To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold. The FIFO (“First-In, First-Out”) method means that the cost of a company’s oldest inventory is used in the COGS (Cost of Goods Sold) calculation.

What is the difference between FIFO vs. LIFO?

- First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method.

- Last-in, first-out (LIFO) assumes the last inventory added will be the first sold.

- Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

How to determine which shares to sell, FIFO or LIFO?

How to Determine Which Shares to Sell, FIFO or LIFO

- FIFO vs LIFO Stock Trades. The first-in, first-out method is the default way to decide which shares to sell. ...

- Tell Your Broker. If you plan to use any method besides FIFO, including LIFO, you must specifically direct your broker as to which shares to sell so that your taxes ...

- 2018 Tax Law Changes. ...

- 2017 Tax Law. ...

How would FIFO and LIFO affect the income taxes paid?

The main difference between LIFO and FIFO is based on the assertion that the most recent inventory purchased is usually the most expensive. If that assertion is accurate, using LIFO will result in a higher cost of goods sold and less profit, which also directly affects the amount of taxes you’ll have to pay. What is LIFO?

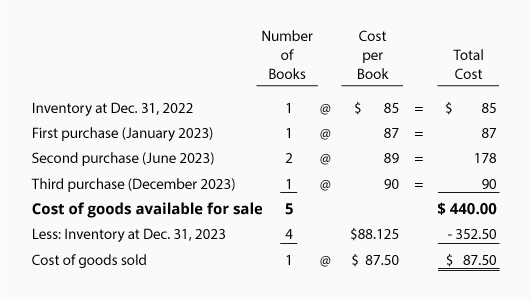

What is FIFO and LIFO example?

Ending Inventory per LIFO: 1,000 units x $8 = $8,000. Remember that the last units in (the newest ones) are sold first; therefore, we leave the oldest units for ending inventory. Ending Inventory per FIFO: 1,000 units x $15 each = $15,000.

Can you use FIFO and LIFO at the same time?

The Internal Revenue Service allows you to use the first-in, first-out method or the last-in, first-out method -- FIFO and LIFO. If you choose LIFO, you can further select from one of several submethods, including dollar-value LIFO, or DVL.

Why FIFO and LIFO methods are used?

FIFO (first in, first out) inventory management seeks to sell older products first so that the business is less likely to lose money when the products expire or become obsolete. LIFO (last in, first out) inventory management applies to nonperishable goods and uses current prices to calculate the cost of goods sold.

How do you calculate ending inventory using FIFO?

According to the FIFO method, the first units are sold first, and the calculation uses the newest units. So, the ending inventory would be 1,500 x 10 = 15,000, since $10 was the cost of the newest units purchased. The ending inventory for Harod's company would be $15,000.

Which inventory method is best?

The most popular inventory accounting method is FIFO because it typically provides the most accurate view of costs and profitability.

Should I sell older or newer stocks?

As a general rule if you have a profit from the sale of a stock you would want to sell those stocks that you have held for over 1 year first, (long term gain). The tax on long term gains are typically less than short term gains.

How do you use FIFO?

To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

Where is LIFO used?

Last in, first out (LIFO) is a method used to account for inventory. Under LIFO, the costs of the most recent products purchased (or produced) are the first to be expensed. LIFO is used only in the United States and governed by the generally accepted accounting principles (GAAP).

What is FIFO example?

Example of FIFO Imagine if a company purchased 100 items for $10 each, then later purchased 100 more items for $15 each. Then, the company sold 60 items. Under the FIFO method, the cost of goods sold for each of the 60 items is $10/unit because the first goods purchased are the first goods sold.

How do you calculate cost of goods sold using LIFO?

2:458:12LIFO Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipFrom which dates with which prices are going to go on the cost of goods sold and which are going toMoreFrom which dates with which prices are going to go on the cost of goods sold and which are going to be in our ending inventory and we're making an assumption and in this case we're going to assume.

What is LIFO example?

Example of LIFO that buys coffee mugs from wholesalers and sells them on the internet. One Cup's cost of goods sold (COGS) differs when it uses LIFO versus when it uses FIFO. In the first scenario, the price of wholesale mugs is rising from 2016 to 2019.

