To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

What is LIFO method with example?

The advantages of LIFO method are as follows:

- LIFO method is easy to implement and understand.

- It provides tax benefits to the business organisations by reporting less profits and deferring Income Tax payment in the future years.

- LIFO method provides the benefit of matching the current cost with the current revenues thereby reducing the profits included in the inventory.

What is the difference between FIFO vs. LIFO?

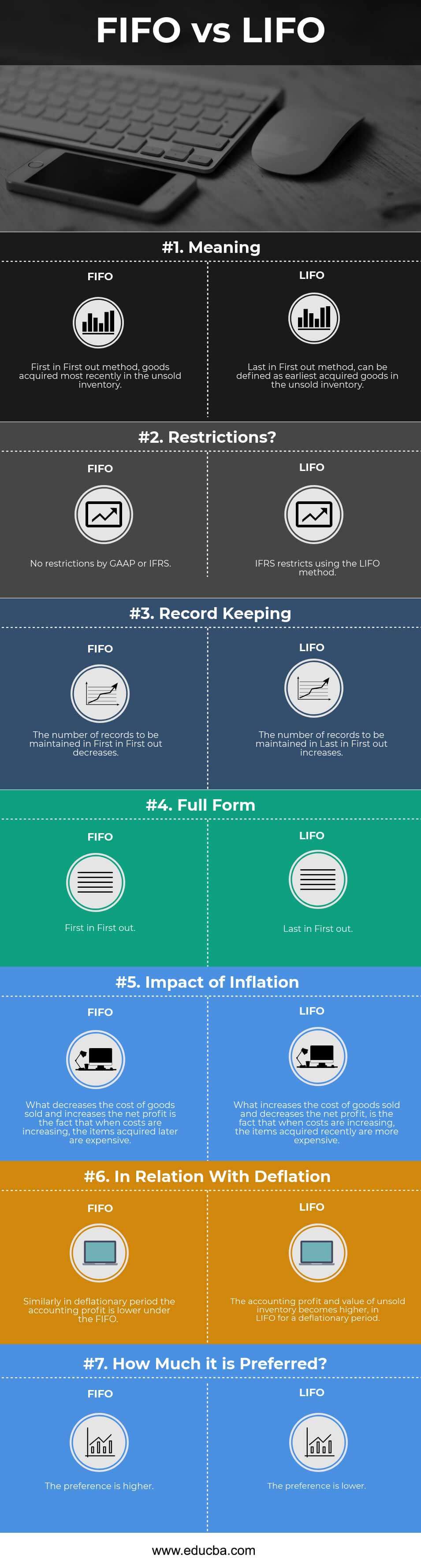

- First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method.

- Last-in, first-out (LIFO) assumes the last inventory added will be the first sold.

- Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

How do you calculate gross profit using FIFO?

What are the benefits of good stock rotation?

- Increases productivity and efficiency.

- Creates a more organised warehouse.

- Helps save time and money.

- Improves accuracy of inventory orders.

- Keeps customers coming back for more.

How to use the FIFO method?

The advantages to the FIFO method are as follows:

- The method is easy to understand, universally accepted and trusted.

- FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first). ...

- Less waste (a company truly following the FIFO method will always be moving out the oldest inventory first).

What is LIFO and FIFO with example?

First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method. Last-in, first-out (LIFO) assumes the last inventory added will be the first sold. Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

What is FIFO method with example?

Example of FIFO Imagine if a company purchased 100 items for $10 each, then later purchased 100 more items for $15 each. Then, the company sold 60 items. Under the FIFO method, the cost of goods sold for each of the 60 items is $10/unit because the first goods purchased are the first goods sold.

How do you solve FIFO questions?

3:0515:57FIFO Method (First In First Out) Store Ledger Account- Problem - YouTubeYouTubeStart of suggested clipEnd of suggested clipRight you purchase them see you on for general you purchase 20 Gandhi on second January you purchaseMoreRight you purchase them see you on for general you purchase 20 Gandhi on second January you purchase 30 on 31 or you purchase 40 and in these prices.

