First In First Out (FIFO)

- First In First Out (FIFO) This method assumes that inventory purchased first is sold first. Therefore, inventory cost under FIFO method will be the cost of latest purchases.

- Example. The sales made on January 5 and 10 were clearly made from purchases on 1st January. ...

- Quiz. How much do you know about inventory costing methods? ...

Which is a better method LIFO or FIFO?

FIFO assumes that cheaper items are sold first, generating a higher profit than LIFO. However, when the more expensive items are sold in later months, profit is lower. LIFO generates lower profits in early periods and more profit in later months. FIFO is the easier method to use, and most businesses stick with the FIFO method.

What is the difference between FIFO and average method?

Difference between FIFO and average costing method: 1. Primary distinction: The primary difference between the two methods is the cost ascertained to the inventory that is dispatched or sold by a business. In FIFO method, the basic assumption followed is that inventory which is acquired first or enters the business first will be the first to exit.

What are the pros and cons of FIFO?

What are the disadvantages of the FIFO life?

- Long hours and shift work is undoubtedly one of the toughest aspects of FIFO work. ...

- Most sites are remote, and workers can be exposed to extreme temperatures, dust, pests and harsh terrain. ...

- FIFO can put a lot of stress on families and relationships. ...

- The roster system means it can be very difficult to plan for social events at home. ...

Why would a company use LIFO instead of FIFO?

Key Takeaway

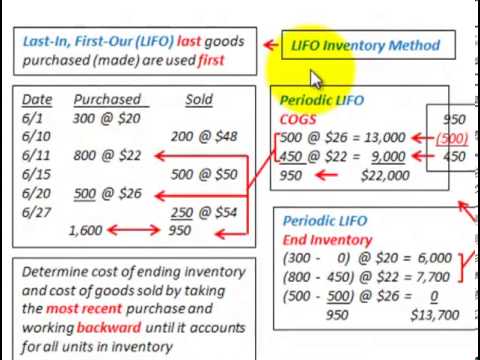

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

What is FIFO method explain it with a example?

The FIFO method requires that what comes in first goes out first. For example, if a batch of 1,000 items gets manufactured in the first week of a month, and another batch of 1,000 in the second week, then the batch produced first gets sold first. The logic behind the FIFO method is to avoid obsolescence of inventory.

What is FIFO method formula?

To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

What is LIFO and FIFO with example?

First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method. Last-in, first-out (LIFO) assumes the last inventory added will be the first sold. Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

What is LIFO example?

Example of LIFO that buys coffee mugs from wholesalers and sells them on the internet. One Cup's cost of goods sold (COGS) differs when it uses LIFO versus when it uses FIFO. In the first scenario, the price of wholesale mugs is rising from 2016 to 2019.

What is the importance of FIFO?

FIFO helps food establishments cycle through their stock, keeping food fresher. This constant rotation helps prevent mold and pathogen growth. When employees monitor the time food spends in storage, they improve the safety and freshness of food. FIFO can help restaurants track how quickly their food stock is used.

Why is FIFO the best method?

FIFO is more likely to give accurate results. This is because calculating profit from stock is more straightforward, meaning your financial statements are easy to update, as well as saving both time and money. It also means that old stock does not get re-counted or left for so long it becomes unusable.

When FIFO method is most suitable?

Key takeaway: FIFO and LIFO allow businesses to calculate COGS differently. From a tax perspective, FIFO is more advantageous for businesses with steady product prices, while LIFO is better for businesses with rising product prices.

What do you mean by LIFO method?

LIFO stands for “Last-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The LIFO method assumes that the most recent products added to a company's inventory have been sold first. The costs paid for those recent products are the ones used in the calculation.

What is the difference between FIFO first in, first out and LIFO last in, first out accounting quizlet?

* FIFO (first-in-first-out) assumes merchandise is sold in the order it was acquired by a firm. * LIFO (last-in-first-out) assumes merchandise is sold in the reverse of the order it was acquired by a firm.

What is Fefo and FIFO?

FEFO / FIFO is a technique for managing loads that aims to supply products (to make them flow through the supply chain) by selecting those closest to expiration first (First Expired, First Out), and when the expiration is the same, the oldest first (First In, First Out).

Is a Queue FIFO or LIFO?

The queue data structure follows the FIFO (First In First Out) principle, i.e. the element inserted at first in the list, is the first element to be removed from the list. The insertion of an element in a queue is called an enqueue operation and the deletion of an element is called a dequeue operation.

Who uses LIFO?

