The most common of these methods are the FIFO, LIFO and Average Cost Method. It is calculated by dividing the total number of units you have on hand by the total cost of goods. You will arrive at an average unit cost for each unit of your inventory.

What is the difference between FIFO and average method?

Difference between FIFO and average costing method: 1. Primary distinction: The primary difference between the two methods is the cost ascertained to the inventory that is dispatched or sold by a business. In FIFO method, the basic assumption followed is that inventory which is acquired first or enters the business first will be the first to exit.

What is the difference between FIFO vs. LIFO?

- First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method.

- Last-in, first-out (LIFO) assumes the last inventory added will be the first sold.

- Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

How to calculate cost of goods sold using FIFO method?

Inputs:

- First of all, you just have to enter the quantity of each unit purchases

- Then, you have to add the quantity of the price/unit you purchased

- Also, the lifo fifo method calculator provides you with options of adding more purchases “one by one” or multiple

- Then, you have to enter the total units sold from your number of purchases

How do you find average cost in FIFO?

Average Cost Method of accounting for inventory takes an average, as the name implies, of all of the costs of all of your inventory. It is calculated by dividing the total number of units you have on hand by the total cost of goods. You will arrive at an average unit cost for each unit of your inventory.

How do you calculate the average cost method?

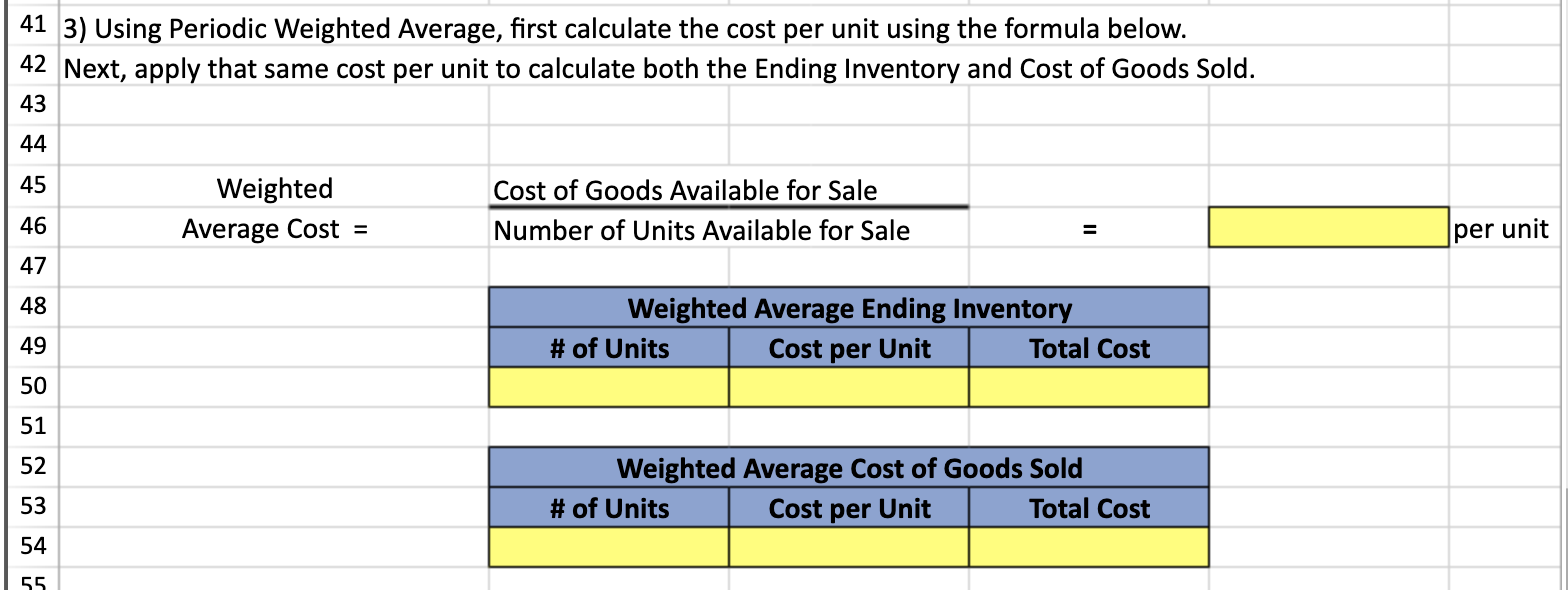

To calculate average cost, take the cost of goods available for sale and divide it by the total number of items from the beginning inventory and purchases. This means that the cost of all 15 pairs is treated as if they were $11 each. Therefore, $11 is the average cost for this item.