How do you calculate FIFO average?

2:319:46FIFO LIFO Weighted Average Examples - YouTubeYouTubeStart of suggested clipEnd of suggested clipThat I'm going to sell all those ones at sixteen cost 51. So I will also sell two at 51. Add thoseMoreThat I'm going to sell all those ones at sixteen cost 51. So I will also sell two at 51. Add those together that means my cost of goods sold I sold 11.

What is LIFO example?

Example of LIFO that buys coffee mugs from wholesalers and sells them on the internet. One Cup's cost of goods sold (COGS) differs when it uses LIFO versus when it uses FIFO. In the first scenario, the price of wholesale mugs is rising from 2016 to 2019.

How do you calculate cost of goods sold using LIFO?

2:458:12LIFO Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipFrom which dates with which prices are going to go on the cost of goods sold and which are going toMoreFrom which dates with which prices are going to go on the cost of goods sold and which are going to be in our ending inventory and we're making an assumption and in this case we're going to assume.

How do you calculate cost of goods sold and ending inventory using FIFO?

2:558:04FIFO Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipWe make a cost flow assumption to tell us which units we're going to assume it that actually help usMoreWe make a cost flow assumption to tell us which units we're going to assume it that actually help us compute cost of goods sold and the ending inventory. So in this case because we're using FIFO. Let

What is LIFO method?

Key Takeaways Last in, first out (LIFO) is a method used to account for inventory. Under LIFO, the costs of the most recent products purchased (or produced) are the first to be expensed. LIFO is used only in the United States and governed by the generally accepted accounting principles (GAAP).

How do you calculate weighted average LIFO and FIFO?

4:036:38FIFO vs. LIFO vs. Weighted Average Cost - YouTubeYouTubeStart of suggested clipEnd of suggested clipMeans lower net income fifo we get the lower cost of goods sold. So we have higher net income. So ifMoreMeans lower net income fifo we get the lower cost of goods sold. So we have higher net income. So if you're comparing two companies. And prices were going up all else equal the one with fifo.

How do you do LIFO charts?

0:004:22LIFO Inventory Chart - YouTubeYouTubeStart of suggested clipEnd of suggested clipSystem so here we go our beginning inventory was four hundred and twenty units at eight. Dollars.MoreSystem so here we go our beginning inventory was four hundred and twenty units at eight. Dollars. Our next transaction I was on April 10th we sold 300 units. So I come to my cost of merchandise sold.

How do you calculate gross profit using LIFO?

Calculate gross profit by deducting cost of sales from total revenues. Using the LIFO example, if the business had made $400 through selling its 15 units, its total revenue is $400 and thus its gross profit after subtracting the $210 is $190.

How do you calculate net income from FIFO?

1:028:30LIFO And FIFO Inventory Accounting (Comparing Net Income & Ending ...YouTubeStart of suggested clipEnd of suggested clipThousand three hundred dollars that's based on using these earlier purchases here first the costMoreThousand three hundred dollars that's based on using these earlier purchases here first the cost there don't go and cost out our sales.

What is FIFO in accounting?

FIFO and LIFO are methods used in the cost of goods sold calculation. FIFO (“First-In, First-Out”) assumes that the oldest products in a company’s inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company’s inventory have been sold first ...

Why are FIFO profits more accurate?

Although this may mean less tax for a company to pay under LIFO, it also means stated profits with FIFO are much more accurate because older inventory reflects the actual costs of that inventory. If profits are naturally high under FIFO, then the company becomes that much more attractive to investors.

What is LIFO reserve?

The LIFO reserve is the amount by which a company’s taxable income has been deferred, as compared to the FIFO method. The remaining unsold 350 televisions will be accounted for in “inventory”.

Is LIFO more attractive than FIFO?

You can see how for Ted, the LIFO method may be more attractive than FIFO. This is because the LIFO number reflects a higher inventory cost, meaning less profit and less taxes to pay at tax time. The LIFO reserve in this example is $31,250.

Is LIFO legal in the US?

