What kind of businesses use FIFO?

The advantages to the FIFO method are as follows:

- The method is easy to understand, universally accepted and trusted.

- FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first). ...

- Less waste (a company truly following the FIFO method will always be moving out the oldest inventory first).

What are the advantages and disadvantages of FIFO?

Advantages: (i) Since materials issued for production are at the original cost, the inventory reflects the current market price, (ii) Profit and Loss Account and the Balance Sheet satisfactorily represent the actual conditions, (iii) When the price level is declining, the FIFO method shows a lower profit for income tax implications, (iv) Next ...

What are the rules of FIFO?

Theory and Practice on FiFo Lanes – How Does FiFo Work in Lean Manufacturing?

- The Reason for FiFo – Decoupling of Processes. Processes usually have different cycle times needed to process one part. ...

- The Rules for FiFo. The first part that goes into the buffer is also the first part that comes out, hence the name FiFo for First-In-First-Out.

- Advantages of FiFo Lanes. A FiFo lane has quite some advantages. ...

- Examples of FiFo Lanes. ...

How do you calculate gross profit using FIFO?

What are the benefits of good stock rotation?

- Increases productivity and efficiency.

- Creates a more organised warehouse.

- Helps save time and money.

- Improves accuracy of inventory orders.

- Keeps customers coming back for more.

What is FIFO method with example?

Example of FIFO Imagine if a company purchased 100 items for $10 each, then later purchased 100 more items for $15 each. Then, the company sold 60 items. Under the FIFO method, the cost of goods sold for each of the 60 items is $10/unit because the first goods purchased are the first goods sold.

How do you calculate FIFO sales?

4:436:32How to Calculate FIFO Inventory (The Easy Way) - YouTubeYouTubeStart of suggested clipEnd of suggested clipSo it's FIFO right first-in first-out so we take our oldest units first and assigned to cost ofMoreSo it's FIFO right first-in first-out so we take our oldest units first and assigned to cost of goods sold. So that means we're gonna take all of this 25 up here so all of the 450. Right. Now we're

How do you perform FIFO?

The FIFO procedure follows 5 simple steps:Locate products with the soonest best before or use-by dates.Remove items that are past these dates or are damaged.Place items with the soonest dates at the front.Stock new items behind the front stock; those with the latest dates should be at the back.More items...•

What is the FIFO costing method?

What is FIFO costing? In simplest terms, FIFO (first-in, first-out) costing allows you to track the cost of an item/SKU based on its cost at purchase order receipt, and apply this cost against each shipment of the item until the receipt quantity is exhausted.

How do you calculate FIFO periodic ending inventory?

According to the FIFO method, the first units are sold first, and the calculation uses the newest units. So, the ending inventory would be 1,500 x 10 = 15,000, since $10 was the cost of the newest units purchased. The ending inventory for Harod's company would be $15,000.

What is LIFO and FIFO with example?

First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method. Last-in, first-out (LIFO) assumes the last inventory added will be the first sold. Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

Is FIFO left to right?

The cone system works as follows: carts are positioned from left to right and the cone shows the ´oldest´ cart, which means it is the first cart to be taken out of the FIFO by the downstream station. When the oldest cart is taken out, the employee moves the cone one position to the right, the new ´oldest´ cart.

Why FIFO method is used?

FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first). This makes bookkeeping easier with less chance of mistakes. Less waste (a company truly following the FIFO method will always be moving out the oldest inventory first).

How do you calculate gross profit using FIFO?

For example, suppose a company's oldest inventory cost $200, the newest cost $400, and it has sold one unit for $1,000. Gross profit would be calculated as $800 under LIFO and $600 under FIFO.

What is the benefit of using FIFO?

1. Better valuation of inventory . By using FIFO, the balance sheet shows a better approximation of the market value of inventory. The latest costs for manufacturing or acquiring the inventory are reflected in inventory, and therefore, the balance sheet reflects the approximate current market value.

What is FIFO expense?

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

Can you use LIFO in Canada?

Therefore, we can see that the balances for COGS and inventory depend on the inventory valuation method. For income tax purposes in Canada, companies are not permitted to use LIFO. However, US companies are able to use FIFO or LIFO.

Why use LIFO method?

For some companies, there are benefits to using the LIFO method for inventory costing. For example, those companies that sell goods that frequently increase in price might use LIFO to achieve a reduction in taxes owed.

What is the first in first out method?

Companies frequently use the first in, first out (FIFO) method to determine the cost of goods sold or COGS. The FIFO method assumes the first products a company acquires are also the first products it sells. The company will report the oldest costs on its income statement, whereas its current inventory will reflect the most recent costs. FIFO is a good method for calculating COGS in a business with fluctuating inventory costs.

Is FIFO a good method for calculating COGS?

FIFO is a good method for calculating COGS in a business with fluctuating inventory costs. While the LIFO inventory valuation method is accepted in the United States, it is considered controversial and prohibited by the International Financial Reporting Standards (IFRS).

