What are the disadvantages of the FIFO accounting method?

FIFO, Average Cost ... It is possible for some investors to use the average cost method of accounting, which averages the cost basis for all shares in the portfolio, and taxable gains are ...

What are the pros and cons of FIFO?

What are the disadvantages of the FIFO life?

- Long hours and shift work is undoubtedly one of the toughest aspects of FIFO work. ...

- Most sites are remote, and workers can be exposed to extreme temperatures, dust, pests and harsh terrain. ...

- FIFO can put a lot of stress on families and relationships. ...

- The roster system means it can be very difficult to plan for social events at home. ...

What is the difference between FIFO vs. LIFO?

- First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method.

- Last-in, first-out (LIFO) assumes the last inventory added will be the first sold.

- Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

What are the rules of FIFO?

Theory and Practice on FiFo Lanes – How Does FiFo Work in Lean Manufacturing?

- The Reason for FiFo – Decoupling of Processes. Processes usually have different cycle times needed to process one part. ...

- The Rules for FiFo. The first part that goes into the buffer is also the first part that comes out, hence the name FiFo for First-In-First-Out.

- Advantages of FiFo Lanes. A FiFo lane has quite some advantages. ...

- Examples of FiFo Lanes. ...

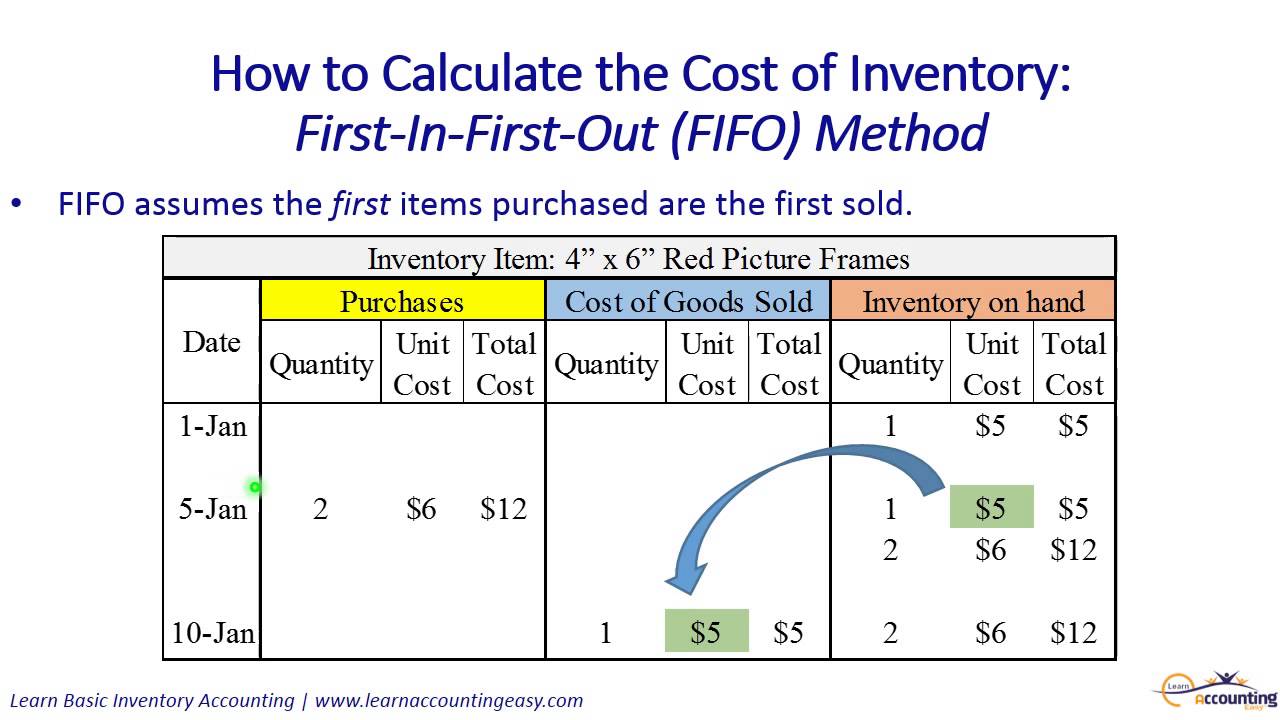

What is FIFO method with example?