How do you find FIFO from LIFO?

Convert LIFO to FIFO statementAdd the LIFO reserve to LIFO inventory.Deduct the excess cash saved from lower taxes under LIFO (i.e. LIFO Reserve x Tax rate)Increase the retained earnings component of shareholders' equity by the LIFO reserve x (1-T)In the income statement, FIFO COGS = LIFO COGS – Δ LIFO Reserve.

How do you calculate cost of goods using LIFO?

How to use LIFO for costs of goods sold calculationq 1 q_1 q1 = Number of units purchased 1st time.p 1 p_1 p1 = 1st units purchased price.q 2 q_2 q2 = Number of units purchased 2nd time.p 2 p_2 p2 = 2nd units purchased price. ... q i q_i qi = Number of units purchased last time.p i p_i pi = Last units purchased price.

What is the example of average cost?

Assume the company sold 72 units in the first quarter. The weighted-average cost is the total inventory purchased in the quarter, $113,300, divided by the total inventory count from the quarter, 100, for an average of $1,133 per unit.

What is the difference between FIFO and average cost?

The difference between the two depends on the way the inventory is issued; one method sells the goods purchased first (FIFO) and the other calculates the average price for the total inventory (weighted average).

How do you calculate the average cost of goods sold?

The average cost is computed by dividing the total cost of goods available for sale by the total units available for sale. This gives a weighted-average unit cost that is applied to the units in the ending inventory.

How do you calculate average inventory?

Average inventory is a calculation of inventory items averaged over two or more accounting periods. To calculate the average inventory over a year, add the inventory counts at the end of each month and then divide that by the number of months.

What is LIFO FIFO with example?

FIFO (“First-In, First-Out”) assumes that the oldest products in a company's inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company's inventory have been sold first and uses those costs instead.

How do you calculate cost of goods sold using FIFO perpetual?

4:346:22FIFO (Perpetual Inventory) - YouTubeYouTubeStart of suggested clipEnd of suggested clipWe need to sell an additional 10 on top of that 15. So that 10 comes from our inventory group at $8MoreWe need to sell an additional 10 on top of that 15. So that 10 comes from our inventory group at $8 apiece so under cost of goods sold. We have 15 units at $6. And then 10 units at $8.

How do you calculate cost of goods sold using the FIFO periodic inventory method?

1:554:57FIFO Periodic Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipSo then the next 20 units are gonna come out of this 30 from January 6 purchase. So that's 20 unitsMoreSo then the next 20 units are gonna come out of this 30 from January 6 purchase. So that's 20 units at $40 a unit. So we add those together and that gives us $1,500. As our cost of goods sold.

B1. Perpetual FIFO

Under the perpetual system the Inventory account is constantly (or perpetually) changing. When a retailer purchases merchandise, the retailer debit...

B2. Perpetual LIFO

Under the perpetual system the Inventory account is constantly (or perpetually) changing. When a retailer purchases merchandise, the retailer debit...

B3. Perpetual Average

Under the perpetual system the Inventory account is constantly (or perpetually) changing. When a retailer purchases merchandise, the costs are debi...