Is FIFO cash flow assumption accurate?

While an actual sales pattern may not follow the FIFO cash flow assumption exactly, it is still an accurate method for determining COGS and allowed by both generally accepted accounting principles (GAAP) and International Financial Reporting Standards (IFRS).

Why Would You Use FIFO over LIFO?

Both are legal although the LIFO method is often frowned upon because bookkeeping is far more complex and the method is easy to manipulate.

What Are the Advantages of FIFO?

The FIFO method is considered to me a more trusted method than the LIFO (“Last-In, First-Out”) method. You can read more about why FIFO is preferable here.

What method does Sal use to calculate his cost of goods sold?

January has come along and Sal needs to calculate his cost of goods sold for the previous year, which he will do using the FIFO method.

Why is the LIFO method understated?

The value of remaining inventory, assuming it is not-perishable, is also understated with the LIFO method because the business is going by the older costs to acquire or manufacture that product. That older inventory may, in fact, stay on the books forever. Investors and banking institutions value FIFO because it is a transparent method ...

What does FIFO mean in accounting?

FIFO stands for “First-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company’s inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation.

Why do investors value FIFO?

Investors and banking institutions value FIFO because it is a transparent method of calculating cost of goods sold. It is also easier for management when it comes to bookkeeping, because of its simplicity.

Which countries use FIFO?

Outside the United States, many countries, such as Canada, India and Russia are required to follow the rules set down by the IFRS (International Financial Reporting Standards) Foundation. The IFRS provides a framework for globally accepted accounting standards, among them is the requirements that all companies calculate cost of goods sold using the FIFO method. As such, many businesses, including those in the United States, make it a policy to go with FIFO.

Why is FIFO accounting used?

FIFO method of accounting saves time, and money spends in calculating the exact inventory cost that is being sold because the recording of inventory is done in the same order as they are purchased or produced. Easy to understand.

What is FIFO valuation?

Under the FIFO method of accounting inventory valuation, the goods which are purchased at the earliest are the first one to be removed from the inventory account. This results in remaining inventory at books to be valued at the most recent price for which the last stock of inventory is purchased. This results in inventory assets recorded on the balance sheet at the most recent costs.

What are the disadvantages of FIFO accounting?

One of the biggest disadvantages of FIFO accounting method is inventory valuation during inflation, First In First Out method will result in higher profits, and thus will results in higher “Tax Liabilities” in that particular period. This may result in increased tax charges and higher tax-related cash outflows.

What is the ending inventory formula?

Ending Inventory The ending inventory formula computes the total value of finished products remaining in stock at the end of an accounting period for sale. It is evaluated by deducting the cost of goods sold from the total of beginning inventory and purchases. read more

Which method of inventory valuation gives the most accurate calculation of the inventory and sales profit?

A business which is in the trading of perishable items generally sells the items which are purchased earliest first, FIFO method of inventory valuation generally gives the most accurate calculation of the inventory and sales profit. Other examples include retail businesses that sell foods or other products with an expiration date.

Is FIFO valuation a good measure?

FIFO method of inventory valuation is not an appropriate measure if the goods/materials purchased have fluctuation in their price patterns as this may results in misstated profits for the same period.

Is the first in first out method a good measure of inventory?

Use of First In First Out method is not a suitable measure of inventory in times of “ hyperinflation .”. During such times, there is no particular pattern of inflation, which may result in prices of goods to inflate drastically.

