Calculating ending inventory

- First-in, first-out (FIFO) method. This method of calculating ending inventory is based on the assumption that the oldest items bought for the production of goods were sold first.

- Last-in, first-out (LIFO) method. The last-in, first-out method is when a company determines its ending inventory by looking at the cost of the last item purchased.

- Weighted-average cost (WAC) method. The weighted-average cost method gives a value to the ending inventory and COGS derived from the total cost of products produced or bought in an accounting ...

How to calculate beginning and ending inventory?

Let’s break down the steps for how to find beginning inventory:

- Determine the cost of goods sold (COGS) using your previous accounting period’s records. a. ...

- Multiply your ending inventory balance by the production cost of each inventory item. Do the same with the amount of new inventory. ...

- Add the ending inventory and cost of goods sold. ...

How to calculate the value of ending inventory?

How to calculate ending inventory

- Example of the Ending Inventory Calculation. A business has $100,000 of beginning inventory, purchases an additional $250,000 of inventory during the month, and sells off $300,000 of it during the ...

- Lower of Cost or Market Rule. ...

- Inventory Valuation Methods. ...

- Related Courses

What is the formula for ending inventory?

Ending inventory methods and examples

- First-in, first-out (FIFO) method. The first in, first out (FIFO) method assumes that the oldest items in inventory are sold first. ...

- Last-in, first out (LIFO) method. To understand the LIFO method, think about buying milk at the grocery store. ...

- Weighted average cost method. ...

- Impact on profit. ...

How do you calculate desired ending inventory?

The calculation is:

- Calculate the cost-to-retail percentage, for which the formula is (Cost / Retail price).

- Calculate the cost of goods available for sale, for which the formula is (Cost of beginning inventory + Cost of purchases).

- Calculate the cost of sales during the period, for which the formula is (Sales x cost-to-retail percentage).

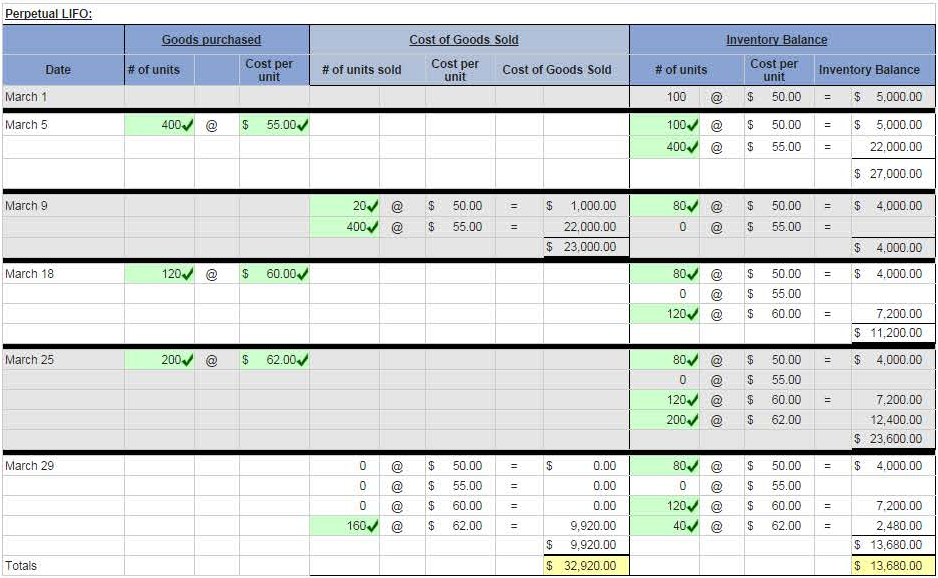

How do you calculate ending inventory using LIFO FIFO?

2:253:29LIFO FIFO INVENTORY in less than 4 minutes! - YouTubeYouTubeStart of suggested clipEnd of suggested clipAnd paste less taxes. You want to figure you want to use LIFO. Now what about if they ask me for theMoreAnd paste less taxes. You want to figure you want to use LIFO. Now what about if they ask me for the average cost method this one is actually the easiest one and it is what the question is a day the

How do you calculate the ending inventory?

To calculate the ending inventory, the new purchases are added to the ending inventory, minus the cost of goods sold. This provides the final value of the inventory at the end of the accounting period. The ending inventory is based on the market value or the lowest value of the goods that the business possesses.

How do you calculate ending inventory using FIFO in Excel?

Inventory Formula – Example #2FIFO Method. Ending Inventory is calculated using the formula given below. Ending Inventory = Total Inventory – Total Sold Inventory. ... LIFO Method. Ending Inventory is calculated using the formula given below. Ending Inventory = Total Inventory – Total Sold Inventory. ... Weighted Average Cost Method.

Is ending inventory FIFO or LIFO?

