefit.

Why would a company choose to use FIFO costing?

Companies must use FIFO for inventory if they are selling perishable goods such as food, which expires after a certain period of time. Companies selling products with relatively short demand cycles, such as designer fashion, also may have to pick FIFO to ensure they are not stuck with outdated styles in inventory.

Why would a company choose FIFO over LIFO?

FIFO is more likely to give accurate results. This is because calculating profit from stock is more straightforward, meaning your financial statements are easy to update, as well as saving both time and money. It also means that old stock does not get re-counted or left for so long it becomes unusable.

What are the pros and cons of FIFO?

FIFO vs. LIFO: Pros and ConsFIFOCOMPLEXITYLess complex. Minimal to no COGS fluctuation.INFLATIONLower COGS. Higher profits. Greater tax liability. Higher earnings and net worth appeal to investors.DEFLATIONHigher COGS. Lower profits. Reduced tax liability. Lower earnings and net worth may discourage investors.3 more rows

What type of businesses use FIFO?

Companies that sell perishable products or units subject to obsolescence, such as food products or designer fashions, commonly follow the FIFO method of inventory valuation.

What is FIFO method?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

What is FIFO in manufacturing?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense. Under FIFO, it is assumed that the cost of inventory purchased first will be recognized first. The dollar value of total inventory decreases in this process because inventory has been removed from the company’s ownership. The costs associated with the inventory may be calculated in several ways — one being the FIFO method.

What is the opposite of FIFO?

The opposite of FIFO is LIFO (Last In, First Out), where the last item purchased or acquired is the first item out. In inflationary economies, this results in deflated net income costs and lower ending balances in inventory when compared to FIFO.

What is FIFO accounting?

First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last. An alternative to FIFO, LIFO is an accounting method in which assets purchased or acquired last are disposed of first.

What are the advantages of first in first out?

What Are the Advantages of First In, First Out (FIFO)? The obvious advantage of FIFO is that it's most widely used method of valuing inventory globally. It is also the most accurate method of aligning the expected cost flow with the actual flow of goods which offers businesses a truer picture of inventory costs.

Why is FIFO preferred?

The advantages to the FIFO method are as follows: The method is easy to understand, universally accepted and trusted. FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first).

What does FIFO mean in accounting?

FIFO stands for “First-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company’s inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation.

Why is the LIFO method understated?

The value of remaining inventory, assuming it is not-perishable, is also understated with the LIFO method because the business is going by the older costs to acquire or manufacture that product. That older inventory may, in fact, stay on the books forever. Investors and banking institutions value FIFO because it is a transparent method ...

Why do investors value FIFO?

Investors and banking institutions value FIFO because it is a transparent method of calculating cost of goods sold. It is also easier for management when it comes to bookkeeping, because of its simplicity.

Is FIFO overstating profit?

A company also needs to be careful with the FIFO method in that it is not overstating profit. This can happen when product costs rise and those later numbers are used in the cost of goods calculation, instead of the actual costs.

Is the FIFO method legal?

Both are legal although the LIFO method is often frowned upon because bookkeeping is far more complex and the method is easy to manipulate.

What is the FIFO method?

FIFO stands for first in, first out, an easy-to-understand inventory valuation method that assumes that goods purchased or produced first are sold first. In theory, this means the oldest inventory gets shipped out to customers before newer inventory.

What method of inventory management should you use?

Of course, you should consult with an accountant but the FIFO method is often recommended for inventory valuation purposes.

Leave inventory management to the pros

ShipBob’s tech-enabled retail fulfillment solution is designed for fast-growing B2B ecommerce and direct-to-consumer brands .

FIFO FAQs

Here are answers to the most common questions about the FIFO inventory method.

What is FIFO based on?

With FIFO, however, each piece of inventory sold is based on the constantly changing price of each batch – meaning that once your oldest batch is all sold in the system, your COGS is recalculated and your inventory price-per-piece changes.

Why does ERPLY use FIFO?

The ERPLY POS uses FIFO for inventory accounting, primarily because it is one of the most accurate methods for calculating inventory cost. The FIFO principle comes into play in many of the functions in the ERPLY system, including setting product costs, setting wholesale prices, and setting warehouse prices.

What is FIFO accounting?

FIFO is the only IRS-approved method of inventory accounting that doesn’t come with restrictions and additional guidelines. That means it’s a common method of accounting for most businesses, and that’s why ERPLY includes FIFO accounting practices built right into the system. The only thing you have to do to set up FIFO accounting is to set the correct price for inventory products. After that, your orders in the system will automatically calculate everything else you need for FIFO accounting. Additionally, as each product is sold, it will be recorded at the correct price point for FIFO accounting, so you already have the numbers you need when it’s time to file your taxes.

Is FIFO required by the IRS?

For some businesses, FIFO is the only method allowed by the IRS. If your business has international locations, for example, FIFO is required by the government on tax reporting. But there are other reasons to use FIFO that can be a benefit to your business.

Does FIFO require record keeping?

Additionally, FIFO does not require as much recordkeeping as LIFO, because it assumes that older items are gone.

