Comparison Chart

| Basis for Comparison | LIFO | FIFO |

| Meaning | LIFO is an inventory valuation technique ... | FIFO is an inventory valuation technique ... |

| Stock in hand | Represents the oldest stock | Represents the latest stock |

| Current market price | Shown by the cost of goods sold | Shown by the cost of unsold stock |

| Restrictions | IFRS, does not recommend the use of LIFO ... | No such restriction |

Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

Which is a better method LIFO or FIFO?

FIFO assumes that cheaper items are sold first, generating a higher profit than LIFO. However, when the more expensive items are sold in later months, profit is lower. LIFO generates lower profits in early periods and more profit in later months. FIFO is the easier method to use, and most businesses stick with the FIFO method.

How do you calculate FIFO, and LIFO?

These are the simple steps that help to convert a LIFO-based statement to a FIFO-based statement:

- First, you have to add the LIFO reserve to LIFO inventory

- Then, you have to deduct the excess cash that saved from lower taxes under LIFO (i:e. ...

- Very next, you have to increase the retained earnings component of shareholders’ equity by the LIFO reserve x (1-T)

- Finally, in the income statement, FIFO COGS = LIFO COGS – Δ LIFO Reserve

How to determine which shares to sell, FIFO or LIFO?

How to Determine Which Shares to Sell, FIFO or LIFO

- FIFO vs LIFO Stock Trades. The first-in, first-out method is the default way to decide which shares to sell. ...

- Tell Your Broker. If you plan to use any method besides FIFO, including LIFO, you must specifically direct your broker as to which shares to sell so that your taxes ...

- 2018 Tax Law Changes. ...

- 2017 Tax Law. ...

What is LIFO and FIFO with example?

First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method. Last-in, first-out (LIFO) assumes the last inventory added will be the first sold. Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

What is the difference between LIFO and FIFO which one is most preferred and why?

FIFO focuses on using up old stock first, whilst LIFO uses the newest stock available. LIFO helps keep tax payments down, but FIFO is much less complicated and easier to work with. However, it is all down to the company you own as to what method you choose.

What is FIFO example?

Example of FIFO Imagine if a company purchased 100 items for $10 each, then later purchased 100 more items for $15 each. Then, the company sold 60 items. Under the FIFO method, the cost of goods sold for each of the 60 items is $10/unit because the first goods purchased are the first goods sold.

What is the difference between LIFO?

LiPos offers several performance enhancements compared with Li-ions, including higher energy density and lighter-weight batteries. In addition, LiPos can be produced in a wider variety of shapes and sizes. However, today's LiPos use gelled membranes, not fully solid polymer electrolytes (SPEs).

What is LIFO example?

Example of LIFO that buys coffee mugs from wholesalers and sells them on the internet. One Cup's cost of goods sold (COGS) differs when it uses LIFO versus when it uses FIFO. In the first scenario, the price of wholesale mugs is rising from 2016 to 2019.

What is the difference between Fefo and FIFO?

FIFO stands for First In, First Out, this is when the stock that was first in the warehouse should be taken out first and used first. This will help ensure that the least amount of food will pass its expiration date. On the other hand, FEFO stands for First Expired, First Out.

What is LIFO method?

Key Takeaways Last in, first out (LIFO) is a method used to account for inventory. Under LIFO, the costs of the most recent products purchased (or produced) are the first to be expensed. LIFO is used only in the United States and governed by the generally accepted accounting principles (GAAP).

What is FIFO formula?

To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

Why is FIFO used?

FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first). This makes bookkeeping easier with less chance of mistakes. Less waste (a company truly following the FIFO method will always be moving out the oldest inventory first).

What is LIFO method?

LIFO. When sales are recorded using the LIFO method, the most recent items of inventory are used to value COGS and are sold first. In other words, the older inventory, which was cheaper, would be sold later.

What is FIFO in accounting?

The First-In, First-Out (FIFO) method assumes that the first unit making its way into inventory–or the oldest inventory–is the sold first. For example, let's say that a bakery produces 200 loaves of bread on Monday at a cost of $1 each, and 200 more on Tuesday at $1.25 each. FIFO states that if the bakery sold 200 loaves on Wednesday, the COGS ( on the income statement) is $1 per loaf because that was the cost of each of the first loaves in inventory. The $1.25 loaves would be allocated to ending inventory ( on the balance sheet ).

Why is LIFO not accurate?

As a result, LIFO doesn't provide an accurate or up-to-date value of inventory because the valuation is much lower than inventory items at today's prices.

Why would COGS be higher under LIFO?

In an inflationary environment, the current COGS would be higher under LIFO because the new inventory would be more expensive. As a result, the company would record lower profits or net income for the period. However, the reduced profit or earnings means the company would benefit from a lower tax liability.

Why is FIFO better than COGS?

FIFO can be a better indicator of the value for ending inventory because the older items have been used up while the most recently acquired items reflect current market prices. For most companies, FIFO is the most logical choice since they typically use their oldest inventory first in the production of their goods, which means the valuation of COGS reflects their production schedule.

When sales are recorded using the FIFO method, what is the oldest inventory?

When sales are recorded using the FIFO method, the oldest inventory–that was acquired first–is used up first. FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet.

Can seafood companies leave their inventory idle?

In other words, the seafood company would never leave their oldest inventory sitting idle since the food could spoil, leading to losses. As a result, LIFO isn't practical for many companies that sell perishable goods and doesn't accurately reflect the logical production process of using the oldest inventory first.

How to compare FIFO and LIFO?

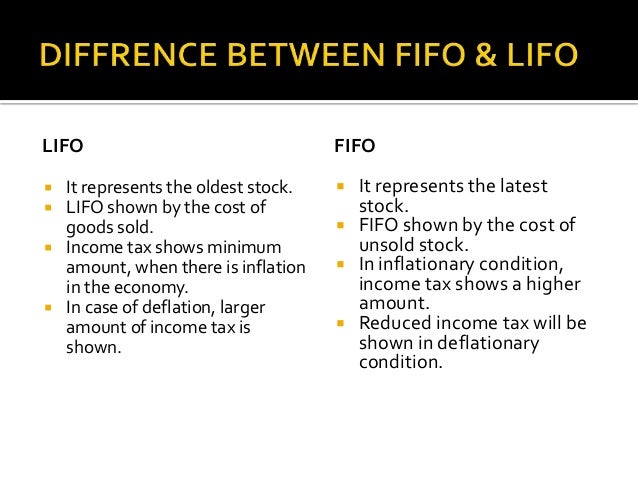

The points given below explain the fundamental differences between LIFO and FIFO methods of inventory valuation: 1 A method of stock valuation in which last received lot in hand is issued first is known as LIFO. FIFO is a short form for First in, first out in which the inventory produced or purchased first, is disposed off or sold out first. 2 In LIFO, the stock in hand represents, oldest stock while in FIFO, the stock in hand is the latest lot of goods. 3 In LIFO, the cost of goods sold (COGS) shows current market price while in the case of FIFO the cost of unsold stock shows current market price. 4 As per International Financial Reporting Framework, LIFO method is not permissible for valuing inventory, which is not in the case of a FIFO. 5 When there is an inflationary trend in the country’s economy, LIFO will show a correct profit and thus help in tax saving. However, it is just opposite in FIFO. 6 In FIFO, a little number of records are being maintained, unlike LIFO.

What does LIFO mean?

Meaning. LIFO is an inventory valuation technique, in which the last received stock of goods is issued first. FIFO is an inventory valuation technique, in which the first received stock of goods is issued first. Stock in hand. Represents the oldest stock.

Why is LIFO not used?

Due to irrational assumptions , LIFO is not used nowadays as it handles the latest stock in hand first which is unfair because the earliest stock stands in the queue. FIFO is very simple to understand as well as to operate. It shows the correct picture when there is a fall in the price. s of goods. Related Differences.

What is FIFO in business?

Definition of FIFO. An asset management technique, in which the actual issue or sale of goods from the stores is made from the oldest lot on hand is known as First in, first out or FIFO. It follows a chronological order, i.e. it first disposes of the item that is placed in the inventory first.

What is the last in first out method?

Last in, first out or LIFO, is a method of accounting for valuing inventory. This method is based on the assumption that the last item placed in the inventory will be sold out first, i.e. reverse chronological order will be followed in issuing inventory from the stores.

Is LIFO a FIFO?

As per International Financial Reporting Framework, LIFO method is not permissible for valuing inventory, which is not in the case of a FIFO. When there is an inflationary trend in the country’s economy, LIFO will show a correct profit and thus help in tax saving. However, it is just opposite in FIFO.

Why use FIFO vs LIFO?

FIFO vs. LIFO for flow of goods. Many companies choose to use FIFO because it more closely mimics the actual flow of goods in and out of inventory. It's considered a simpler system with less spoilage and waste of materials.

Why is FIFO higher than LIFO?

Because the cost of goods sold is usually higher under LIFO, this decreases a company's reported profits, which can lower the amount of tax liability. Conversely, FIFO valuations present a higher tax liability because the cost of goods sold is lower. Read more: FIFO Accounting: What It Is and What You Need To Know.

What is a fifo and a fifo?

While both FIFO and LIFO are a way to manage inventory, the marketable goods produced by a company usually dictate which method to choose. FIFO is typically used for perishable products like food and beverages or stock that may become obsolete if it isn't sold within a certain period of time. LIFO however is often used for products that aren't affected by the amount of time spent in inventory or where the flow of product fits the LIFO method.

How is FIFO inventory calculated?

FIFO inventory cost is calculated by determining the cost of the oldest stock and multiplying that amount by the number of items sold.

What is FIFO in inventory?

What is FIFO? First in, first out is a method to value inventory and calculate the cost of goods sold. FIFO items are the oldest products in an inventory because they were the first stock to be added after purchase or production. FIFO uses the principle that when items are acquired first, they are also sold first.

What is LIFO method?

Using the LIFO method, more recent stock can be valued higher than older goods when there is a price increase. LIFO works well using the matching principle, which is used to charge costs along with revenues during the same period of inventory calculations. Read more: A Guide To the Inflation Rate.

What is the last in first out approach?

Last in, first out is another way to manage inventory and calculate profits from goods. In this approach, businesses figure that the most recent inventory is the first sold. This means that older stock continues to sit for longer periods before being sold.

What is the difference between FIFO and LIFO?

Here are the main differences between FIFO and LIFO: 1 The FIFO method assumes that the oldest stocks are sold or used in production first. 2 The LIFO method assumes that the most recent purchases or the newest inventory to arrive is sold or used in production first. 3 The FIFO method is an accepted practice around the world, approved by both GAAP and IFRS. 4 The LIFO method is allowed by GAAP but prohibited by IFRS. 5 The FIFO method follows the natural flow of inventory and a logical approach to avoid inventory losses through obsolescence — expired or stale goods for production or sale. 6 The LIFO method can cause inventory losses from obsolete or spoiled goods.

Why is FIFO more transparent than LIFO?

Since most businesses don't want expired or stale products and strive to use or sell the oldest stocks first, FIFO follows the natural flow of inventory. The simple process prevents mistakes in bookkeeping. This is why the FIFO method is said to be more transparent compared to LIFO.

What is LIFO reserve?

public companies must publish what's known as LIFO reserves in the footnotes of their financial statements. LIFO reserves represent the difference between ending inventory under LIFO and under another system, which is usually FIFO.

What is FIFO in accounting?

First In, First Out (FIFO) is an inventory management and valuation method . It assumes that the oldest inventory produced or purchased are sold or used in production first. The FIFO method uses the cost of the oldest stocks to calculate the cost of goods sold (COGS), which is recorded in the income statement.

Why is FIFO used?

Under the FIFO method, the possibility of a higher profit is greater since the COGS is calculated using the price of the oldest inventories (which are generally acquired for lower costs). Businesses that use FIFO report higher net incomes when market prices increase. This is why FIFO is said to give a clearer picture of a business's profitability and growth.#N#Proponents of FIFO also claim that it's a better measure for valuing inventory on hand. It uses the per-unit cost of the most recent purchases, which ties to the current market value of the products.

Why is FIFO important?

This is why FIFO is said to give a clearer picture of a business's profitability and growth. Proponents of FIFO also claim that it's a better measure for valuing inventory on hand. It uses the per-unit cost of the most recent purchases, which ties to the current market value of the products.

What is the benefit of using the LIFO method?

Lower profit means lower tax liability, which is the greatest advantage of using the LIFO method. Since the LIFO method allows a business to lower its income tax, this also means less cash outlay and a higher cash flow for the company.

What is a FIFO?

FIFO is mostly recommended for businesses that deal in perishable products. The approach provides such ventures with a more accurate value of their profits and inventory. FIFO is not only suited for companies that deal with perishable items but also those that don’t fall under the category.

What is LIFO system?

The LIFO system is founded on the assumption that the latest items to be stored are the first items to be sold. It is a recommended technique for businesses dealing in products that are not perishable or ones that don’t face the risk of obsolescence.

How does LIFO work?

Apart from reducing the tax liability, using the LIFO technique offers other benefits, such as: 1 It complies better with the matching principle, as it charges costs with the revenues of a similar period 2 Reduces the likelihood of write-downs of inventory if their fair market value has decreased 3 In some industries, it conforms with the actual physical flow of inventory, such as in extraction industries (i.e., coal, oil and gas)

What are the benefits of LIFO?

Apart from reducing the tax liability, using the LIFO technique offers other benefits, such as: It complies better with the matching principle, as it charges costs with the revenues of a similar period. Reduces the likelihood of write-downs of inventory if their fair market value has decreased.

What is the LIFO method?

Whenever there are price increases, such as in an inflationary period, the LIFO method has the impact of recording the sale of higher-priced items first while the cheaper, older products are maintained as stock. Doing so causes a firm’s cost of goods sold to increase and the net income to decrease.

What are the drawbacks of LIFO?

One of its drawbacks is that it does not correspond to the normal physical flow of most inventories. Also, the LIFO approach tends to understate the value of the closing stock and overstate COGS, which is not accepted by most taxation authorities.

What are the advantages of FIFO?

The biggest advantage of FIFO lies in its simplicity. It is easy to use, generally accepted and trusted, and it follows the natural physical flow of inventory. Another advantage is that there’s less wastage when it comes to the deterioration of materials.

What is the difference between "last in first out" and "last in first out"?

Last in First out is used to defer the payment of income taxes. First in First out implies the inventory which was added first will be removed first from the stock. Last in First out, on the other hand, implies inventory that was added last to the stock will be removed first.

Is inflation the same as last year?

The answer is yes. It’s the inflation, because of which arises the need of having more than one accounting method. As if, the cost of material or goods purchase was the same today and last year, the cost of material would be equal to what was purchased last year.

Understanding the inventory formula

Beginning inventory + purchases = goods available for sale – cost of goods sold (COGS) = ending inventory

How are FIFO and LIFO methods different?

FIFO and LIFO inventory valuations differ because each method makes a different assumption about the units sold. To understand FIFO vs. LIFO flow of inventory, you need to visualize inventory items sitting on the shelf, each with a cost assigned to it.

How do you calculate FIFO and LIFO?

To explain inventory valuation in detail, assume that Sterling Fashions sells a line of men’s shirts and that the store had no beginning inventory balance on March 1st. Here is the inventory activity for March:

How do FIFO and LIFO affect more straightforward accounting operations?

Using FIFO simplifies the accounting process because the oldest items in inventory are assumed to be sold first. When Sterling uses FIFO, all of the $50 units are sold first, followed by the items at $54.

Industry, regulatory and tax considerations

Accountants use “inventoriable costs” to define all expenses required to obtain inventory and prepare the items for sale. For retailers and wholesalers, the largest inventoriable cost is the purchase cost.

Final thoughts

The FIFO and LIFO methods impact your inventory costs, profit, and your tax liability. Keep your accounting simple by using the FIFO method of accounting, and discuss your company’s regulatory and tax issues with a CPA.

What is the difference between FIFO and LIFO?

FIFO is very appealing to companies looking to bolster their attractiveness to investors and lenders. LIFO is appealing to companies looking to reduce their tax liability and do not prioritize either investment or obtaining credit at the best possible rates during periods of inflation.

What is FIFO in accounting?

Higher earnings and net worth appeal to investors. Essentially speaking, FIFO is for those who want maximum compatibility with accounting and legal requirements while enjoying higher profits and net worth during inflation (and enduring the risk of lower net worth and angry investors during deflation).

What is LIFO in inventory management?

While not as frequently used as FIFO, the LIFO method remains a valuable strategic tool for businesses looking to optimize their COGS and ending inventory. Unlike FIFO, under LIFO the last items to enter inventory are sold first; items leave inventory in reverse order of their arrival.

What is FIFO in inventory?

First-In, First-Out (FIFO) Commonly used by businesses carrying physical inventory of some kind, FIFO operates on the assumption that the first items added to inventory are also the first ones sold. Under FIFO, items leave inventory in the same order they arrived.

Is FIFO a GAAP?

FIFO is compatible with both the generally accepted accounting principles (GAAP) used by businesses operating exclusively in the United States and the International Financial Reporting Standards (IFRS) used by companies doing business outside the United States.

Is LIFO a GAAP method?

Also unlike FIFO, the LIFO method is acceptable only under GAAP and is not recognized by IFRS. Using LIFO is strategically valuable during times of inflation, as goods sold first are also the most expensive. This increases COGS and reduces profits—which also reduces income tax liability.

What is FIFO accounting?

The first in, first out (FIFO) accounting method relies on a cost flow assumption that removes costs from the inventory account when an item in someone’s inventory has been purchased at varying costs, over time. When a business uses FIFO, the oldest cost of an item in an inventory will be removed first when one of those items is sold. This oldest cost will then be reported on the income statement as part of the cost of goods sold.

Does LIFO match the flow of costs?

It should be understood that, although LIFO matches the most recent costs with sales on the income statement, the flow of costs does not necessarily have to match the flow of the physical units. Generally speaking, FIFO is preferable in times of rising prices, so that the costs recorded are low, and income is higher.