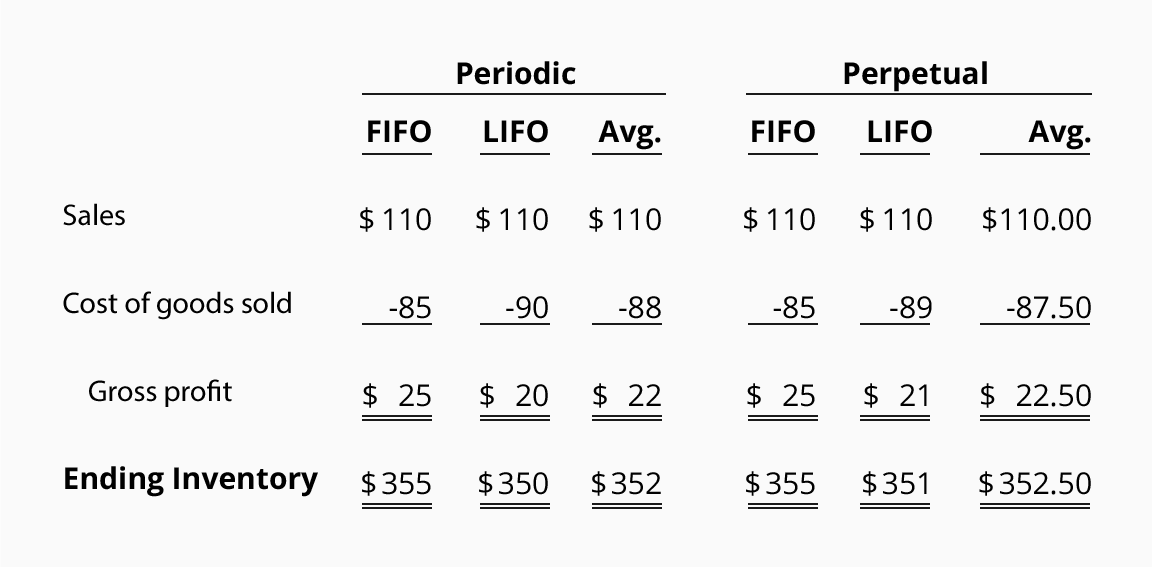

Comparison of Cost Flow Assumptions

Below is a recap of the varying amounts for the cost of goods sold, gross profit, and ending inventory that were calculated above.The example assum...

What is the difference between FIFO and LIFO?

The FIFO (“First-In, First-Out”) method means that the cost of a company’s oldest inventory is used in the COGS (Cost of Goods Sold) calculation. LIFO (“Last-In, First-Out”) means that the cost of a company’s most recent inventory is used instead. Here’s What We’ll Cover:

Why use LIFO or FIFO?

The LIFO method for financial accounting may be used over FIFO when the cost of inventory is increasing, perhaps due to inflation. Using FIFO means the cost of a sale will be higher because the more expensive items in inventory are being sold off first.

What does FIFO mean in accounting?

FIFO is an acronym. It stands for “First-In, First-Out” and is used for cost flow assumption purposes. Cost flow assumptions refers to the method of moving the cost of a company’s product out of its inventory to its cost of goods sold. Inventory refers to:

When calculating COGS, what is the company going to go by?

Therefore, when calculating COGS (Cost of Goods Sold), the company will go by those specific inventory costs. Although the oldest inventory may not always be the first sold, the FIFO method is not actually linked to the tracking of physical inventory, just inventory totals. However, FIFO makes this assumption in order for ...

What is FIFO accounting?

The first in, first out (FIFO) accounting method relies on a cost flow assumption that removes costs from the inventory account when an item in someone’s inventory has been purchased at varying costs, over time. When a business uses FIFO, the oldest cost of an item in an inventory will be removed first when one of those items is sold. This oldest cost will then be reported on the income statement as part of the cost of goods sold.

What is the last in first out accounting method?

With this accounting technique, the costs of the oldest products will be reported as inventory. It should be understood that, although LIFO matches the most recent costs with sales on the income statement, the flow of costs does not necessarily have to match the flow of the physical units.

What is the weighted average method?

When it comes time for businesses to account for their inventory, they typically use one of three different primary accounting methodologies: the weighted average method, the first in, first out (FIFO) method, or the last in, first out (LIFO) method. The weighted average method is most commonly employed when inventory items are so intertwined ...

When to use weighted average?

The weighted average method, which is mainly utilized to assign the average cost of production to a given product, is most commonly employed when inventory items are so intertwined that it becomes difficult to assign a specific cost to an individual unit. This is frequently the case when the inventory items in question are identical to one another.

Does LIFO match the flow of costs?

It should be understood that, although LIFO matches the most recent costs with sales on the income statement, the flow of costs does not necessarily have to match the flow of the physical units. Generally speaking, FIFO is preferable in times of rising prices, so that the costs recorded are low, and income is higher.

Perpetual LIFO

When using the perpetual system, the Inventory account is constantly (or perpetually) changing. The Inventory account is updated for every purchase and every sale.

Perpetual Average

When using the perpetual inventory system, the Inventory account is constantly (or perpetually) changing. The inventory account is updated for every purchase and every sale.

What is FIFO in accounting?