Does FIFO work for ERPLY?

However, if you do keep a perpetual inventory, such as the automatic inventory system of ERPLY, FIFO will still work very well for you. In this system, inventory is automatically removed from your accounting system, and the cost per piece of inventory (calculated based on the oldest price in your system) is automatically recorded. In this way, you are still calculating your costs based on FIFO, but you are able to keep a closer eye on your inventory at any given moment.

Why is FIFO used?

FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual financial health. Here’s everything you need to know to decide if the FIFO method is right for you.

What is the FIFO method?

Short for first in, first out, the FIFO method is a popular strategy for fulfilling customer orders and assigning costs to your sold inventory for accounting purposes. The first in, first out (or FIFO) method is a strategy for assigning costs to goods sold. Essentially, it means your business sells the oldest items in your inventory first—at least ...

What is FIFO accounting?

That being said, FIFO is primarily an accounting method for assigning costs to your goods sold. So you don’t necessarily have to actually sell your oldest products first—you just account for the cost of goods sold using the oldest numbers. In other words, when determining your business’s cost of goods sold (COGS), ...

What is the first in first out method?

The first in, first out (or FIFO) method is a strategy for assigning costs to goods sold. Essentially, it means your business sells the oldest items in your inventory first—at least on paper, anyway. FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual ...

Is FIFO better than LIFO?

FIFO is also more transparent and easier to use than LIFO. LIFO systems are easy to manipulate to make it look like your business is doing better than it is. But a FIFO system provides a more accurate reflection of the current value of your inventory. This is one of the reasons why the International Financial Reporting Standards (IFRS) Foundation requires businesses to use FIFO.

Why is FIFO accounting used?

FIFO method of accounting saves time, and money spends in calculating the exact inventory cost that is being sold because the recording of inventory is done in the same order as they are purchased or produced. Easy to understand.

What are the disadvantages of FIFO accounting?

One of the biggest disadvantages of FIFO accounting method is inventory valuation during inflation, First In First Out method will result in higher profits, and thus will results in higher “Tax Liabilities” in that particular period. This may result in increased tax charges and higher tax-related cash outflows.

Is the first in first out method a good measure of inventory?

Use of First In First Out method is not a suitable measure of inventory in times of “ hyperinflation .”. During such times, there is no particular pattern of inflation, which may result in prices of goods to inflate drastically.

Does inflation increase operating expenses?

Normally in an inflationary environment, prices are always rising, which will cause an increase in operating expenses, but with FIFO accounting, the same inflation will cause an increase in ending inventory.

What is a FIFO?

Disk controllers can use the FIFO as a disk scheduling algorithm to determine the order in which to service disk I/O requests. Communication network bridges, switches and routers used in computer networks use FIFOs to hold data packets en route to their next destination.

What does FIFO mean in data?

FIFO is an abbreviation for first in, first out. It is a method for handling data structures where the first element is processed first and the newest element is processed last. Real life example: In this example, following things are to be considered: There is a ticket counter where people come, take tickets and go.

What is the advantage of FIFO method?

The first in first out (FIFO) method of inventory valuation has the following advantages for business organization: FIFO method saves money and time in calculating the exact cost of the inventory being sold because the cost will depend upon the most former cash flows of purchases to be used first.

Why is FIFO not appropriate?

FIFO will not be an appropriate measure if the materials/goods purchased have fluctuating price patterns, because this can result in misstated profits for the same period as different costs of same goods during that same period are recorded.

What is the first in first out method of inventory valuation?

The first in first out (FIFO) method of inventory valuation has the following advantages for business organization: 1 FIFO method saves money and time in calculating the exact cost of the inventory being sold because the cost will depend upon the most former cash flows of purchases to be used first. 2 It is a simple concept which is easy to understand. Even a layman can grab the idea with little explanation. The managers with little to no accounting information would be able to understand it easily. 3 It is a fairly practical approach to use, as sometimes it becomes difficult to identify the costs of the products sold at the point of sale and FIFO rectifies the matter. 4 It is a widely used and accepted approach of valuation which increases its comparability and consistency. 5 It makes manipulation of the income reported in financial statements difficult, as under FIFO policy there remains no vagueness about the values to be used in cost of sales figure of profit/loss statement. 6 FIFO will show increased gross and net profits in times of increasing prices of goods.#N#Cost of sales = opening stock + Purchases – closing stock#N#This is because the “cost of sales” consists of figure of inventory and as first inventories will have less cost than recent inventories during inflation, the profits reported would be higher.

What are the disadvantages of using a FIFO valuation method?

The major disadvantages of using a FIFO inventory valuation method are given below: One of the biggest disadvantage of FIFO approach of valuation for inventory/stock is that in the times of inflation it results in higher profits, due to which higher “Tax Liabilities” incur . It can result in increased cash out flows in relation to tax charges.

Why does FIFO show increased gross and net profits?

This is because the “cost of sales” consists of figure of inventory and as first inventories will have less cost than recent inventories during inflation, the profits reported would be higher.

Is FIFO a measure of hyperinflation?