How do you calculate cost of goods sold using the FIFO periodic inventory method?

1:554:57FIFO Periodic Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipSo then the next 20 units are gonna come out of this 30 from January 6 purchase. So that's 20 unitsMoreSo then the next 20 units are gonna come out of this 30 from January 6 purchase. So that's 20 units at $40 a unit. So we add those together and that gives us $1,500. As our cost of goods sold.

What is LIFO method?

LIFO. When sales are recorded using the LIFO method, the most recent items of inventory are used to value COGS and are sold first. In other words, the older inventory, which was cheaper, would be sold later.

Why is LIFO not accurate?

As a result, LIFO doesn't provide an accurate or up-to-date value of inventory because the valuation is much lower than inventory items at today's prices.

What is FIFO in accounting?

The First-In, First-Out (FIFO) method assumes that the first unit making its way into inventory–or the oldest inventory–is the sold first. For example, let's say that a bakery produces 200 loaves of bread on Monday at a cost of $1 each, and 200 more on Tuesday at $1.25 each. FIFO states that if the bakery sold 200 loaves on Wednesday, the COGS ( on the income statement) is $1 per loaf because that was the cost of each of the first loaves in inventory. The $1.25 loaves would be allocated to ending inventory ( on the balance sheet ).

Why would COGS be higher under LIFO?

In an inflationary environment, the current COGS would be higher under LIFO because the new inventory would be more expensive. As a result, the company would record lower profits or net income for the period. However, the reduced profit or earnings means the company would benefit from a lower tax liability.

Why is FIFO better than COGS?

FIFO can be a better indicator of the value for ending inventory because the older items have been used up while the most recently acquired items reflect current market prices. For most companies, FIFO is the most logical choice since they typically use their oldest inventory first in the production of their goods, which means the valuation of COGS reflects their production schedule.

What is the first in first out method?

The First-In, First-Out (FIFO) method assumes that the oldest unit of inventory is the sold first. LIFO is not realistic for many companies because they would not leave their older inventory sitting idle in stock. FIFO is the most logical choice since companies typically use their oldest inventory first in the production of their goods.

When sales are recorded using the FIFO method, what is the oldest inventory?

When sales are recorded using the FIFO method, the oldest inventory–that was acquired first–is used up first. FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet.

What is FIFO in accounting?

FIFO and LIFO are methods used in the cost of goods sold calculation. FIFO (“First-In, First-Out”) assumes that the oldest products in a company’s inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company’s inventory have been sold first ...

What is LIFO reserve?

The LIFO reserve is the amount by which a company’s taxable income has been deferred, as compared to the FIFO method. The remaining unsold 350 televisions will be accounted for in “inventory”.

Why are FIFO profits more accurate?

Although this may mean less tax for a company to pay under LIFO, it also means stated profits with FIFO are much more accurate because older inventory reflects the actual costs of that inventory. If profits are naturally high under FIFO, then the company becomes that much more attractive to investors.

Is LIFO more attractive than FIFO?

You can see how for Ted, the LIFO method may be more attractive than FIFO. This is because the LIFO number reflects a higher inventory cost, meaning less profit and less taxes to pay at tax time. The LIFO reserve in this example is $31,250.

Is LIFO legal in the US?

Under GAAP, LIFO is legal. Outside the United States, LIFO is not permitted as an accounting practice. This is why you’ll see some American companies use the LIFO method on their financial statements, and switch to FIFO for their international operations.

Why use FIFO vs LIFO?

FIFO vs. LIFO for flow of goods. Many companies choose to use FIFO because it more closely mimics the actual flow of goods in and out of inventory. It's considered a simpler system with less spoilage and waste of materials.

Why is FIFO higher than LIFO?

Because the cost of goods sold is usually higher under LIFO, this decreases a company's reported profits, which can lower the amount of tax liability. Conversely, FIFO valuations present a higher tax liability because the cost of goods sold is lower. Read more: FIFO Accounting: What It Is and What You Need To Know.

What is a fifo and a fifo?