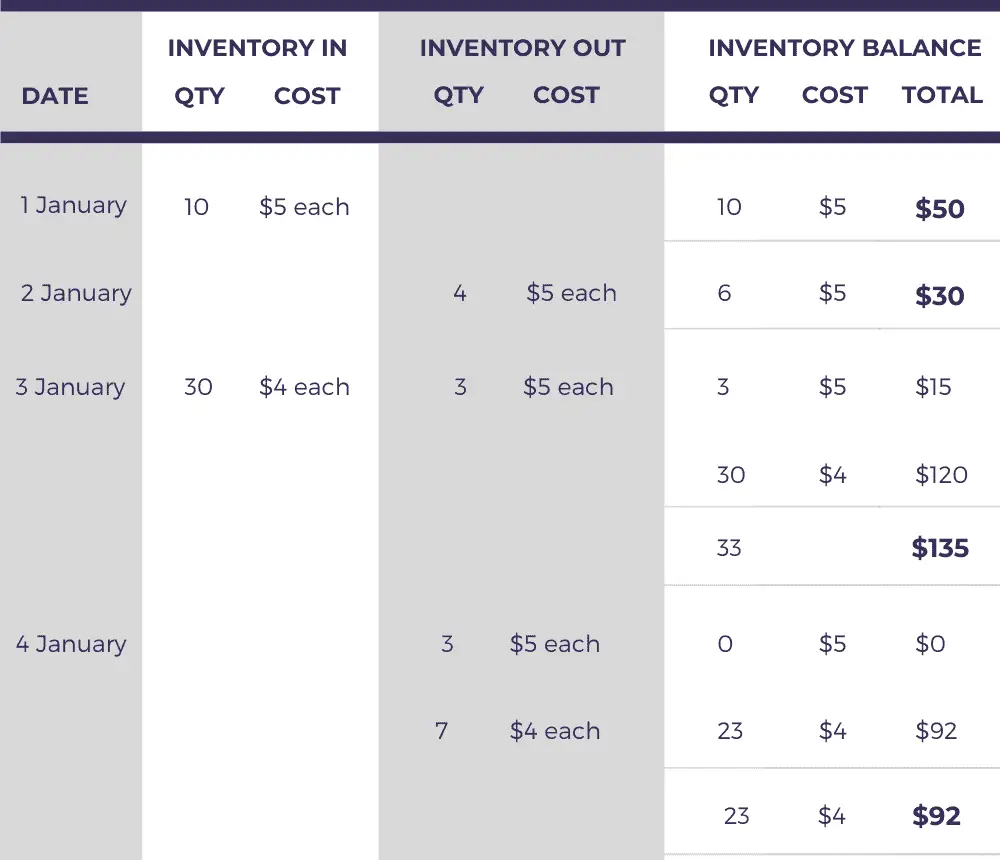

Methods of calculating inventory cost

As inventory is usually purchased at different rates (or manufactured at different costs) over an accounting period, there is a need to determine what cost needs to be assigned to inventory.

First In First Out (FIFO)

This method assumes that inventory purchased first is sold first. Therefore, inventory cost under FIFO method will be the cost of latest purchases. Consider the following example:

Example

Bike LTD purchased 10 bikes during January and sold 6 bikes, details of which are as follows:

What is FIFO method?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

What is FIFO accounting?

First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last. An alternative to FIFO, LIFO is an accounting method in which assets purchased or acquired last are disposed of first.

What Are the Advantages of First In, First Out (FIFO)?

The obvious advantage of FIFO is that it's the most widely used method of valuing inventory globally. It is also the most accurate method of aligning the expected cost flow with the actual flow of goods which offers businesses a truer picture of inventory costs . Furthermore, it reduces the impact of inflation, a ssuming that the cost of purchas ing newer inventory will be higher than the purchasing cost of older invent ory. Finally, it reduces the obsolescence of inventory.

What happens when FIFO assigns the oldest costs to the cost of goods sold?

In this situation, if FIFO assigns the oldest costs to the cost of goods sold, these oldest costs will theoretically be priced lower than the most recent inventory purchased at current inflated prices. This lower expense results in higher net income. Also, because the newest inventory was purchased at generally higher prices, the ending inventory balance is inflated.

What is FIFO in manufacturing?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense. Under FIFO, it is assumed that the cost of inventory purchased first will be recognized first. The dollar value of total inventory decreases in this process because inventory has been removed from the company’s ownership. The costs associated with the inventory may be calculated in several ways — one being the FIFO method.

What Are the Other Inventory Valuation Methods?

In inflationary economies, this results in deflated net income costs and lower ending balances in inventory when compared to FIFO. Average cost inventory is another method that assigns the same cost to each item and results in net income and ending inventory balances between FIFO and LIFO. Finally, specific inventory tracing is used only when all components attributable to a finished product are known.

What is FIFO method?

The use of FIFO method is very common to compute cost of goods sold and the ending balance of inventory under both perpetual and periodic inventory systems. The example given below explains the use of FIFO method in a perpetual inventory system. If you want to understand its use in a periodic inventory system, read “ first-in, ...

What is FIFO in inventory?

The first-in, first-out (FIFO) method is a widely used inventory valuation method that assumes that the goods are sold (by merchandising companies) or materials are issued to production department (by manufacturing companies) in the order in which they are purchased. In other words, the costs to acquire merchandise or materials are charged ...

What is FIFO in fine electronics?

The Fine Electronics company uses perpetual inventory system to account for acquisition and sale of inventory and first-in, first-out (FIFO) method to compute cost of goods sold and for the valuation of ending inventory. The company has made the following purchases and sales during the month of January 2016.

How much did Fine Electronics sell for in 2016?

January 4:#N#The Fine electronics company has sold 16 units for $25,600 (16 units × $1,600) on January 4, 2016. On this date, 24 units in the beginning inventory are the only units available for sale. The cost of goods sold is, therefore, $16,000 (16 × $1,000). Since the company uses perpetual inventory system, two journal entries would be made for the sale of inventory – one to reduce the inventory account by the cost of 16 units and one to record the sale of 16 units. These two journal entries are given below:

Can you compute the cost of goods sold and ending inventory?

With the help of the above inventory card, we can easily compute the cost of goods sold and ending inventory.