How do you calculate FIFO and LIFO?

- FIFO accounting results. To calculate the cost of goods sold, start with the oldest units. ...

- LIFO inventory values. Cost of sales using LIFO includes the newest units purchased at $54. ...

- Inventory values when all units are sold. When all 250 units are sold, the entire cost of inventory ($13,100) is posted to the cost of goods sold.

What are the disadvantages of the FIFO accounting method?

FIFO, Average Cost ... It is possible for some investors to use the average cost method of accounting, which averages the cost basis for all shares in the portfolio, and taxable gains are ...

Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

Which is a better method LIFO or FIFO?

FIFO assumes that cheaper items are sold first, generating a higher profit than LIFO. However, when the more expensive items are sold in later months, profit is lower. LIFO generates lower profits in early periods and more profit in later months. FIFO is the easier method to use, and most businesses stick with the FIFO method.

What are the advantages and disadvantages of FIFO?

Advantages: (i) Since materials issued for production are at the original cost, the inventory reflects the current market price, (ii) Profit and Loss Account and the Balance Sheet satisfactorily represent the actual conditions, (iii) When the price level is declining, the FIFO method shows a lower profit for income tax implications, (iv) Next ...

What is FIFO method in accounting?

Key Takeaways First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last.

What is FIFO method with example?

The FIFO method requires that what comes in first goes out first. For example, if a batch of 1,000 items gets manufactured in the first week of a month, and another batch of 1,000 in the second week, then the batch produced first gets sold first. The logic behind the FIFO method is to avoid obsolescence of inventory.

What are the steps for FIFO?

The FIFO procedure follows 5 simple steps:Locate products with the soonest best before or use-by dates.Remove items that are past these dates or are damaged.Place items with the soonest dates at the front.Stock new items behind the front stock; those with the latest dates should be at the back.More items...•

How do you do FIFO journal entries?

1:339:35FIFO Inventory (Part 2) Journal Entries - YouTubeYouTubeStart of suggested clipEnd of suggested clipI remember debits and credits always have to balance. Now with periodic we do not have to adjust forMoreI remember debits and credits always have to balance. Now with periodic we do not have to adjust for inventory okay under periodic we are not recording inventory.

How do you calculate sales using FIFO?

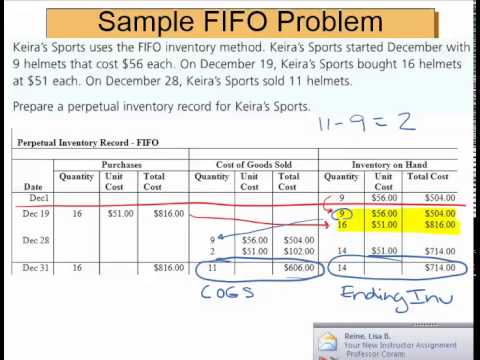

The First-in First-out (FIFO) method of inventory valuation is based on the assumption that the sale or usage of goods follows the same order in which they are bought....For the sale of 250 units:100 units at $2/unit = $200 in COGS.100 units at $3/unit = $300 in COGS.50 units at $4/unit = $200 in COGS.

What is the FIFO method first in first out?

FIFO stands for first in, first out, an easy-to-understand inventory valuation method that assumes that goods purchased or produced first are sold first. In theory, this means the oldest inventory gets shipped out to customers before newer inventory.

How does FIFO costing work?

What is FIFO costing? In simplest terms, FIFO (first-in, first-out) costing allows you to track the cost of an item/SKU based on its cost at purchase order receipt, and apply this cost against each shipment of the item until the receipt quantity is exhausted.

What is LIFO and FIFO with example?

First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method. Last-in, first-out (LIFO) assumes the last inventory added will be the first sold. Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

How do you calculate gross margin for FIFO?

To calculate gross margin, subtract Cost of Goods Sold (COGS) from total revenue and divide that number by total revenue (Gross Margin = (Total Revenue - Cost of Goods Sold)/Total Revenue). The formula to calculate gross margin as a percentage is Gross Margin = (Total Revenue – Cost of Goods Sold)/Total Revenue x 100.