While both FIFO and LIFO are a way to manage inventory, the marketable goods produced by a company usually dictate which method to choose. FIFO is typically used for perishable products like food and beverages or stock that may become obsolete if it isn't sold within a certain period of time. LIFO however is often used for products that aren't affected by the amount of time spent in inventory or where the flow of product fits the LIFO method.

How is FIFO inventory calculated?

FIFO inventory cost is calculated by determining the cost of the oldest stock and multiplying that amount by the number of items sold.

What is FIFO in inventory?

What is FIFO? First in, first out is a method to value inventory and calculate the cost of goods sold. FIFO items are the oldest products in an inventory because they were the first stock to be added after purchase or production. FIFO uses the principle that when items are acquired first, they are also sold first.

What is LIFO method?

Using the LIFO method, more recent stock can be valued higher than older goods when there is a price increase. LIFO works well using the matching principle, which is used to charge costs along with revenues during the same period of inventory calculations. Read more: A Guide To the Inflation Rate.

What is the last in first out approach?

Last in, first out is another way to manage inventory and calculate profits from goods. In this approach, businesses figure that the most recent inventory is the first sold. This means that older stock continues to sit for longer periods before being sold.

What is the LIFO method?

Recordkeeping. If you choose to use the LIFO method of inventory valuation, you will need a recordkeeping system that allows you to determine when you access older “layers” of inventory and then apply the cost of that older inventory accurately.

What does FIFO mean in inventory?

FIFO stands for “first in, first out” and assumes the first items entered into your inventory are the first ones you sell. LIFO, also known as “last in, first out,” assumes the most recent items entered into your inventory will be the ones to sell first. The inventory valuation method you choose will depend on your tax situation, ...

What is inventory flow?

Inventory flow: Most businesses sell the oldest items in stock first. Think of a grocery store or a clothing boutique: In both of these types of businesses, stock loses its value with time, and so the older items are pushed to the front of the shelves to help them sell quicker.

Can you use LIFO or FIFO valuation?

Inventory flow. For spools of craft wire, you can reasonably use either LIFO or FIFO valuation. For perishable goods — like groceries — or other items that lose their value with time, using LIFO valuation doesn’t make sense because you will always try to sell older inventory first.

Can you use LIFO for inventory?

You can choose to value all your inventory using LIFO, or you can use LIFO just for certain goods you carry. Once you elect to use LIFO for your inventory valuation, you cannot switch back to FIFO or another inventory valuation method without express permission from the IRS. To request a change in inventory valuation from the IRS, ...

Is LIFO more onerous than FIFO?

Recordkeeping: When comparing FIFO vs. LIFO, the recordkeeping requirements for LIFO are typically more onerous than those for FIFO. This is because the inventory in a business that uses LIFO is “layered,” meaning older inventory can be held for long periods of time.

Is LIFO valuation allowed?

Reporting requirements. If you are looking to do business internationally, you must keep IFRS requirements in mind. LIFO valuation is not allowed under these standards. If you plan to do business outside of the U.S., choose FIFO or another inventory valuation method instead. Back to top.

What is LIFO method?

The LIFO method is one that you have to elect affirmatively with your broker. The main benefit of the LIFO method is that the shares that you've owned for the shortest period of time tend to be the ones that have the smallest taxable gain, and so you can make a sale without incurring a large tax bill. However, because the LIFO method involves the ...

What does FIFO mean in stock?

FIFO and LIFO are acronyms that, in this case, relate to the stock you decide to sell. FIFO stands for first in, first out, while LIFO stands for last in, first out. What this means is that if you use the FIFO method, then a sale of stock will be allocated to the shares you bought earliest.

What is FIFO in tax?

The FIFO method is the default for the IRS, and so if you don't specify a method with your broker when you sell shares, you'll automatically be treated as if you had elected FIFO treatment. The main benefit of the FIFO method is that by using the shares you acquired first, you're more likely to get long-term capital gains treatment ...

What is the disadvantage of FIFO method?

The disadvantage of the FIFO method, however, is that because stock prices tend to rise over time, the shares you bought first will typically have the lowest cost basis. That means that your taxable gain could be higher than it would be on other shares you've owned for a shorter period of time.

