How to calculate LIFO and FIFO?

These are the simple steps that help to convert a LIFO-based statement to a FIFO-based statement:

- First, you have to add the LIFO reserve to LIFO inventory

- Then, you have to deduct the excess cash that saved from lower taxes under LIFO (i:e. ...

- Very next, you have to increase the retained earnings component of shareholders’ equity by the LIFO reserve x (1-T)

- Finally, in the income statement, FIFO COGS = LIFO COGS – Δ LIFO Reserve

What is the difference between FIFO vs. LIFO?

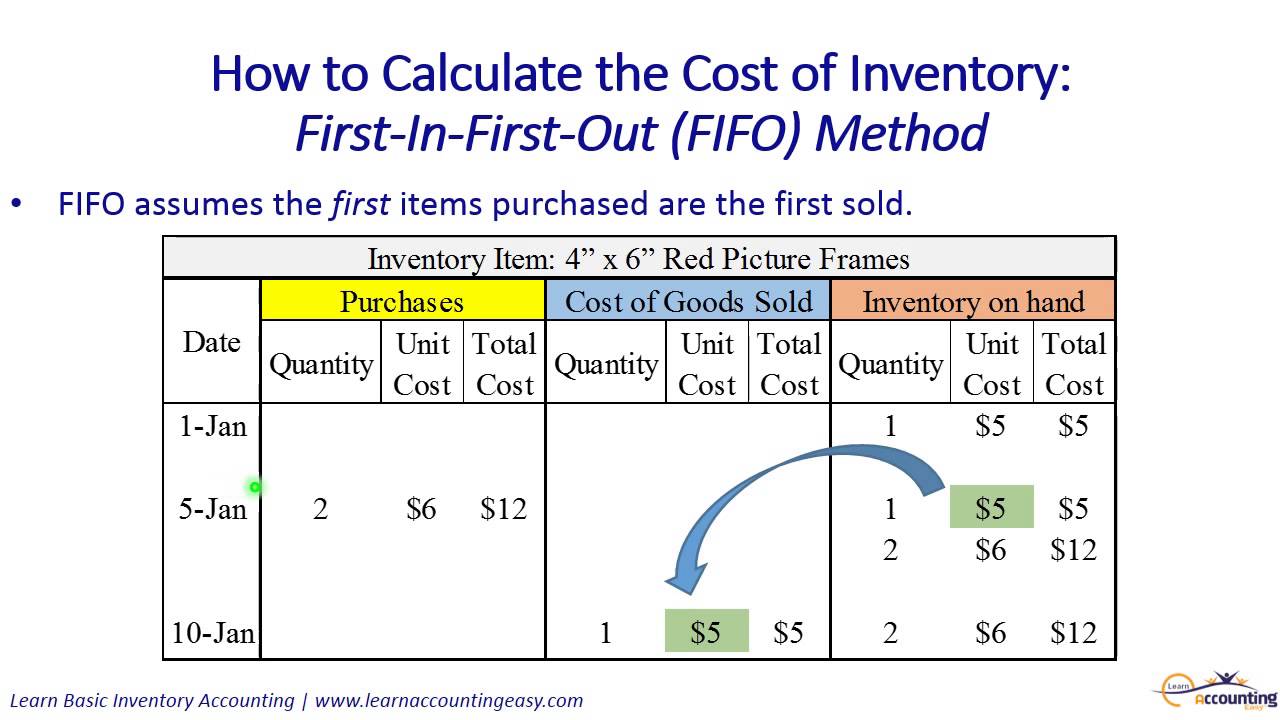

- First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method.

- Last-in, first-out (LIFO) assumes the last inventory added will be the first sold.

- Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

How to calculate cost of goods sold using FIFO method?

Inputs:

- First of all, you just have to enter the quantity of each unit purchases

- Then, you have to add the quantity of the price/unit you purchased

- Also, the lifo fifo method calculator provides you with options of adding more purchases “one by one” or multiple

- Then, you have to enter the total units sold from your number of purchases

What is FIFO inventory management method and why use it?

The advantages to the FIFO method are as follows:

- The method is easy to understand, universally accepted and trusted.

- FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first). ...

- Less waste (a company truly following the FIFO method will always be moving out the oldest inventory first).

What is FIFO method formula?

To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

Why FIFO method is used?

If your inventory costs are going down as time goes on, FIFO will allow you to claim a higher average cost-per-piece on newer inventory, which can help you save money on your taxes. Additionally, FIFO does not require as much recordkeeping as LIFO, because it assumes that older items are gone.

What is the FIFO rule?

FIFO is “first in first out” and simply means you need to label your food with the dates you store them, and put the older foods in front or on top so that you use them first. This system allows you to find your food quicker and use them more efficiently.

What is LIFO and FIFO with example?

First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method. Last-in, first-out (LIFO) assumes the last inventory added will be the first sold. Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

What are the 5 benefits of FIFO?

5 Benefits of FIFO Warehouse StorageIncreased Warehouse Space. Goods can be packed more compactly to free up extra floor space in the warehouse.Warehouse Operations are More Streamlined. ... Keeps Stock Handling to a Minimum. ... Enhanced Quality Control. ... Warranty Control.

What is LIFO method?

Key Takeaways Last in, first out (LIFO) is a method used to account for inventory. Under LIFO, the costs of the most recent products purchased (or produced) are the first to be expensed. LIFO is used only in the United States and governed by the generally accepted accounting principles (GAAP).

What are two differences between FIFO and LIFO?

FIFO (“First-In, First-Out”) assumes that the oldest products in a company's inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company's inventory have been sold first and uses those costs instead.

What is LIFO example?

Example of LIFO that buys coffee mugs from wholesalers and sells them on the internet. One Cup's cost of goods sold (COGS) differs when it uses LIFO versus when it uses FIFO. In the first scenario, the price of wholesale mugs is rising from 2016 to 2019.

What is FIFO accounting?

First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last. An alternative to FIFO, LIFO is an accounting method in which assets purchased or acquired last are disposed of first.

What is FIFO method?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

What is the opposite of FIFO?

The opposite of FIFO is LIFO (Last In, First Out), where the last item purchased or acquired is the first item out. In inflationary economies, this results in deflated net income costs and lower ending balances in inventory when compared to FIFO.

What is FIFO in manufacturing?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense. Under FIFO, it is assumed that the cost of inventory purchased first will be recognized first. The dollar value of total inventory decreases in this process because inventory has been removed from the company’s ownership. The costs associated with the inventory may be calculated in several ways — one being the FIFO method.

Why does the dollar value of total inventory decrease?

The dollar value of total inventory decreases in this process because inventory has been removed from the company’s ownership. The costs associated with the inventory may be calculated in several ways — one being the FIFO method. Typical economic situations involve inflationary markets and rising prices.

How is inventory assigned?

Inventory is assigned costs as items are prepared for sale. This may occur through the purchase of the inventory or production costs, through the purchase of materials, and utilization of labor. These assigned costs are based on the order in which the product was used, and for FIFO, it is based on what arrived first. For example, if 100 items were purchased for $10 and 100 more items were purchased next for $15, FIFO would assign the cost of the first item resold of $10. After 100 items were sold, the new cost of the item would become $15, regardless of any additional inventory purchases made.

What are the advantages of first in first out?

What Are the Advantages of First In, First Out (FIFO)? The obvious advantage of FIFO is that it's most widely used method of valuing inventory globally. It is also the most accurate method of aligning the expected cost flow with the actual flow of goods which offers businesses a truer picture of inventory costs.

What is FIFO expense?

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

What is the benefit of using FIFO?

1. Better valuation of inventory . By using FIFO, the balance sheet shows a better approximation of the market value of inventory. The latest costs for manufacturing or acquiring the inventory are reflected in inventory, and therefore, the balance sheet reflects the approximate current market value.

What is the valuation of goods?

valuation is based on the assumption that the sale or usage of goods follows the same order in which they are bought. In other words, under the first-in, first-out method, the earliest purchased or produced goods are sold/removed and expensed first. Therefore, the most recent costs remain on the balance sheet, while the oldest costs are expensed ...

What is the term for the days required for a business to receive inventory, sell the inventory, and collect cash from

It considers the cost of goods sold, relative to its average inventory for a year or in any a set period of time. Operating Cycle. Operating Cycle An Operating Cycle (OC) refers to the days required for a business to receive inventory, sell the inventory, and collect cash from the sale.

Can you use LIFO in Canada?

Therefore, we can see that the balances for COGS and inventory depend on the inventory valuation method. For income tax purposes in Canada, companies are not permitted to use LIFO. However, US companies are able to use FIFO or LIFO.

What does FIFO mean in inflation?

In a normal inflationary environment, this means that the cost of goods sold will be relatively low in comparison to current costs, which will increase the amount of taxable income; also, the inventory value reported on the balance sheet will approximately match current costs. The FIFO concept also applies to the actual usage of inventory.

Why is FIFO important?

When inventory items have a relatively short life span, it can be of considerable importance to structure the warehousing storage system so that the oldest items are presented to pickers first. Doing so reduces the risk of inventory spoilage.

What is FIFO 2021?

FIFO is an acronym for first in, first out. It is a cost layering concept under which the first goods purchased are assumed to be the first goods sold. The concept is used to devise the valuation of ending inventory, which in turn is used to calculate the cost of goods sold.

How much should ABC inventory be in March?

Based on the FIFO concept, the first ten units that ABC purchased should be charged to the cost of goods sold, on the theory that the first units into inventory should be the first ones removed from it. Thus, the cost of goods sold in March should be $50, while the value of the inventory at the end of March should be $70.

How to determine inventory cost?

As inventory is usually purchased at different rates (or manufactured at different costs) over an accounting period, there is a need to determine what cost needs to be assigned to inventory. For instance, if a company purchased inventory three times in a year at $50, $60 and $70, what cost must be attributed to inventory at the year end? Inventory cost at the end of an accounting period may be determined in the following ways: 1 First In First Out (FIFO) 2 Last In First Out (LIFO) 3 Average Cost Method (AVCO) 4 Actual Unit Cost Method

How is the cost of inventory sold determined?

