How to use the FIFO LIFO calculator?

- Enter "units".

- Type in "costs".

- Type the total units solved in the textbox.

- Click " Calculate Fifo " or " Calculate Lifo " according to your need.

What is the difference between FIFO and average method?

Difference between FIFO and average costing method: 1. Primary distinction: The primary difference between the two methods is the cost ascertained to the inventory that is dispatched or sold by a business. In FIFO method, the basic assumption followed is that inventory which is acquired first or enters the business first will be the first to exit.

Which is a better method LIFO or FIFO?

FIFO assumes that cheaper items are sold first, generating a higher profit than LIFO. However, when the more expensive items are sold in later months, profit is lower. LIFO generates lower profits in early periods and more profit in later months. FIFO is the easier method to use, and most businesses stick with the FIFO method.

How to make a FIFO formula in Excel?

Learn Excel: how to make a fifo formula in exce

- The value of what you have left + value of the newly received stock is your total cost. ...

- How To Enter A Formula Into An Excel Spreadsheet Youtube Excel Spreadsheets Excel Math Formulas . ...

- how to make a fifo formula in excel. how to make sales report in excel with formula. ...

- Love Microsoft Excel? This clip contains a tip that just might induce you to. ...

What are the disadvantages of the FIFO accounting method?

FIFO, Average Cost ... It is possible for some investors to use the average cost method of accounting, which averages the cost basis for all shares in the portfolio, and taxable gains are ...

What is FIFO method with example?

Example of FIFO Imagine if a company purchased 100 items for $10 each, then later purchased 100 more items for $15 each. Then, the company sold 60 items. Under the FIFO method, the cost of goods sold for each of the 60 items is $10/unit because the first goods purchased are the first goods sold.

How do you calculate cost using FIFO?

2:378:04FIFO Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipLet's just say we take all these t-shirts. And we just throw them in one big pile. So we just gotMoreLet's just say we take all these t-shirts. And we just throw them in one big pile. So we just got one big pile of inventory. And so when we sell the 250. We don't know which ones they were that we

How do you find ending inventory using FIFO?

According to the FIFO method, the first units are sold first, and the calculation uses the newest units. So, the ending inventory would be 1,500 x 10 = 15,000, since $10 was the cost of the newest units purchased. The ending inventory for Harod's company would be $15,000.

How do you calculate gross profit using the FIFO method?

For example, suppose a company's oldest inventory cost $200, the newest cost $400, and it has sold one unit for $1,000. Gross profit would be calculated as $800 under LIFO and $600 under FIFO.

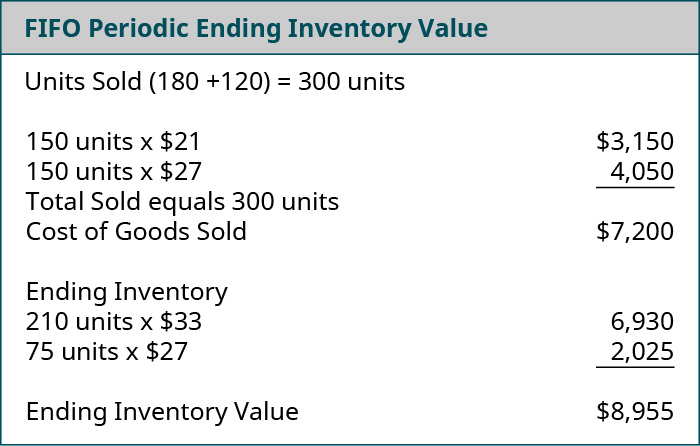

How do you calculate cost of goods sold using the FIFO periodic inventory method?

1:554:57FIFO Periodic Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipSo then the next 20 units are gonna come out of this 30 from January 6 purchase. So that's 20 unitsMoreSo then the next 20 units are gonna come out of this 30 from January 6 purchase. So that's 20 units at $40 a unit. So we add those together and that gives us $1,500. As our cost of goods sold.

How is FIFO depth calculated?

Example : FIFO Depth Calculation If if we have alternate read cycles i.e between two read cycle there is IDLE cycle. If 10 IDLE cycles betweeen two read cycles . FIFO DEPTH = B - B *F2/(F1*10) .

How do you calculate inventory order?

Take the average number of days (lead time) between ordering items and having these items ready for sale. Multiply this by your average daily sales volume over the past month/quarter/year. Then add your safety stock number.

What is FIFO and LIFO example?

Ending Inventory per LIFO: 1,000 units x $8 = $8,000. Remember that the last units in (the newest ones) are sold first; therefore, we leave the oldest units for ending inventory. Ending Inventory per FIFO: 1,000 units x $15 each = $15,000.

How do I calculate inventory?