How Do You Calculate FIFO?

To calculate COGS (Cost of Goods Sold) using the FIFO method, determine the cost of your oldest inventory. Multiply that cost by the amount of inventory sold.

What Is FIFO?

FIFO is an acronym. It stands for “First-In, First-Out” and is used for cost flow assumption purposes. Cost flow assumptions refers to the method of moving the cost of a company’s product out of its inventory to its cost of goods sold.

What Is a FIFO and LIFO Example?

Here is an example of a small business using the FIFO and LIFO methods.

What is LIFO in accounting?

LIFO stands for “Last-In, First-Out”. LIFO is the opposite of the FIFO method and it assumes that the most recent items added to a company’s inventory are sold first. The company will go by those inventory costs in the COGS (Cost of Goods Sold) calculation. The LIFO method for financial accounting may be used over FIFO when the cost ...

What is the difference between FIFO and LIFO?

The FIFO (“First-In, First-Out”) method means that the cost of a company’s oldest inventory is used in the COGS (Cost of Goods Sold) calculation. LIFO (“Last-In, First-Out”) means that the cost of a company’s most recent inventory is used instead. Here’s What We’ll Cover:

Why use LIFO or FIFO?

The LIFO method for financial accounting may be used over FIFO when the cost of inventory is increasing, perhaps due to inflation. Using FIFO means the cost of a sale will be higher because the more expensive items in inventory are being sold off first.

When calculating COGS, what is the company going to go by?

Therefore, when calculating COGS (Cost of Goods Sold), the company will go by those specific inventory costs. Although the oldest inventory may not always be the first sold, the FIFO method is not actually linked to the tracking of physical inventory, just inventory totals. However, FIFO makes this assumption in order for ...

What does FIFO mean in accounting?

FIFO stands for “First-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company’s inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation.

Why do investors value FIFO?

Investors and banking institutions value FIFO because it is a transparent method of calculating cost of goods sold. It is also easier for management when it comes to bookkeeping, because of its simplicity.

What Are the Advantages of FIFO?

The FIFO method is considered to me a more trusted method than the LIFO (“Last-In, First-Out”) method. You can read more about why FIFO is preferable here.

Why Would You Use FIFO over LIFO?

Both are legal although the LIFO method is often frowned upon because bookkeeping is far more complex and the method is easy to manipulate.

How to calculate COGS?

To calculate COGS (Cost of Goods Sold) using the FIFO method, determine the cost of your oldest inventory. Multiply that cost by the amount of inventory sold.

What method does Sal use to calculate his cost of goods sold?

January has come along and Sal needs to calculate his cost of goods sold for the previous year, which he will do using the FIFO method.

Why is the LIFO method understated?

The value of remaining inventory, assuming it is not-perishable, is also understated with the LIFO method because the business is going by the older costs to acquire or manufacture that product. That older inventory may, in fact, stay on the books forever. Investors and banking institutions value FIFO because it is a transparent method ...

What is FIFO accounting?

First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last. An alternative to FIFO, LIFO is an accounting method in which assets purchased or acquired last are disposed of first.

What is FIFO method?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

What Are the Advantages of First In, First Out (FIFO)?

The obvious advantage of FIFO is that it's the most widely used method of valuing inventory globally. It is also the most accurate method of aligning the expected cost flow with the actual flow of goods which offers businesses a truer picture of inventory costs . Furthermore, it reduces the impact of inflation, a ssuming that the cost of purchas ing newer inventory will be higher than the purchasing cost of older invent ory. Finally, it reduces the obsolescence of inventory.

What Are the Other Inventory Valuation Methods?

In inflationary economies, this results in deflated net income costs and lower ending balances in inventory when compared to FIFO. Average cost inventory is another method that assigns the same cost to each item and results in net income and ending inventory balances between FIFO and LIFO. Finally, specific inventory tracing is used only when all components attributable to a finished product are known.

What happens when FIFO assigns the oldest costs to the cost of goods sold?

