If your inventory costs are going up, or are likely to increase, LIFO costing may be better because the higher cost items (the ones purchased or made last) are considered to be sold. This results in higher costs and lower profits. If the opposite is true, and your inventory costs are going down, FIFO costing might be better.

Why would a company use LIFO instead of FIFO?

Key Takeaway

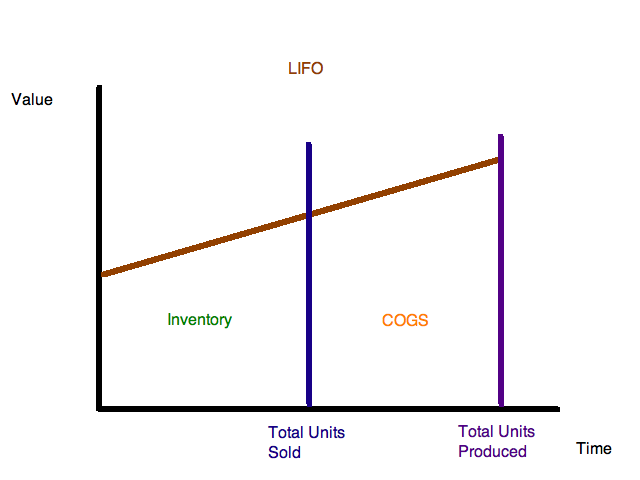

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

Which companies use LIFO method?

To complete the election application, you will need to:

- Specify the goods to which the LIFO method will apply,

- Identify and describe the inventory method (s) you used in the prior year to value these goods, and

- Explain what goods the LIFO method will NOT be used for.

What is LIFO method with example?

The advantages of LIFO method are as follows:

- LIFO method is easy to implement and understand.

- It provides tax benefits to the business organisations by reporting less profits and deferring Income Tax payment in the future years.

- LIFO method provides the benefit of matching the current cost with the current revenues thereby reducing the profits included in the inventory.

What does LIFO and FIFO mean?

Understanding LIFO and FIFO

- First-In, First-Out (FIFO) The First-In, First-Out (FIFO) method assumes that the first unit making its way into inventory–or the oldest inventory–is the sold first.

- Last-In, First-Out (LIFO) The Last-In, First-Out (LIFO) method assumes that the last or moreunit to arrive in inventory is sold first.

- Average Cost. ...

Why LIFO is better than FIFO?

FIFO focuses on using up old stock first, whilst LIFO uses the newest stock available. LIFO helps keep tax payments down, but FIFO is much less complicated and easier to work with.

Is LIFO or FIFO better for net income?

Since inventory costs have increased in recent times, LIFO shows higher COGS and lower net income – whereas COGS is lower under FIFO, so net income is higher.

Is LIFO or FIFO better for food?

Should restaurants use LIFO? The short answer is no. The higher cost of goods sold brought on by the LIFO model and will ultimately yield lower restaurant profit margins and net income. Also, unlike FIFO, the last-in, first-out method doesn't always provide an accurate valuation of closing inventory.

Why is LIFO more accurate?

LIFO inventory accounting increases record-keeping, because older inventory items may be kept on hand for several years, while under FIFO, those older items are sold first, so recordkeeping requirements are less.

Why is LIFO so popular?

The biggest benefit of LIFO is a tax advantage. During times of inflation, LIFO results in a higher cost of goods sold and a lower balance of remaining inventory. A higher cost of goods sold means lower net income, which results in a smaller tax liability.

Why do companies use LIFO?

The primary reason that companies choose to use an LIFO inventory method is that when you account for your inventory using the “last in, first out” method, you report lower profits than if you adopted a “first in, first out” method of inventory, known commonly as FIFO.

Is it better to sell stock FIFO or LIFO?

FIFO vs LIFO Stock Trades Under FIFO, if you sell shares of a company that you've bought on multiple occasions, you always sell your oldest shares first. FIFO stock trades results in the lower tax burden if you bought the older shares at a higher price than the newer shares.

Which inventory costing method is the best?

The most popular inventory accounting method is FIFO because it typically provides the most accurate view of costs and profitability.

What Is FIFO & What Is LIFO?

FIFO – According to FIFO, or First in, First out, the oldest inventory items are sold first. As a result, the oldest cost of an item in inventory is removed. Then this cost appears on the income statement as part of the cost of goods sold. For example, a clothes store purchased 200 pairs of jeans at a cost of $ 10 per pair. Then the store purchased one more batch at a cost of $ 11 per pair. As a result, the COGS of $10 per pair ($10 x 200 = $ 2,000) is recorded on the income statement because that was the cost of the first items in the inventory. The $11 pairs of jeans will be allocated to ending inventory, and this figure will appear on the balance sheet.