FIFO is an acronym for first in, first out. Under the FIFO cost flow assumption, the first (oldest) costs are the first costs to leave inventory and be reported as the cost of goods sold on the income statement. The last (or recent) costs will remain in inventory and be reported as inventory on the balance sheet.

What is periodic FIFO?

Periodic FIFO. Periodic means that the Inventory account is not routinely updated during the accounting period. Instead, the cost of merchandise purchased from suppliers is debited to the general ledger account Purchases. At the end of the accounting year the Inventory account is adjusted to equal the cost of the merchandise that has not been sold.

Why is periodic LIFO always higher than first?

If the costs of textbooks continue to increase, periodic LIFO will always result in the least amount of profit. The reason is that the last costs will always be higher than the first costs. Higher costs result in less profits and often lower income taxes.

Inventory Valuation and Tracking

Businesses need to keep track of which items they sell and which items they have on hand, including their exact value.

1. The FIFO Method

The FIFO method is the first option for valuing stock and probably the most common.

2. The LIFO Method

Another method that is used, and the opposite of the FIFO method, is LIFO.

3. The Weighted Average Cost Method

The weighted average method is a final option for valuing our inventory.

FIFO vs LIFO vs Weighted Average Around the World

Generally accepted accounting principles in the United States allow for the use of all three inventory methods.

Test Yourself!

Before you start, I would recommend to time yourself to make sure that you not only get the questions right but are completing them at the right speed.

FIFO, LIFO, Weighted Average Method Mini Quiz

1. Computerized inventory systems are most commonly associated with which inventory tracking system? *

Inventories that are not interchangeable

The cost of inventories that are not ordinarily interchangeable should be measured by specifically identifying their costs. This approach should also be followed for items that are segregated for a specific project (IAS 2.23-24).

Interchangeable inventories

Cost of inventories that are interchangeable and are not segregated for a specific project should be assigned using FIFO (First-In, First-Out) or weighted average cost formula. The same cost formula should be applied consistently for all inventories having a similar nature and use to the entity (IAS 2.25-26).

More about IAS 2

Excerpts from IFRS Standards come from the Official Journal of the European Union (© European Union, https://eur-lex.europa.eu). The information provided on this website is for general information and educational purposes only and should not be used as a substitute for professional advice. Use at your own risk.

Fifo and Lifo

What do the accountancy terms FIFO and LIFO mean? The methods FIFO (First In First Out) and LIFO (Last In First Out) define methods used to gather inventory units and determine the Cost of Goods Sold (COGS).

How to calculate FIFO and LIFO?

Consider that there is a watch manufacturing company that gets its units for the last 6 months as follows.

Fifo vs Lifo

If you have a look at the cost of COGS in LIFO, it is more than COGS in FIFO because the order in which the units have been consumed is not the same. In this example as well, we needed to determine the COGS of 250 units.

Ending Inventory

It is the actual amount of products that are available for sale at the end of an auditing period.

References

Business News Daily. (2020, August 28). FIFO vs LIFO: What Is the Difference?

Weighted Average vs. FIFO vs. LIFO: An Overview

Weighted Average

- The weighted average method, which is mainly utilized to assign the average cost of production to a given product, is most commonly employed when inventory items are so intertwined that it becomes difficult to assign a specific cost to an individual unit. This is frequently the case when the inventory items in question are identical to one another. Furthermore, this method assumes …

First In, First Out

- The first in, first out (FIFO) accounting method relies on a cost flow assumption that removes costs from the inventory account when an item in someone’s inventory has been purchased at varying costs, over time. When a business uses FIFO, the oldest cost of an item in an inventory will be removed first when one of those items is sold. This oldest cost will then be reported on the in…

Last In, First Out

- The last in, first out (LIFO) accounting method assumes that the latest items bought are the first items to be sold. With this accounting technique, the costs of the oldest products will be reported as inventory. It should be understood that, although LIFO matches the most recent costs with sales on the income statement, the flow of costs does not necessarily have to match the flow o…

Weighted Average vs. FIFO vs. LIFO Example

- Consider this example: Suppose you own a furniture store and you purchase 200 chairs for $10 per unit. The next month, you buy another 300 chairs for $20 per unit. At the end of an accounting period, let's assume you sold 100 total chairs. The weighted average costs, using both FIFO and LIFO considerations are as follows: 1. 200 chairs at $10 per c...