Why use LIFO over FIFO?

The advantages of LIFO are also its disadvantages as the only real purpose of instituting LIFO is to avoid paying higher taxes but this means profits are generally lower.

What happens when a company uses FIFO?

When companies use FIFO they will constantly have an updated reflection of the current market prices for the items in their inventory. This happens as older products are taken from the inventory stock to be sold, the newer inventory is left on the books for the end of the month.

What is FIFO in inventory management?

FIFO. The first in first out method of inventory management explains the order in which inventory is purchased and then sold. When a business utilizes the FIFO method, they sell the products that they received first before selling the products they received last.

Why is LIFO so hard to find investors?

2. Because of LIFO’s generally lower reported profits, businesses utilizing this valuation of inventory can have a harder time finding investors. Individuals and businesses looking to invest their money are usually looking for companies that show substantial profit growth over a period of time.

What are the advantages and disadvantages of LIFO?

Like mentioned above, LIFO most often means lower profits for the company, but when you report lower profits, you don’t have to pay as many income taxes. This allows the business to have more cash-in-hand to use for investment opportunities or to purchase more inventory. Disadvantages.

Why do accountants have to write off obsolete inventory?

Because FIFO makes sure that the oldest items in stock are used or sold before they are deemed obsolete companies can save money. 2.

What is the difference between FIFO and LIFO?

FIFO (first in, first out) inventory management seeks to sell older products first so that the business is less likely to lose money when the products expire or become obsolete. LIFO (last in , first out) inventory management applies to nonperishable goods and uses current prices to calculate the cost of goods sold.

How are FIFO and LIFO similar?

However, they are similar in one regard: Both depend on the product remaining the same, with price being the only fluctuating element. FIFO and LIFO influence a company's earnings on paper.

Why is FIFO a good valuation method?

For businesses that need to impress investors, this becomes an ideal method of valuation, until the higher tax liability is considered. Because FIFO results in a lower recorded cost per unit, it also records a higher level of pretax earnings. And with higher profits, companies will likewise face higher taxes.

What is LIFO in accounting?

The principle of LIFO is highly dependent on how the price of goods fluctuates based on the economy . If a company holds inventory for a long time, holding on to products may prove quite advantageous in hedging profits for taxes. LIFO allows for higher after-tax earnings due to the higher cost of goods.

How does LIFO work?

As an example of how LIFO works, suppose a website development company purchases a plugin for $30 and then sells the finished product for $50. However, several months later, that asset has increased in price to $35. When the company calculates its profits, it would use the most recent price of $35. In tax statements, it would then appear as if the company made a profit of only $15. By using LIFO, a company would appear to be making less money than it actually did and, therefore, have to report less in taxes.

Is LIFO a FIFO?

This increases the comparability of LIFO and FIFO firms. In general, both U.S. and international standards are moving away from LIFO. Many U.S.-based companies have switched to FIFO, and some companies still use LIFO within the United States as a form of inventory management but translate it to FIFO for tax reporting.

Does LIFO have to be converted to FIFO?

Because of the current discrepancy, however, U.S.-based companies that use LIFO must convert their statements to FIFO in the footnotes of their financial statements. This difference is known as the LIFO reserve and is calculated between the cost of goods sold under LIFO and FIFO, Melwani said.

What is FIFO accounting?

The first in, first out (FIFO) accounting method relies on a cost flow assumption that removes costs from the inventory account when an item in someone’s inventory has been purchased at varying costs, over time. When a business uses FIFO, the oldest cost of an item in an inventory will be removed first when one of those items is sold. This oldest cost will then be reported on the income statement as part of the cost of goods sold.

What is the last in first out accounting method?

With this accounting technique, the costs of the oldest products will be reported as inventory. It should be understood that, although LIFO matches the most recent costs with sales on the income statement, the flow of costs does not necessarily have to match the flow of the physical units.

Does LIFO match the flow of costs?

It should be understood that, although LIFO matches the most recent costs with sales on the income statement, the flow of costs does not necessarily have to match the flow of the physical units. Generally speaking, FIFO is preferable in times of rising prices, so that the costs recorded are low, and income is higher.