How to calculate cost of goods sold using FIFO method?

Inputs:

- First of all, you just have to enter the quantity of each unit purchases

- Then, you have to add the quantity of the price/unit you purchased

- Also, the lifo fifo method calculator provides you with options of adding more purchases “one by one” or multiple

- Then, you have to enter the total units sold from your number of purchases

Which is a better method LIFO or FIFO?

FIFO assumes that cheaper items are sold first, generating a higher profit than LIFO. However, when the more expensive items are sold in later months, profit is lower. LIFO generates lower profits in early periods and more profit in later months. FIFO is the easier method to use, and most businesses stick with the FIFO method.

Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

What is FIFO inventory costing and why use it?

It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company’s inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation. How Do You Calculate FIFO? What Are the Advantages of FIFO?

What is FIFO method with example?

Example of FIFO Imagine if a company purchased 100 items for $10 each, then later purchased 100 more items for $15 each. Then, the company sold 60 items. Under the FIFO method, the cost of goods sold for each of the 60 items is $10/unit because the first goods purchased are the first goods sold.

What is the FIFO method formula?

To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

Why is FIFO the best method?

FIFO is more likely to give accurate results. This is because calculating profit from stock is more straightforward, meaning your financial statements are easy to update, as well as saving both time and money. It also means that old stock does not get re-counted or left for so long it becomes unusable.

What is FIFO method in business?

FIFO (first in, first out) inventory management seeks to sell older products first so that the business is less likely to lose money when the products expire or become obsolete. LIFO (last in, first out) inventory management applies to nonperishable goods and uses current prices to calculate the cost of goods sold.

What is FIFO and LIFO example?

Ending Inventory per LIFO: 1,000 units x $8 = $8,000. Remember that the last units in (the newest ones) are sold first; therefore, we leave the oldest units for ending inventory. Ending Inventory per FIFO: 1,000 units x $15 each = $15,000.

How do you calculate cost of goods sold FIFO?

For the sale of 250 units: 100 units at $2/unit = $200 in COGS. 100 units at $3/unit = $300 in COGS. 50 units at $4/unit = $200 in COGS....Example of First-In, First-Out (FIFO)100 units @ $3/unit.100 units @ $4/unit.100 units @ $5/unit.

What are the advantages and disadvantages of FIFO method?

This method is useful for materials which are subject to obsolescence and deterioration In periods of rising prices, the FIFO method produces higher profits and results in higher tax liability because lower cost is charged to production Conversely in periods of falling, prices.

Which company uses FIFO method?

Just to name a few examples, Dell Computer (NASDAQ:DELL) uses FIFO. General Electric (NYSE:GE) uses LIFO for its U.S. inventory and FIFO for international. Teen retailer Hot Topic (NASDAQ:HOTT) uses FIFO. Wal-Mart (NYSE:WMT) uses LIFO.

Why do businesses use FIFO?

If your inventory costs are going down as time goes on, FIFO will allow you to claim a higher average cost-per-piece on newer inventory, which can help you save money on your taxes. Additionally, FIFO does not require as much recordkeeping as LIFO, because it assumes that older items are gone.

What is FIFO in accounting?

FIFO is the default method of determining inventory value. If you want to use LIFO, you must meet some specific requirements and file an application using IRS Form 970.

What is the difference between LIFO and FIFO?

Under FIFO, the cost of goods sold will be lower and the closing inventory will be higher. However, in times of falling prices, the opposite will hold. 2 . FIFO is the default method of determining inventory value.

What is FIFO in 2021?

Updated February 07, 2021. FIFO is one of several ways to calculate the cost of inventory in a business. The other common inventory calculation methods are LIFO (last-in, first-out) and average cost. FIFO, which stands for "first-in, first-out," is an inventory costing method that assumes that the first items placed in inventory are the first sold.

What is the cost of goods sold?

At the end of the year, you want to record the cost of the inventory you've sold, as an expense of doing business, which is deducted from your sales. This calculation is called the cost of goods sold .

What is FIFO method?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

What is FIFO accounting?

First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last. An alternative to FIFO, LIFO is an accounting method in which assets purchased or acquired last are disposed of first.

What Are the Advantages of First In, First Out (FIFO)?

The obvious advantage of FIFO is that it's the most widely used method of valuing inventory globally. It is also the most accurate method of aligning the expected cost flow with the actual flow of goods which offers businesses a truer picture of inventory costs . Furthermore, it reduces the impact of inflation, a ssuming that the cost of purchas ing newer inventory will be higher than the purchasing cost of older invent ory. Finally, it reduces the obsolescence of inventory.

What happens when FIFO assigns the oldest costs to the cost of goods sold?

In this situation, if FIFO assigns the oldest costs to the cost of goods sold, these oldest costs will theoretically be priced lower than the most recent inventory purchased at current inflated prices. This lower expense results in higher net income. Also, because the newest inventory was purchased at generally higher prices, the ending inventory balance is inflated.

What is FIFO in manufacturing?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense. Under FIFO, it is assumed that the cost of inventory purchased first will be recognized first. The dollar value of total inventory decreases in this process because inventory has been removed from the company’s ownership. The costs associated with the inventory may be calculated in several ways — one being the FIFO method.

How to calculate average cost?

The average cost method is calculated by dividing the cost of goods in inventory by the total number of items available for sale. This results in net income and ending inventory balances between FIFO and LIFO.

What Are the Other Inventory Valuation Methods?

In inflationary economies, this results in deflated net income costs and lower ending balances in inventory when compared to FIFO. Average cost inventory is another method that assigns the same cost to each item and results in net income and ending inventory balances between FIFO and LIFO. Finally, specific inventory tracing is used only when all components attributable to a finished product are known.