Under GAAP, LIFO is legal. Outside the United States, LIFO is not permitted as an accounting practice. This is why you’ll see some American companies use the LIFO method on their financial statements, and switch to FIFO for their international operations.

Why is LIFO not accurate?

As a result, LIFO doesn't provide an accurate or up-to-date value of inventory because the valuation is much lower than inventory items at today's prices.

What is LIFO method?

LIFO. When sales are recorded using the LIFO method, the most recent items of inventory are used to value COGS and are sold first. In other words, the older inventory, which was cheaper, would be sold later.

What would happen if inflation was nonexistent?

If inflation were nonexistent, then all three of the inventory valuation methods would produce the same exact results. Inflation is a measure of the rate of price increases in an economy. When prices are stable, our bakery example from earlier would be able to produce all of its bread loaves at $1, and LIFO, FIFO, and average cost would give us a cost of $1 per loaf. However, in the real world, prices tend to rise over the long term, which means that the choice of accounting method can affect the inventory valuation and profitability for the period. 1

What is FIFO in accounting?

The First-In, First-Out (FIFO) method assumes that the first unit making its way into inventory–or the oldest inventory–is the sold first. For example, let's say that a bakery produces 200 loaves of bread on Monday at a cost of $1 each, and 200 more on Tuesday at $1.25 each. FIFO states that if the bakery sold 200 loaves on Wednesday, the COGS ( on the income statement) is $1 per loaf because that was the cost of each of the first loaves in inventory. The $1.25 loaves would be allocated to ending inventory ( on the balance sheet ).

Why would COGS be higher under LIFO?

In an inflationary environment, the current COGS would be higher under LIFO because the new inventory would be more expensive. As a result, the company would record lower profits or net income for the period. However, the reduced profit or earnings means the company would benefit from a lower tax liability.

Why is FIFO better than COGS?

FIFO can be a better indicator of the value for ending inventory because the older items have been used up while the most recently acquired items reflect current market prices. For most companies, FIFO is the most logical choice since they typically use their oldest inventory first in the production of their goods, which means the valuation of COGS reflects their production schedule.

What is the first in first out method?

The First-In, First-Out (FIFO) method assumes that the oldest unit of inventory is the sold first. LIFO is not realistic for many companies because they would not leave their older inventory sitting idle in stock. FIFO is the most logical choice since companies typically use their oldest inventory first in the production of their goods.

Understanding the inventory formula

Beginning inventory + purchases = goods available for sale – cost of goods sold (COGS) = ending inventory

How are FIFO and LIFO methods different?

FIFO and LIFO inventory valuations differ because each method makes a different assumption about the units sold. To understand FIFO vs. LIFO flow of inventory, you need to visualize inventory items sitting on the shelf, each with a cost assigned to it.

How do you calculate FIFO and LIFO?

To explain inventory valuation in detail, assume that Sterling Fashions sells a line of men’s shirts and that the store had no beginning inventory balance on March 1st. Here is the inventory activity for March:

How do FIFO and LIFO affect more straightforward accounting operations?

Using FIFO simplifies the accounting process because the oldest items in inventory are assumed to be sold first. When Sterling uses FIFO, all of the $50 units are sold first, followed by the items at $54.

Industry, regulatory and tax considerations

Accountants use “inventoriable costs” to define all expenses required to obtain inventory and prepare the items for sale. For retailers and wholesalers, the largest inventoriable cost is the purchase cost.

Final thoughts

The FIFO and LIFO methods impact your inventory costs, profit, and your tax liability. Keep your accounting simple by using the FIFO method of accounting, and discuss your company’s regulatory and tax issues with a CPA.

Methods of calculating inventory cost

As inventory is usually purchased at different rates (or manufactured at different costs) over an accounting period, there is a need to determine what cost needs to be assigned to inventory.

First In First Out (FIFO)

This method assumes that inventory purchased first is sold first. Therefore, inventory cost under FIFO method will be the cost of latest purchases. Consider the following example:

Example

Bike LTD purchased 10 bikes during January and sold 6 bikes, details of which are as follows: