What is LIFO and FIFO with example?

First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method. Last-in, first-out (LIFO) assumes the last inventory added will be the first sold. Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

How is FIFO calculated?

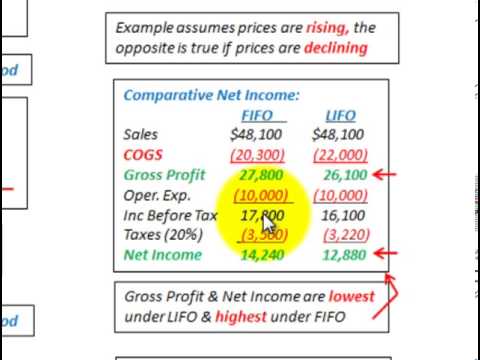

To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

What is LIFO accounting?

Last in, first out (LIFO) is a method used to account for inventory. Under LIFO, the costs of the most recent products purchased (or produced) are the first to be expensed. LIFO is used only in the United States and governed by the generally accepted accounting principles (GAAP).

What is difference between FIFO and LIFO?

Key Takeaways. The Last-In, First-Out (LIFO) method assumes that the last unit to arrive in inventory or more recent is sold first. The First-In, First-Out (FIFO) method assumes that the oldest unit of inventory is the sold first.

What is FIFO example?

Example of FIFO Imagine if a company purchased 100 items for $10 each, then later purchased 100 more items for $15 each. Then, the company sold 60 items. Under the FIFO method, the cost of goods sold for each of the 60 items is $10/unit because the first goods purchased are the first goods sold.

Why FIFO method is used?

If your inventory costs are going down as time goes on, FIFO will allow you to claim a higher average cost-per-piece on newer inventory, which can help you save money on your taxes. Additionally, FIFO does not require as much recordkeeping as LIFO, because it assumes that older items are gone.

Why would a company use FIFO instead of LIFO?

Reason for Using FIFO Instead of LIFO If a U.S. corporation's cost of inventory items are continuously increasing and the corporation has been experiencing operating losses and negative taxable income, the use of FIFO means matching its oldest/lower costs with its current sales.

Is FIFO allowed under GAAP?

One of the most basic differences is that GAAP permits the use of all three of the most common methods for inventory accountability—weighted-average cost method; first in, first out (FIFO); and last in, first out (LIFO)—while the IFRS forbids the use of the LIFO method.

What type of companies use FIFO?

Many companies that sell perishable commodities such as food or flowers use FIFO inventory tracking. Given that inventory has a limited shelf life in these industries, the FIFO method reduces losses.

What is LIFO example?

Example of LIFO that buys coffee mugs from wholesalers and sells them on the internet. One Cup's cost of goods sold (COGS) differs when it uses LIFO versus when it uses FIFO.

Why LIFO is not allowed?

IFRS prohibits LIFO due to potential distortions it may have on a company's profitability and financial statements. For example, LIFO can understate a company's earnings for the purposes of keeping taxable income low. It can also result in inventory valuations that are outdated and obsolete.

Why is LIFO used?

The primary reason that companies choose to use an LIFO inventory method is that when you account for your inventory using the “last in, first out” method, you report lower profits than if you adopted a “first in, first out” method of inventory, known commonly as FIFO.