All Answers (8) Generally, automotive suppliers in terms of urgency (emergency) to fulfill the customer demand they used LIFO components.

What is FIFO expense?

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

What is the benefit of using FIFO?

1. Better valuation of inventory . By using FIFO, the balance sheet shows a better approximation of the market value of inventory. The latest costs for manufacturing or acquiring the inventory are reflected in inventory, and therefore, the balance sheet reflects the approximate current market value.

Can you use LIFO in Canada?

Therefore, we can see that the balances for COGS and inventory depend on the inventory valuation method. For income tax purposes in Canada, companies are not permitted to use LIFO. However, US companies are able to use FIFO or LIFO.

Methods of calculating inventory cost

As inventory is usually purchased at different rates (or manufactured at different costs) over an accounting period, there is a need to determine what cost needs to be assigned to inventory.

First In First Out (FIFO)

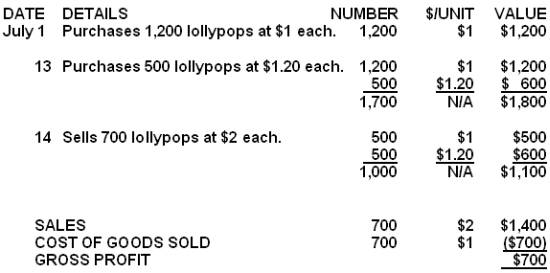

This method assumes that inventory purchased first is sold first. Therefore, inventory cost under FIFO method will be the cost of latest purchases. Consider the following example:

Example

Bike LTD purchased 10 bikes during January and sold 6 bikes, details of which are as follows:

What is FIFO method?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

What is FIFO in manufacturing?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense. Under FIFO, it is assumed that the cost of inventory purchased first will be recognized first. The dollar value of total inventory decreases in this process because inventory has been removed from the company’s ownership. The costs associated with the inventory may be calculated in several ways — one being the FIFO method.

What is the opposite of FIFO?

The opposite of FIFO is LIFO (Last In, First Out), where the last item purchased or acquired is the first item out. In inflationary economies, this results in deflated net income costs and lower ending balances in inventory when compared to FIFO.

What is FIFO accounting?

First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last. An alternative to FIFO, LIFO is an accounting method in which assets purchased or acquired last are disposed of first.

What are the advantages of first in first out?

What Are the Advantages of First In, First Out (FIFO)? The obvious advantage of FIFO is that it's most widely used method of valuing inventory globally. It is also the most accurate method of aligning the expected cost flow with the actual flow of goods which offers businesses a truer picture of inventory costs.

What is FIFO approach?

The FIFO approach yields a higher value of the final stock, lesser cost of goods sold, and greater gross profit during inflation. This is because in an inflationary market when FIFO is applied, the old stock cleared first leaves behind the costlier items in the balance sheet, to be sold at a higher price in the future.

How does FIFO work?

In the process, FIFO enhances the net income as the cheaper older inventory will be used to confirm the current cost of the sold goods. However, the company will have to pay higher taxes for a higher income. The FIFO approach yields a higher value of the final stock, lesser cost of goods sold, and greater gross profit during inflation.

What does FIFO mean in stock valuation?

FIFO in inventory valuation means the company sells the oldest stock first and calculates it COGS based on FIFO. Simply put, FIFO means the company sells the oldest stock first and the newest will be the last one to go for sale. This means, the cheapest stock will be sold first and the costliest stock will be the last;

Why is FIFO so efficient?

Cost-efficient and saves time: FIFO can help save a lot of time and money required to estimate the cost of the inventory being sold. This is because the cost directly depends on the foregoing cash flows of purchases that would be used first.

Why is FIFO important?

It is important to the businesses for the following reasons: Determines cost of goods sold. Provides exact numbers for budgets. Evaluating profitability.

What is FIFO accounting?

FIFO is a method of accounting that assumes that the goods purchased first will be sold first, and it assumes the cost of these goods sold first. FIFO is a widely accepted method across the globe, owing to its efficacy in raising profits.

What is FIFO in business?

Unlike LIFO which is used primarily in the US, FIFO finds approval across the globe. Logical and Easy to understand: FIFO method is easy to understand and convenient to apply for almost all organizations. With a cycle that runs from selling oldest to newest, this model works well for most businesses.

First In First Out

In accounting, First In, First Out (FIFO) is the assumption that a business issues its inventory to its customers in the order in which it has been acquired.

Example 1 (Perpetual)

Bill sells a specific model of a toaster on his website for $12 apiece.