The FIFO method requires that what comes in first goes out first. For example, if a batch of 1,000 items gets manufactured in the first week of a month, and another batch of 1,000 in the second week, then the batch produced first gets sold first. The logic behind the FIFO method is to avoid obsolescence of inventory.

What is FIFO and LIFO in cost accounting?

Key Takeaways. The Last-In, First-Out (LIFO) method assumes that the last unit to arrive in inventory or more recent is sold first. The First-In, First-Out (FIFO) method assumes that the oldest unit of inventory is the sold first.

What is the FIFO formula?

To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

What is LIFO in cost accounting?

Last in, first out (LIFO) is a method used to account for inventory. Under LIFO, the costs of the most recent products purchased (or produced) are the first to be expensed. LIFO is used only in the United States and governed by the generally accepted accounting principles (GAAP).

What is LIFO and FIFO explain with an example?

First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method. Last-in, first-out (LIFO) assumes the last inventory added will be the first sold. Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

Why FIFO method is used?

FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first). This makes bookkeeping easier with less chance of mistakes. Less waste (a company truly following the FIFO method will always be moving out the oldest inventory first).

What are the 5 main reasons for using FIFO?

5 Benefits of FIFO Warehouse StorageIncreased Warehouse Space. Goods can be packed more compactly to free up extra floor space in the warehouse.Warehouse Operations are More Streamlined. ... Keeps Stock Handling to a Minimum. ... Enhanced Quality Control. ... Warranty Control.

Which is better LIFO or FIFO?

From a tax perspective, FIFO is more advantageous for businesses with steady product prices, while LIFO is better for businesses with rising product prices.

What is LIFO example?

Example of LIFO that buys coffee mugs from wholesalers and sells them on the internet. One Cup's cost of goods sold (COGS) differs when it uses LIFO versus when it uses FIFO. In the first scenario, the price of wholesale mugs is rising from 2016 to 2019.

Why is LIFO used?

The primary reason that companies choose to use an LIFO inventory method is that when you account for your inventory using the “last in, first out” method, you report lower profits than if you adopted a “first in, first out” method of inventory, known commonly as FIFO.

What is FIFO accounting?

First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last. An alternative to FIFO, LIFO is an accounting method in which assets purchased or acquired last are disposed of first.

What is FIFO in manufacturing?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense. Under FIFO, it is assumed that the cost of inventory purchased first will be recognized first. The dollar value of total inventory decreases in this process because inventory has been removed from the company’s ownership. The costs associated with the inventory may be calculated in several ways — one being the FIFO method.

What is the opposite of FIFO?

The opposite of FIFO is LIFO (Last In, First Out), where the last item purchased or acquired is the first item out. In inflationary economies, this results in deflated net income costs and lower ending balances in inventory when compared to FIFO.

How is inventory assigned?

Inventory is assigned costs as items are prepared for sale. This may occur through the purchase of the inventory or production costs, through the purchase of materials, and utilization of labor. These assigned costs are based on the order in which the product was used, and for FIFO, it is based on what arrived first. For example, if 100 items were purchased for $10 and 100 more items were purchased next for $15, FIFO would assign the cost of the first item resold of $10. After 100 items were sold, the new cost of the item would become $15, regardless of any additional inventory purchases made.

What is FIFO method?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

What are the advantages of first in first out?

What Are the Advantages of First In, First Out (FIFO)? The obvious advantage of FIFO is that it's most widely used method of valuing inventory globally. It is also the most accurate method of aligning the expected cost flow with the actual flow of goods which offers businesses a truer picture of inventory costs.

Why does the dollar value of total inventory decrease?

The dollar value of total inventory decreases in this process because inventory has been removed from the company’s ownership. The costs associated with the inventory may be calculated in several ways — one being the FIFO method. Typical economic situations involve inflationary markets and rising prices.

What does FIFO mean in inflation?

In a normal inflationary environment, this means that the cost of goods sold will be relatively low in comparison to current costs, which will increase the amount of taxable income; also, the inventory value reported on the balance sheet will approximately match current costs. The FIFO concept also applies to the actual usage of inventory.