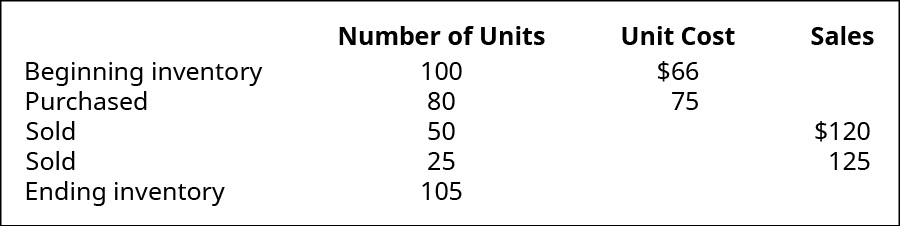

Under LIFO, the last units purchased are sold first; this leaves the oldest units at $8 still in inventory. With FIFO, the oldest units at $8 were sold, leaving the newest units purchased at $11 remaining in inventory. The ending inventory value using FIFO: 1,000 units x $11 = $11,000.

What is FIFO method with example?

Example of FIFO Imagine if a company purchased 100 items for $10 each, then later purchased 100 more items for $15 each. Then, the company sold 60 items. Under the FIFO method, the cost of goods sold for each of the 60 items is $10/unit because the first goods purchased are the first goods sold.

What is the FIFO method?

FIFO stands for “First-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company's inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation.

How do you calculate cost of goods sold using FIFO?

With this method, companies add up the total cost of goods purchased or produced during a specified time. This amount is then divided by the number of items the company purchased or produced during that same period. This gives the company an average cost per item.

How do you calculate FIFO and LIFO periodic?

1:334:41LIFO Periodic Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipSo cost of goods sold is gonna be 25. At $50 a unit and 15 at $40 a unit under LIFO with theMoreSo cost of goods sold is gonna be 25. At $50 a unit and 15 at $40 a unit under LIFO with the periodic method that's gonna be the cost of goods sold.

What is the end inventory formula?

Ending Inventory formula calculates the value of goods available for sale at the end of the accounting period. Usually, it is recorded on the balance sheet at the lower of cost or its market value.

What is the last in first out inventory method?

Under Last In First Out Inventory Method Last In First Out Inventory Method LIFO (Last In First Out) is one accounting method for inventory valuation on the balance sheet. LIFO accounting means inventory acquired at last would be used up or sold first. read more, the last item purchased is the cost of the first item sold, which results in the closing Inventory reported by the Business on its Balance Sheet depicts the cost of the earliest items purchased. Ending Inventory is valued on the Balance Sheet The Balance Sheet A balance sheet is one of the financial statements of a company that presents the shareholders' equity, liabilities, and assets of the company at a specific point in time. It is based on the accounting equation that states that the sum of the total liabilities and the owner's capital equals the total assets of the company. read more using the earlier costs, and in an inflationary environment LIFO ending Inventory is less than the current cost. Thus in an Inflationary environment i.e., when prices are rising, it will be lower.

What is closing stock?

It also Known as Closing Stock Known As Closing Stock Closing stock or inventory is the amount that a company still has on its hand at the end of a financial period. It may include products getting processed or are produced but not sold. Raw materials, work in progress, and final goods are all included on a broad level. read more and normally comprises three types of Inventory Types Of Inventory Direct material inventory, work in progress inventory, and finished goods inventory are the three types of inventories. The raw material is direct material inventory, work in progress inventory is partially completed inventory, and finished goods inventory is stock that has completed all stages of production. read more namely:

What is the ending inventory formula?

Ending Inventory The ending inventory formula computes the total value of finished products remaining in stock at the end of an accounting period for sale. It is evaluated by deducting the cost of goods sold from the total of beginning inventory and purchases. read more

What is FIFO valuation?

Under the FIFO method of accounting inventory valuation, the goods which are purchased at the earliest are the first one to be removed from the inventory account. This results in remaining inventory at books to be valued at the most recent price for which the last stock of inventory is purchased. This results in inventory assets recorded on the balance sheet at the most recent costs.

What are the disadvantages of FIFO accounting?

One of the biggest disadvantages of FIFO accounting method is inventory valuation during inflation, First In First Out method will result in higher profits, and thus will results in higher “Tax Liabilities” in that particular period. This may result in increased tax charges and higher tax-related cash outflows.

Why is FIFO accounting used?

FIFO method of accounting saves time, and money spends in calculating the exact inventory cost that is being sold because the recording of inventory is done in the same order as they are purchased or produced. Easy to understand.

What method does ABC use for inventory valuation?

ABC Corporation uses the FIFO method of inventory valuation for the month of December. During that month, it records the following transactions:

Which method of inventory valuation gives the most accurate calculation of the inventory and sales profit?

A business which is in the trading of perishable items generally sells the items which are purchased earliest first, FIFO method of inventory valuation generally gives the most accurate calculation of the inventory and sales profit. Other examples include retail businesses that sell foods or other products with an expiration date.

How are inventory costs reported?

Inventory costs are reported either on the balance sheet, or they are transferred to the income statement as an expense to match against sales revenue. When inventories are used up in production or are sold, their cost is transferred from the balance sheet to the income statement as cost of goods sold.