FIFO: Periodic Vs. Perpetual

The example above shows how a perpetual inventory system works when applying the FIFO method.

Example 2 (Periodic)

In the first example, we worked out the value of ending inventory using the FIFO perpetual system at $92.

What is the FIFO method?

Short for first in, first out, the FIFO method is a popular strategy for fulfilling customer orders and assigning costs to your sold inventory for accounting purposes. The first in, first out (or FIFO) method is a strategy for assigning costs to goods sold. Essentially, it means your business sells the oldest items in your inventory first—at least ...

Why is FIFO used?

FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual financial health. Here’s everything you need to know to decide if the FIFO method is right for you.

What is FIFO accounting?

That being said, FIFO is primarily an accounting method for assigning costs to your goods sold. So you don’t necessarily have to actually sell your oldest products first—you just account for the cost of goods sold using the oldest numbers. In other words, when determining your business’s cost of goods sold (COGS), ...

What is the first in first out method?

The first in, first out (or FIFO) method is a strategy for assigning costs to goods sold. Essentially, it means your business sells the oldest items in your inventory first—at least on paper, anyway. FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual ...

Is FIFO better than LIFO?

FIFO is also more transparent and easier to use than LIFO. LIFO systems are easy to manipulate to make it look like your business is doing better than it is. But a FIFO system provides a more accurate reflection of the current value of your inventory. This is one of the reasons why the International Financial Reporting Standards (IFRS) Foundation requires businesses to use FIFO.

What does FIFO mean?

FIFO Meaning, Importance and Example. For any company, there are two possible inventory valuation methods, LIFO and FIFO. Where LIFO stands for last in first out, FIFO, on the other hand, stands for First in first out. In the LIFO method, you sell the latest goods first, and in FIFO, you sell the oldest inventory first.

Does FIFO always give exact cost?

Firstly as prices of the oldest stock will be used to calculate the Cost of goods sold in present times, FIFO does not always give exact cost calculations. Secondly, there is no tax benefit by using FIFO, unlike LIFO, as valuation leads to higher income tax and low cash flow.

What is FIFO in accounting?

FIFO and LIFO are methods used in the cost of goods sold calculation. FIFO (“First-In, First-Out”) assumes that the oldest products in a company’s inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company’s inventory have been sold first ...

Why are FIFO profits more accurate?

Although this may mean less tax for a company to pay under LIFO, it also means stated profits with FIFO are much more accurate because older inventory reflects the actual costs of that inventory. If profits are naturally high under FIFO, then the company becomes that much more attractive to investors.

What is LIFO reserve?

The LIFO reserve is the amount by which a company’s taxable income has been deferred, as compared to the FIFO method. The remaining unsold 350 televisions will be accounted for in “inventory”.

Is LIFO more attractive than FIFO?

You can see how for Ted, the LIFO method may be more attractive than FIFO. This is because the LIFO number reflects a higher inventory cost, meaning less profit and less taxes to pay at tax time. The LIFO reserve in this example is $31,250.

Is LIFO legal in the US?

Under GAAP, LIFO is legal. Outside the United States, LIFO is not permitted as an accounting practice. This is why you’ll see some American companies use the LIFO method on their financial statements, and switch to FIFO for their international operations.

Example of First-In, First-Out

- Company A reported beginning inventories of 100 units at $2/unit. Also, the company made purchases of: 1. 100 units @ $3/unit 2. 100 units @ $4/unit 3. 100 units @ $5/unit If the company sold 250 units, the order of cost expenses would be as follows: As illustrated above, the cost of goods sold (COGS)Cost of Goods Sold (COGS)Cost of Goods Sold (COG...

FIFO vs. LIFO

- To reiterate, FIFO expenses the oldest inventories first. In the following example, we will compare FIFO to LIFO (last in first out)Last-In First-Out (LIFO)The Last-in First-out (LIFO) method of inventory valuation is based on the practice of assets produced or acquired last being the first to be. LIFO expenses the most recent costs first. Consider the same example above. Recall that un…

Impact of FIFO Inventory valuation Method on Financial Statements

- Recall the comparison example of First-In First-Out and LIFO. The two methods yield different inventory and COGS. Now it is important to consider the impact of using FIFO on a company’s financial statements?

Key Takeaways from First-In First-Out

- FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold.

- It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system.

- It provides a poor matching of revenue with expenses.

Related Reading

- CFI is a global provider of financial analyst training and career advancement for finance professionals, including the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll t…