Why use the FIFO method?

With the FIFO method, you sell those older products first—ens uring that all items in your inventory are as recent as possible.

What is FIFO accounting?

That being said, FIFO is primarily an accounting method for assigning costs to your goods sold. So you don’t necessarily have to actually sell your oldest products first—you just account for the cost of goods sold using the oldest numbers. In other words, when determining your business’s cost of goods sold (COGS), ...

Why is the FIFO method better than the LIFO method?

Because of inflation, businesses using the FIFO method are often able to report higher profit margins than companies using the last in, first out (LIFO) method. That’s because the FIFO method matches older, lower-cost inventory items with higher current- cost revenue. Businesses on the LIFO system, on the other hand, see less of a margin between their current costs and their current revenue.

What is the first in first out method?

The first in, first out (or FIFO) method is a strategy for assigning costs to goods sold. Essentially, it means your business sells the oldest items in your inventory first—at least on paper, anyway. FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual ...

How many items were in the first sale of the FIFO?

The first sale (on October 9) consisted of 150 items—more than the first purchase order (or FIFO layer) included. So we applied the cost of the 100 items in the first FIFO layer to the first 100 items in the sales order. The cost of the remaining 50 items was taken from the next-oldest purchase order (FIFO layer 2).

Why is FIFO used?

FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual financial health. Here’s everything you need to know to decide if the FIFO method is right for you.

What is cost of goods sold?

Cost of goods sold (COGS) is a metric used by businesses to calculate their profit margins —an important way to gauge your company’s success. The trick is that inventory costs can vary a lot depending on when you ordered the product, the number of items you ordered, and the supplier you ordered from.

Why is FIFO accounting used?

FIFO method of accounting saves time, and money spends in calculating the exact inventory cost that is being sold because the recording of inventory is done in the same order as they are purchased or produced. Easy to understand.

What is FIFO valuation?

Under the FIFO method of accounting inventory valuation, the goods which are purchased at the earliest are the first one to be removed from the inventory account. This results in remaining inventory at books to be valued at the most recent price for which the last stock of inventory is purchased. This results in inventory assets recorded on the balance sheet at the most recent costs.

What are the disadvantages of FIFO accounting?

One of the biggest disadvantages of FIFO accounting method is inventory valuation during inflation, First In First Out method will result in higher profits, and thus will results in higher “Tax Liabilities” in that particular period. This may result in increased tax charges and higher tax-related cash outflows.

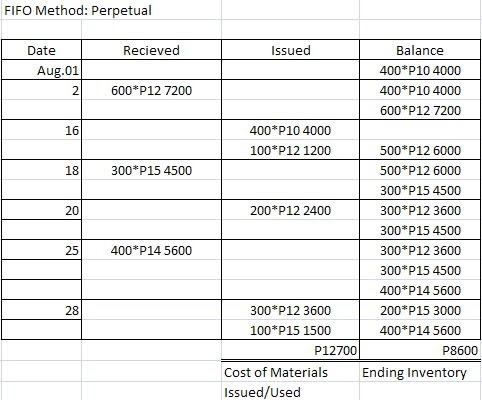

What method does ABC use for inventory valuation?

ABC Corporation uses the FIFO method of inventory valuation for the month of December. During that month, it records the following transactions:

What is the ending inventory formula?

Ending Inventory The ending inventory formula computes the total value of finished products remaining in stock at the end of an accounting period for sale. It is evaluated by deducting the cost of goods sold from the total of beginning inventory and purchases. read more

Which method of inventory valuation gives the most accurate calculation of the inventory and sales profit?

A business which is in the trading of perishable items generally sells the items which are purchased earliest first, FIFO method of inventory valuation generally gives the most accurate calculation of the inventory and sales profit. Other examples include retail businesses that sell foods or other products with an expiration date.

How are inventory costs reported?

Inventory costs are reported either on the balance sheet, or they are transferred to the income statement as an expense to match against sales revenue. When inventories are used up in production or are sold, their cost is transferred from the balance sheet to the income statement as cost of goods sold.

Why use LIFO method?

For some companies, there are benefits to using the LIFO method for inventory costing. For example, those companies that sell goods that frequently increase in price might use LIFO to achieve a reduction in taxes owed.

Why is the average cost method important?

The simplicity of the average cost method is one of its main benefits. It takes less time and labor to implement an average cost method , thereby reducing company costs. The method works best for companies that sell large numbers of relatively similar products.

What is the first in first out method?

Companies frequently use the first in, first out (FIFO) method to determine the cost of goods sold or COGS. The FIFO method assumes the first products a company acquires are also the first products it sells. The company will report the oldest costs on its income statement, whereas its current inventory will reflect the most recent costs. FIFO is a good method for calculating COGS in a business with fluctuating inventory costs.

How to find average cost of goods sold?

This amount is then divided by the number of items the company purchased or produced during that same period . This gives the company an average cost per item. To determine the cost of goods sold, the company then multiplies the number of items sold during the period by the average cost per item.

Is FIFO a good method for calculating COGS?

FIFO is a good method for calculating COGS in a business with fluctuating inventory costs. While the LIFO inventory valuation method is accepted in the United States, it is considered controversial and prohibited by the International Financial Reporting Standards (IFRS).

Is FIFO cash flow assumption accurate?

While an actual sales pattern may not follow the FIFO cash flow assumption exactly, it is still an accurate method for determining COGS and allowed by both generally accepted accounting principles (GAAP) and International Financial Reporting Standards (IFRS).

How to represent issues out of inventory?

Issues out of inventory are represented by vertical arrows below the timeline.

Do you have to use FIFO when you have an inventory?

When you use FIFO, you don’t have to use the FIFO rule.