Theoretically, the cost of inventory sold could be determined in two ways. One is the standard way in which purchases during the period are adjusted for movements in inventory. The second way could be to adjust purchases and sales of inventory in the inventory ledger itself.

What is FIFO in accounting?

FIFO and LIFO are methods used in the cost of goods sold calculation. FIFO (“First-In, First-Out”) assumes that the oldest products in a company’s inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company’s inventory have been sold first ...

Why are FIFO profits more accurate?

Although this may mean less tax for a company to pay under LIFO, it also means stated profits with FIFO are much more accurate because older inventory reflects the actual costs of that inventory. If profits are naturally high under FIFO, then the company becomes that much more attractive to investors.

What is LIFO reserve?

The LIFO reserve is the amount by which a company’s taxable income has been deferred, as compared to the FIFO method. The remaining unsold 350 televisions will be accounted for in “inventory”.

How does inventory affect profits?

The method a company uses to assess their inventory costs will affect their profits. The amount of profits a company declares will directly affect their income taxes . Inventory refers to purchased goods with the intention of reselling, or produced goods (including labor, material & manufacturing overhead costs). FIFO and LIFO are assumptions only.

Is LIFO more attractive than FIFO?

You can see how for Ted, the LIFO method may be more attractive than FIFO. This is because the LIFO number reflects a higher inventory cost, meaning less profit and less taxes to pay at tax time. The LIFO reserve in this example is $31,250.

Can a company use unsold inventory to calculate cost of goods?

Lastly, the product needs to have been sold to be used in the equation. A company cannot apply unsold inventory to the cost of goods calculation.

Is LIFO legal in the US?

Under GAAP, LIFO is legal. Outside the United States, LIFO is not permitted as an accounting practice. This is why you’ll see some American companies use the LIFO method on their financial statements, and switch to FIFO for their international operations.

What is FIFO accounting?

The Bottom Line. First-in, first-out (FIFO) is a popular and GAAP -approved accounting method that companies use to calculate and value their inventory —which, of course, ultimately impacts their earnings. FIFO has several strong points. But it also has drawbacks, most of them related to inflation. Let's look at the disadvantages ...

How does FIFO work?

In the manufacturing world, first-in, first-out (FIFO) is an inventory management/valuation system used during an accounting period to assign costs to a company's goods (including raw materials, goods that are in production, and finished goods that ready for sale). As its name implies, FIFO assumes the first ...

What is the opposite of FIFO?

One alternative accounting method to FIFO is LIFO ( last-in, first-out ). As the name implies, this approach is the opposite of FIFO: The LIFO method assumes goods manufactured or purchased last during a period are the first sold. So, under LIFO, the most recent products are the first to be expensed as cost of goods sold (COGS), which means the lower cost of older products will be reported as ending inventory.

What are the advantages of FIFO?

FIFO has several advantages as an accounting system. Among them: 1 It's easy to understand and use—in fact, it's one of the most widely applied accounting methods out there, both in the U.S. and abroad. 2 It makes it difficult to manipulate figures and income—the cost attached to the unit sold is always the oldest cost. 3 It aligns the expected cost flow with the logical, physical flow of goods (in our example, we sold our older muffins first, remember), offering businesses a truer picture of inventory costs. 4 It's a better indicator of the worth of the ending inventory—the balance sheet amount is likely to approximate the current market value.

Why does LIFO show the largest cost of goods sold?

During periods of inflation, LIFO shows the largest cost of goods sold because the newest costs charged to COGS are also the highest costs. The larger the cost of goods sold, the smaller the net income—and the smaller the tax liability.

What does FIFO mean?

As its name implies, FIFO assumes the first inventory manufactured or purchased during a period is sold first, while the inventory manufactured or produced last is sold last. It's kind of like milk in a grocery store. The milk the store buys first is pushed to the front of the shelf and sold first.

How does FIFO affect net income?

As a result, FIFO can increase net income and inflate profits, because inventory that might be several years old, which was acquired or produced for a lower cost is used to value your expenses.

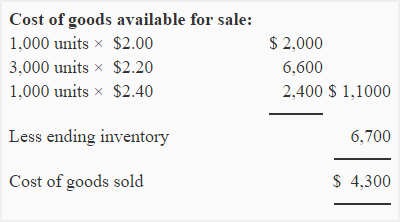

Example of First-In, First-Out

FIFO vs. LIFO

- To reiterate, FIFO expenses the oldest inventories first. In the following example, we will compare FIFO to LIFO (last in first out)Last-In First-Out (LIFO)The Last-in First-out (LIFO) method of inventory valuation is based on the practice of assets produced or acquired last being the first to be. LIFO expenses the most recent costs first. Consider the same example above. Recall that un…

Impact of FIFO Inventory valuation Method on Financial Statements

- Recall the comparison example of First-In First-Out and LIFO. The two methods yield different inventory and COGS. Now it is important to consider the impact of using FIFO on a company’s financial statements?

Key Takeaways from First-In First-Out

- FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold.

- It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system.

- It provides a poor matching of revenue with expenses.

Related Reading

- CFI is a global provider of financial analyst training and career advancement for finance professionals, including the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll t…