Why is FIFO important?

When inventory items have a relatively short life span, it can be of considerable importance to structure the warehousing storage system so that the oldest items are presented to pickers first. Doing so reduces the risk of inventory spoilage.

What is FIFO 2021?

FIFO is an acronym for first in, first out. It is a cost layering concept under which the first goods purchased are assumed to be the first goods sold. The concept is used to devise the valuation of ending inventory, which in turn is used to calculate the cost of goods sold.

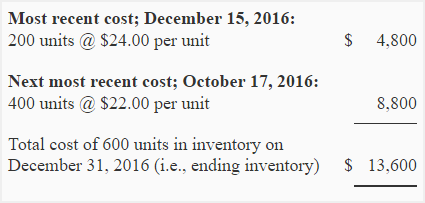

How much should ABC inventory be in March?

Based on the FIFO concept, the first ten units that ABC purchased should be charged to the cost of goods sold, on the theory that the first units into inventory should be the first ones removed from it. Thus, the cost of goods sold in March should be $50, while the value of the inventory at the end of March should be $70.

What is the difference between LIFO and FIFO?

Under FIFO, the cost of goods sold will be lower and the closing inventory will be higher. However, in times of falling prices, the opposite will hold. 2 . FIFO is the default method of determining inventory value.

What is FIFO in 2021?

Updated February 07, 2021. FIFO is one of several ways to calculate the cost of inventory in a business. The other common inventory calculation methods are LIFO (last-in, first-out) and average cost. FIFO, which stands for "first-in, first-out," is an inventory costing method that assumes that the first items placed in inventory are the first sold.

Is inventory cost deductible on taxes?

Like other legitimate business costs, the cost of the products you buy to resell can be deducted from your business income to reduce your taxes.

How to determine inventory cost?

As inventory is usually purchased at different rates (or manufactured at different costs) over an accounting period, there is a need to determine what cost needs to be assigned to inventory. For instance, if a company purchased inventory three times in a year at $50, $60 and $70, what cost must be attributed to inventory at the year end? Inventory cost at the end of an accounting period may be determined in the following ways: 1 First In First Out (FIFO) 2 Last In First Out (LIFO) 3 Average Cost Method (AVCO) 4 Actual Unit Cost Method

How is the cost of inventory sold determined?

Theoretically, the cost of inventory sold could be determined in two ways. One is the standard way in which purchases during the period are adjusted for movements in inventory. The second way could be to adjust purchases and sales of inventory in the inventory ledger itself.

What is FIFO in accounting?

FIFO and LIFO are methods used in the cost of goods sold calculation. FIFO (“First-In, First-Out”) assumes that the oldest products in a company’s inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company’s inventory have been sold first ...

Why are FIFO profits more accurate?

Although this may mean less tax for a company to pay under LIFO, it also means stated profits with FIFO are much more accurate because older inventory reflects the actual costs of that inventory. If profits are naturally high under FIFO, then the company becomes that much more attractive to investors.

What is LIFO reserve?

The LIFO reserve is the amount by which a company’s taxable income has been deferred, as compared to the FIFO method. The remaining unsold 350 televisions will be accounted for in “inventory”.

How does inventory affect profits?

The method a company uses to assess their inventory costs will affect their profits. The amount of profits a company declares will directly affect their income taxes . Inventory refers to purchased goods with the intention of reselling, or produced goods (including labor, material & manufacturing overhead costs). FIFO and LIFO are assumptions only.

Is LIFO more attractive than FIFO?

You can see how for Ted, the LIFO method may be more attractive than FIFO. This is because the LIFO number reflects a higher inventory cost, meaning less profit and less taxes to pay at tax time. The LIFO reserve in this example is $31,250.

Can a company use unsold inventory to calculate cost of goods?

Lastly, the product needs to have been sold to be used in the equation. A company cannot apply unsold inventory to the cost of goods calculation.

Is LIFO legal in the US?

Under GAAP, LIFO is legal. Outside the United States, LIFO is not permitted as an accounting practice. This is why you’ll see some American companies use the LIFO method on their financial statements, and switch to FIFO for their international operations.