Why use LIFO method?

It helps them match the latest costs of products with the sales revenue of the current period, and thus reduce tax liability.

What is LIFO in accounting?

LIFO – According to LIFO, or Last in, First out, the most current prices are reported in ending inventory. If we return to our previous example, $11 will appear on the income statement as COGS ($11 x 200 = $ 2,200). As you can see, the LIFO method overvalues the inventory and thus reduces income tax liability.

Why is LIFO valuation not allowed?

Non-compliance with the IFRS (International Financial Reporting Standards) – The LIFO valuation method will not allow your business to operate internationally because it is banned by the IFRS due to reduced income tax figures.

What is accurate FIFO?

Accurate reports – With FIFO, your balance sheet will show the exact prices you paid to purchase the inventory.

Is it good to have fluctuating prices?

Not good in case of fluctuating prices – If your business places many orders for products that have fluctuating prices, it can become difficult to manage the inventory and respective prices of each new shipment.

Is FIFO compliant with LIFO?

Suitable for international sales – The FIFO method is compliant with International Financial Reporting Standards, because it does not reduce the tax figures like LIFO, so you can use it if your business operates internationally.

How to change from FiFO to LIFO?

If your business decides to change from FIFO to LIFO, you must file an application to use LIFO by sending Form 970 to the IRS. If you filed your business tax return for the year when you want to use LIFO, you can make the election by filing an amended tax return within 12 months of the date you filed the original return. 8

What is LIFO valuation?

LIFO is a newer inventory cost valuation technique (accepted in the 1930s), which assumes that the newest inventory is sold first. LIFO gives a higher cost to inventory.

What is FIFO in inventory?

First-In, First-Out (FIFO) Under FIFO, it's assumed that the inventory that is the oldest is being sold first. The FIFO method is the standard inventory method for most companies. FIFO gives a lower-cost inventory because of inflation; lower-cost items are usually older.

Which accounting organization allows FIFO and LIFO?

The U.S. accounting standards organization, the Financial Accounting Standards Board (FASB), in its Generally Accepted Accounting Procedures, allows both FIFO and LIFO accounting.

Does the IRS like LIFO?

As you might guess, the IRS doesn't like LIFO valuation, because it usually results in lower profits (less taxable income). But the IRS does allow businesses to use LIFO accounting, requiring an application, on Form 970 . If your business decides to change from FIFO to LIFO, you must file an application to use LIFO by sending Form 970 to the IRS. ...

Does IFRS allow LIFO inventory?

The international accounting standards organization IFRS doesn't allow LIFO inventory, so you will have to use FIFO if you are doing business internationally. 5

Is LIFO costing better than FIFO costing?

If your inventory costs are going up, or are likely to increase, LIFO costing may be better because the higher cost items (the ones purchased or made last) are considered to be sold. This results in higher costs and lower profits. If the opposite is true, and your inventory costs are going down, FIFO costing might be better.

Why is FIFO easier to understand?

As such, FIFO is just following that natural flow of inventory, meaning less chance of mistakes when it comes to bookkeeping.

Why are FIFO profits more accurate?

Although this may mean less tax for a company to pay under LIFO, it also means stated profits with FIFO are much more accurate because older inventory reflects the actual costs of that inventory. If profits are naturally high under FIFO, then the company becomes that much more attractive to investors.

What is LIFO reserve?

The LIFO reserve is the amount by which a company’s taxable income has been deferred, as compared to the FIFO method. The remaining unsold 350 televisions will be accounted for in “inventory”.

What is FIFO in accounting?

FIFO and LIFO are methods used in the cost of goods sold calculation. FIFO (“First-In, First-Out”) assumes that the oldest products in a company’s inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company’s inventory have been sold first ...

What is the problem with a company switching to the LIFO method?

The problem with a company switching to the LIFO method is that the older inventory may stay on the books forever, and that older inventory (if not perishable or obsolete) will not reflect current market values. It will be understated.

Is FIFO a LIFO?

FIFO and LIFO are assumptions only. The methods are not actually linked to the tracking of physical inventory, just inventory totals. This does mean a company using the FIFO method could be offloading more recently acquired inventory first, or vice-versa with LIFO. However, in order for the cost of goods sold (COGS) calculation to work, both methods have to assume inventory is being sold in their intended orders.

Is FIFO considered a best practice?

It is considered a best practice to go with FIFO.

Why do companies use FIFO or LIFO?

Most companies naturally prefer the FIFO inventory accounting method over LIFO because there is typically no valid reason to use recent inventory first, while leaving older inventory to age on the shelf. This is particularly true of perishable items, and items that rapidly become obsolete.

How to balance LIFO and FIFO?

Some businesses seek to balance LIFO and FIFO by using the average cost method of inventory cost accounting. Under ACM, the weighted average cost of all available inventory items for a given accounting period is used to calculate both COGS and ending inventory.

What is LIFO accounting?

Ultimately, the choice between FIFO and LIFO inventory accounting methods will be based on the needs of your business, and how it operates.

What industries use LIFO?

companies that use physical LIFO – Certain industries, like lumber and mining, stack the newest inventory items on top of older ones. businesses that face inventory write-downs during inflation – Examples include the fashion and agricultural industries that carry inventory that spoils, is easily damaged, or is vulnerable to obsolescence.

What is a LIFO?

LIFO and FIFO are the most common methods of inventory valuation for product-oriented businesses. Though each has its pros and cons, an understanding of how FIFO and LIFO work with your inventory accounting system will help you decide which method is best for your business.

Why do pharmacies use LIFO?

LIFO can appeal to companies looking to reduce their tax liability, and may be a better choice in certain scenarios, such as: businesses with steeply rising costs – Supermarkets and pharmacies typically use LIFO because their products are sensitive to inflation.

Why is LIFO important?

LIFO, on the other hand, is only strategically valuable during times of inflation, as goods sold first are also typically the most expensive. This increases the cost of goods sold, and reduces profits, which also reduces income tax liability.

Why use FIFO instead of LIFO?

In an inflationary economy, using LIFO leads to lower profit figures and helps in tax saving, while using FIFO leads to higher profit and a huge tax burden.

What is FIFO vs LIFO?

FIFO is a more realistic and logical approach of inventory valuation compared to LIFO. There is a risk of stocks, getting obsolete and outdated in case of LIFO, as goods are used from old stock, this risk can be reduced if FIFO is used. Unlike LIFO, record maintenance is easier in FIFO, as several layering is less.

Why use LIFO method?

So ultimately, the benefit of using the LIFO method for a company is that it can report a lower Net Income and hence defer its tax liabilities during the times of high inflation.

What is FIFO in accounting?

FIFO is the globally and widely used method for inventory valuation. While US GAAP allows adopting LIFO as well as FIFO, but in the international scenarios, FIFO is widely used, and IFRS restricts the use of LIFO for inventory valuation. Under LIFO, stock in hand represents the oldest stock, while in FIFO, stock in hand represents the latest stock.

Why do some companies use FIFO while some use LIFO for calculating the value of inventory?

Still, why do some companies use FIFO while some use LIFO for calculating the value of inventory? The answer to this is this: Companies use different methods of inventory accounting for the benefits and convenience offered by both methods in different situations.

What does FIFO mean in stock?

FIFO stands for ‘First In First Out, ‘ which implies that the inventory which was added first to the stock will be removed from stock first. So the inventory will leave the stock in order the same as that in which it was added to the stock.

How much is the cost of goods sold in LIFO?

3 plus any 50 units of Batch No. 2. Hence, the Cost of Goods Sold (COGS) will be equal to (100 * $ 20) + (50 * $ 15) = $ 2750.

What does LIFO stand for in inventory?

The LIFO definition stands for last in , first out. As such, it presumes that the most recent products in a company’s inventory gets sold first.

What is the FIFO Process?

It’s simple to use FIFO – the first in, first out method means just that. The oldest inventory items are always the first to go. So, old stock isn’t left hanging around. Whether you’re running an e-commerce site or a bricks and mortar company, the outcome is the same. It basically means that whatever is at the front of the queue goes first. Products leave the warehouse in the order in which they arrived.

What does "less profit" mean?

Less profit does mean less tax, though. Deflation may mean less profit. – If everything is based on the last item sold, then you will not be getting as much gross profit on this item. However, if you buy an item for cheap and manage to sell it on at a higher rate, then you will be making more profit.

Is inventory accounting FIFO or LIFO?

When it comes to inventory accounting, there is a difference in the result of FIFO and LIFO. The method of inventory management you choose will impact your financial results and tax payments. Here is what to take into consideration when looking at first in, first out accounting: It’s good for record-keeping.

When the gig is over, who is the first out?

Those that get in first go to the end of the venue, and those that are in last end up next to the door. So, when the gig is over, those that went in last are the first out.

Is FIFO accounting easy?

– The cycle of buying and selling stock makes the FIFO accounting method a much easier way to keep on top of things. As well as making it much simpler to calculate the COGS.

What is LIFO valuation?

Last in, first out (LIFO): LIFO inventory valuation is essentially the opposite of FIFO inventory costing. The LIFO method assumes the most recent items entered into your inventory will be the ones to sell first.

What is FIFO in accounting?

First in, first out (FIFO): The FIFO method of inventory valuation assumes the first items entered into your inventory are the first items you sell. FIFO inventory valuation assumes any inventory left on hand at the end of the accounting period should be valued at the most recent purchase price. Anything purchased at an older price would have been discarded due to spoilage or other loss of value.

What does FIFO mean in inventory?

FIFO stands for “first in, first out” and assumes the first items entered into your inventory are the first ones you sell. LIFO, also known as “last in, first out,” assumes the most recent items entered into your inventory will be the ones to sell first. The inventory valuation method you choose will depend on your tax situation, ...

Which method of inventory valuation is the least specific?

Retail method: Instead of valuing inventory based on the cost to acquire the inventory, the retail method values inventory based on the retail price of the inventory, reduced by the markup percentage. This is the least specific inventory valuation method.

Can you use LIFO for inventory?

You can choose to value all your inventory using LIFO, or you can use LIFO just for certain goods you carry. Once you elect to use LIFO for your inventory valuation, you cannot switch back to FIFO or another inventory valuation method without express permission from the IRS. To request a change in inventory valuation from the IRS, ...

Is LIFO more onerous than FIFO?

Recordkeeping: When comparing FIFO vs. LIFO, the recordkeeping requirements for LIFO are typically more onerous than those for FIFO. This is because the inventory in a business that uses LIFO is “layered,” meaning older inventory can be held for long periods of time.

Is $40 profit differential good?

A $40 profit differential wouldn’t make a significant difference to your bottom line. For the sake of simplicity, we kept the numbers in the example small. Also, we only looked at one item in your entire inventory. But you can easily see that — if the dollar amounts or the quantities sold were higher, and you factor in the different products in your craft store — choosing LIFO over FIFO would have a significant impact on your business’s profitability.

Why is LIFO lower than FIFO?

1. Because of inflation, where costs and expenses continue to rise, LIFO will have a lower profit margin than that of FIFO. This is because there is little to no inflation gap to allow LIFO businesses to capitalize on their inventory.

Which is more complicated, LIFO or FIFO?

LIFO has much more complicated cost layers than FIFO does. Cost layers are a way to keep track of the inventory, purchasing expenses and profits. Here’s an example to further demonstrate cost layers.

What is FIFO valuation?

In the end, FIFO is the most widely recognized and accepted valuation method for inventory management. It’s safer, easier and is more advantageous in the long run that dealing with the confusion and potential profit loss of LIFO. Learn more about inventory management techniques to help you make a sound decision for your business. You can also brush up on your accounting skills in our finance and accounting for start-ups course.

What is FIFO in inventory management?

FIFO. The first in first out method of inventory management explains the order in which inventory is purchased and then sold. When a business utilizes the FIFO method, they sell the products that they received first before selling the products they received last.

What are the disadvantages of LIFO?

2. The second disadvantage would be clerical errors. When inventory prices are always in flux it can become cumbersome to correctly record cost of goods, selling price of goods and any discrepancy that may occur because of rising or falling market prices. With last in first out, the last batch of goods purchased is the first batch of goods being sold so the likelihood of a price change is low. However, LIFO has many cost layers and can become quite confusing to record correctly. There is more to this but see LIFO disadvantages below.

Why is LIFO so hard to find investors?

2. Because of LIFO’s generally lower reported profits, businesses utilizing this valuation of inventory can have a harder time finding investors. Individuals and businesses looking to invest their money are usually looking for companies that show substantial profit growth over a period of time.

Why do accountants use FIFO?

Accountants have to write off what’s called obsolete inventory after a certain amount of time goes by and the product is not used or sold. Because FIFO makes sure that the oldest items in stock are used or sold before they are deemed obsolete companies can save money.