In this situation, if FIFO assigns the oldest costs to the cost of goods sold, these oldest costs will theoretically be priced lower than the most recent inventory purchased at current inflated prices. This lower expense results in higher net income. Also, because the newest inventory was purchased at generally higher prices, the ending inventory balance is inflated.

What is FIFO in manufacturing?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense. Under FIFO, it is assumed that the cost of inventory purchased first will be recognized first. The dollar value of total inventory decreases in this process because inventory has been removed from the company’s ownership. The costs associated with the inventory may be calculated in several ways — one being the FIFO method.

How is inventory assigned?

Inventory is assigned costs as items are prepared for sale. This may occur through the purchase of the inventory or production costs, through the purchase of materials, and utilization of labor. These assigned costs are based on the order in which the product was used, and for FIFO, it is based on what arrived first. For example, if 100 items were purchased for $10 and 100 more items were purchased next for $15, FIFO would assign the cost of the first item resold of $10. After 100 items were sold, the new cost of the item would become $15, regardless of any additional inventory purchases made.

What is FIFO accounting?

In accounting, First In, First Out (FIFO) is the assumption that a business issues its inventory to its customers in the order in which it has been acquired. Under the FIFO Method, inventory acquired by the earliest purchase made by the business is assumed to be issued first to its customers.

Which inventory system provides the same value of ending inventory under the FIFO method?

As we shall see in the following example, both periodic and perpetual inventory systems provide the same value of ending inventory under the FIFO method.

How to find cost valuation of ending inventory?

To find the cost valuation of ending inventory, we need to track the cost of inventory received and assign that cost to the correct issue of inventory according to the FIFO assumption.

What is the value of ending inventory based on?

In the FIFO Method, the value of ending inventory is based on the cost of the most recent purchases.

When a business buys identical inventory units for varying costs over a period of time, it needs to have?

When a business buys identical inventory units for varying costs over a period of time, it needs to have a consistent basis for valuing the ending inventory and the cost of goods sold.

Does periodic inventory give timely inventory management information?

Even though the periodic inventory system provides the value of ending inventory more quickly, it does not give timely inventory management information, making it only suitable for tiny businesses with low stock turnover.

What does FIFO stand for in accounting?

In accounting, FIFO stands for “First In, First Out.” It is an accounting method used for managing and valuing assets that details of which assets purchased or acquired are sold, used, or disposed of first. A simpler way to describe this method is that it assumes the first items placed into inventory will be the first ones to go out, and it is up to bookkeepers to oversee this process for an organization.

Why is FIFO accounting method more reliable?

The FIFO accounting method generates more reliable financial statements because it’s more difficult to manipulate the numbers compared to other valuation methods.

What is FIFO in inventory?

FIFO is a widely used method of valuing inventory all over the world. It is known to be the most accurate method of aligning the expected cost flow with the actual flow of goods, offering businesses a clear picture of inventory costs. It’s also easier to understand and manage versus the other methods. Moreover, most organizations prefer to move their oldest products first before the newer products.

What is the opposite of FIFO?

The most common alternative method to FIFO is the LIFO method, meaning “Last In, First Out.” The LIFO method is the opposite of FIFO because it assumes the last products to enter inventory will move out first.

How does inventory affect tax?

The manner how an organization determines its inventory’s value, determines how much profit they believe the company makes, which ultimately affects how much is paid in income tax. The Internal Revenue Service (IRS) grants businesses the opportunity to deduct the cost of inventory from their taxable income. The lower your company’s profit is, the lower the amount in taxes it has to pay. As an accountant and bookkeeper, it’s important to choose the method that benefits the business during tax season.

How to calculate average cost?

The average cost is calculated by dividing the cost of goods in inventory by the total number of items available for sale. This results in net income and ending inventory balances between FIFO and LIFO.

How to calculate FIFO?

To calculate FIFO, you first have to calculate the cost of goods sold (otherwise known as COGS). Using the FIFO method, determine the cost of your oldest inventory first before the newest. Multiply that cost by the amount of inventory sold. The inventory sold refers to the cost of purchased goods or the cost of produced goods. It’s important to note that even though a company pays a price for its inventory, prices often fluctuate. Fluctuating costs need to be taken into account when calculating inventory valuation.

How to determine inventory cost?

As inventory is usually purchased at different rates (or manufactured at different costs) over an accounting period, there is a need to determine what cost needs to be assigned to inventory. For instance, if a company purchased inventory three times in a year at $50, $60 and $70, what cost must be attributed to inventory at the year end? Inventory cost at the end of an accounting period may be determined in the following ways: 1 First In First Out (FIFO) 2 Last In First Out (LIFO) 3 Average Cost Method (AVCO) 4 Actual Unit Cost Method

How is the cost of inventory sold determined?

Theoretically, the cost of inventory sold could be determined in two ways. One is the standard way in which purchases during the period are adjusted for movements in inventory. The second way could be to adjust purchases and sales of inventory in the inventory ledger itself.

Is inventory accounted for separately from sales?

However, as we shall see in following sections, inventory is accounted for separately from purchases and sales through a single adjustment at the year end.

What is FIFO in accounting?

The company makes a physical count at the end of each accounting period to find the number of units in ending inventory. The company then applies first-in, first-out (FIFO) method to compute the cost of ending inventory.

What is FIFO in inventory?

First-in, first-out (FIFO) method in periodic inventory system. Under first-in, first-out (FIFO) method, the costs are chronologically charged to cost of goods sold (COGS) i.e., the first costs incurred are first costs charged to cost of goods sold (COGS).

How to calculate cost of goods sold?

Formula method: Under formula method, the cost of goods sold would be computed as follows: Cost of goods sold = Cost of units in beginning inventory + Cost of units purchased during the period – Cost of units in ending inventory.

What is FIFO method?

The use of FIFO method is very common to compute cost of goods sold and the ending balance of inventory under both perpetual and periodic inventory systems. The example given below explains the use of FIFO method in a perpetual inventory system. If you want to understand its use in a periodic inventory system, read “ first-in, ...

What is FIFO in inventory?

The first-in, first-out (FIFO) method is a widely used inventory valuation method that assumes that the goods are sold (by merchandising companies) or materials are issued to production department (by manufacturing companies) in the order in which they are purchased. In other words, the costs to acquire merchandise or materials are charged ...

What is FIFO in fine electronics?

The Fine Electronics company uses perpetual inventory system to account for acquisition and sale of inventory and first-in, first-out (FIFO) method to compute cost of goods sold and for the valuation of ending inventory. The company has made the following purchases and sales during the month of January 2016.

How much did Fine Electronics sell for in 2016?

January 4:#N#The Fine electronics company has sold 16 units for $25,600 (16 units × $1,600) on January 4, 2016. On this date, 24 units in the beginning inventory are the only units available for sale. The cost of goods sold is, therefore, $16,000 (16 × $1,000). Since the company uses perpetual inventory system, two journal entries would be made for the sale of inventory – one to reduce the inventory account by the cost of 16 units and one to record the sale of 16 units. These two journal entries are given below:

Can you compute the cost of goods sold and ending inventory?

With the help of the above inventory card, we can easily compute the cost of goods sold and ending inventory.

FIFO vs. LIFO

- To reiterate, FIFO expenses the oldest inventories first. In the following example, we will compare FIFO to LIFO (last in first out)Last-In First-Out (LIFO)The Last-in First-out (LIFO) method of inventory valuation is based on the practice of assets produced or acquired last being the first to be. LIFO expenses the most recent costs first. Consider the same example above. Recall that un…

Impact of FIFO Inventory valuation Method on Financial Statements

- Recall the comparison example of First-In First-Out and LIFO. The two methods yield different inventory and COGS. Now it is important to consider the impact of using FIFO on a company’s financial statements?

Key Takeaways from First-In First-Out

- FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold.

- It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system.

- FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold.

- It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system.

- It provides a poor matching of revenue with expenses.

Related Reading

- CFI is a global provider of financial analyst training and career advancement for finance professionals, including the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll t…