FIFO may not be a suitable measure in times of “hyper inflation”. In such times there exist no reasonable pattern of inflation and prices of goods could inflate drastically.

How does FIFO work?

In the manufacturing world, first-in, first-out (FIFO) is an inventory management/valuation system used during an accounting period to assign costs to a company's goods (including raw materials, goods that are in production, and finished goods that ready for sale). As its name implies, FIFO assumes the first ...

What does FIFO mean?

As its name implies, FIFO assumes the first inventory manufactured or purchased during a period is sold first, while the inventory manufactured or produced last is sold last. It's kind of like milk in a grocery store. The milk the store buys first is pushed to the front of the shelf and sold first.

What is the opposite of FIFO?

One alternative accounting method to FIFO is LIFO ( last-in, first-out ). As the name implies, this approach is the opposite of FIFO: The LIFO method assumes goods manufactured or purchased last during a period are the first sold. So, under LIFO, the most recent products are the first to be expensed as cost of goods sold (COGS), which means the lower cost of older products will be reported as ending inventory.

What is FIFO accounting?

The Bottom Line. First-in, first-out (FIFO) is a popular and GAAP -approved accounting method that companies use to calculate and value their inventory —which, of course, ultimately impacts their earnings. FIFO has several strong points. But it also has drawbacks, most of them related to inflation. Let's look at the disadvantages ...

What are the advantages of FIFO?

FIFO has several advantages as an accounting system. Among them: 1 It's easy to understand and use—in fact, it's one of the most widely applied accounting methods out there, both in the U.S. and abroad. 2 It makes it difficult to manipulate figures and income—the cost attached to the unit sold is always the oldest cost. 3 It aligns the expected cost flow with the logical, physical flow of goods (in our example, we sold our older muffins first, remember), offering businesses a truer picture of inventory costs. 4 It's a better indicator of the worth of the ending inventory—the balance sheet amount is likely to approximate the current market value.

Why does LIFO show the largest cost of goods sold?

During periods of inflation, LIFO shows the largest cost of goods sold because the newest costs charged to COGS are also the highest costs. The larger the cost of goods sold, the smaller the net income—and the smaller the tax liability.

How does FIFO affect net income?

As a result, FIFO can increase net income and inflate profits, because inventory that might be several years old, which was acquired or produced for a lower cost is used to value your expenses.

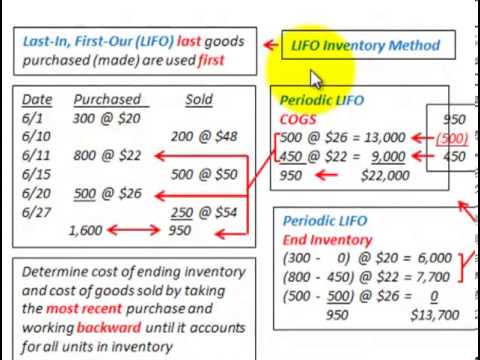

FIFO vs. LIFO

- To reiterate, FIFO expenses the oldest inventories first. In the following example, we will compare FIFO to LIFO (last in first out)Last-In First-Out (LIFO)The Last-in First-out (LIFO) method of inventory valuation is based on the practice of assets produced or acquired last being the first to be. LIFO expenses the most recent costs first. Consider the same example above. Recall that un…

Impact of FIFO Inventory valuation Method on Financial Statements

- Recall the comparison example of First-In First-Out and LIFO. The two methods yield different inventory and COGS. Now it is important to consider the impact of using FIFO on a company’s financial statements?

Key Takeaways from First-In First-Out

- FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold.

- It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system.

- FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold.

- It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system.

- It provides a poor matching of revenue with expenses.

Related Reading

- CFI is a global provider of financial analyst training and career advancement for finance professionals, including the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll t…

What Is The FIFO Method?

- FIFO stands for first in, first out, an easy-to-understand inventory valuation methodthat assumes that goods purchased or produced first are sold first. In theory, this means the oldest inventory gets shipped out to customers before newer inventory. To calculate the value of ending inventory, the cost of goods sold (COGS) of the oldest inventory is...

What’s The Difference Between FIFO vs. LIFO?

- LIFO stands for last in, first out, which assumes goods purchased or produced last are sold first (and the inventory that was most recently purchased will be sent to customers before the oldest inventory). It is an alternative valuation method and is only legally used by US-based businesses. FIFO, on the other hand, is the most common inventory valuation method in most countries, acc…

What Method of Inventory Management Should You use?

- Of course, you should consult with an accountant but the FIFO method is often recommended for inventory valuation purposes. If you sell a product that requires fulfilling older inventory first for quality purposes (especially if you sell perishables and other types of time-sensitive goods), the FIFO method will follow the natural flow of inventory, providing accurate numbers. For retailers d…

Leave Inventory Management to The Pros

- ShipBob’s tech-enabled retail fulfillment solution is designed for fast-growing B2B ecommerce and direct-to-consumer brands. For inventory tracking purposes and accurate fulfillment, ShipBob uses a lot tracking system that includes a lot feature, allowing you to separate items based on their lot numbers. When you send us a lot item, it will not be sold with other non-lot items, or oth…