The basic formula for calculating ending inventory is: Beginning inventory + net purchases – COGS = ending inventory. Your beginning inventory is the last period's ending inventory. The net purchases are the items you've bought and added to your inventory count.

How do you solve FIFO problems?

To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

How do you calculate weighted average LIFO and FIFO?

4:036:38FIFO vs. LIFO vs. Weighted Average Cost - YouTubeYouTubeStart of suggested clipEnd of suggested clipMeans lower net income fifo we get the lower cost of goods sold. So we have higher net income. So ifMoreMeans lower net income fifo we get the lower cost of goods sold. So we have higher net income. So if you're comparing two companies. And prices were going up all else equal the one with fifo.

How do you calculate profit using LIFO?

Calculate gross profit by deducting cost of sales from total revenues. Using the LIFO example, if the business had made $400 through selling its 15 units, its total revenue is $400 and thus its gross profit after subtracting the $210 is $190.

What is FIFO expense?

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

What is the benefit of using FIFO?

1. Better valuation of inventory . By using FIFO, the balance sheet shows a better approximation of the market value of inventory. The latest costs for manufacturing or acquiring the inventory are reflected in inventory, and therefore, the balance sheet reflects the approximate current market value.

Can you use LIFO in Canada?

Therefore, we can see that the balances for COGS and inventory depend on the inventory valuation method. For income tax purposes in Canada, companies are not permitted to use LIFO. However, US companies are able to use FIFO or LIFO.

How to calculate FIFO?

To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

What does FIFO mean?

FIFO is an acronym. It stands for “First-In, First-Out” and is used for cost flow assumption purposes. Cost flow assumptions refers to the method of moving the cost of a company’s product out of its inventory to its cost of goods sold.

What is LIFO in accounting?

LIFO stands for “Last-In, First-Out”. LIFO is the opposite of the FIFO method and it assumes that the most recent items added to a company’s inventory are sold first. The company will go by those inventory costs in the COGS (Cost of Goods Sold) calculation. The LIFO method for financial accounting may be used over FIFO when the cost ...

What is the difference between FIFO and LIFO?

The FIFO (“First-In, First-Out”) method means that the cost of a company’s oldest inventory is used in the COGS (Cost of Goods Sold) calculation. LIFO (“Last-In, First-Out”) means that the cost of a company’s most recent inventory is used instead. Here’s What We’ll Cover:

Why use LIFO or FIFO?

The LIFO method for financial accounting may be used over FIFO when the cost of inventory is increasing, perhaps due to inflation. Using FIFO means the cost of a sale will be higher because the more expensive items in inventory are being sold off first.

When calculating COGS, what is the company going to go by?

Therefore, when calculating COGS (Cost of Goods Sold), the company will go by those specific inventory costs. Although the oldest inventory may not always be the first sold, the FIFO method is not actually linked to the tracking of physical inventory, just inventory totals. However, FIFO makes this assumption in order for ...

What is FIFO in accounting?

FIFO is the default method of determining inventory value. If you want to use LIFO, you must meet some specific requirements and file an application using IRS Form 970.

What is the difference between LIFO and FIFO?

Under FIFO, the cost of goods sold will be lower and the closing inventory will be higher. However, in times of falling prices, the opposite will hold. 2 . FIFO is the default method of determining inventory value.

What is FIFO in 2021?

Updated February 07, 2021. FIFO is one of several ways to calculate the cost of inventory in a business. The other common inventory calculation methods are LIFO (last-in, first-out) and average cost. FIFO, which stands for "first-in, first-out," is an inventory costing method that assumes that the first items placed in inventory are the first sold.

What is specific identification?

Instead of using FIFO, some businesses use one of these other inventory costing methods : Specific identification is used when specific items can be identified. For example, the cost of antiques or collectibles, fine jewelry, or furs can be determined individually, usually through appraisals.

What does FIFO mean in accounting?

FIFO stands for “First-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company’s inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation.

Why is FIFO preferred?

The advantages to the FIFO method are as follows: The method is easy to understand, universally accepted and trusted. FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first).

How to calculate COGS?

To calculate COGS (Cost of Goods Sold) using the FIFO method, determine the cost of your oldest inventory. Multiply that cost by the amount of inventory sold.

What method does Sal use to calculate his cost of goods sold?

January has come along and Sal needs to calculate his cost of goods sold for the previous year, which he will do using the FIFO method.

Why is the LIFO method understated?

The value of remaining inventory, assuming it is not-perishable, is also understated with the LIFO method because the business is going by the older costs to acquire or manufacture that product. That older inventory may, in fact, stay on the books forever. Investors and banking institutions value FIFO because it is a transparent method ...

Why do investors value FIFO?

Investors and banking institutions value FIFO because it is a transparent method of calculating cost of goods sold. It is also easier for management when it comes to bookkeeping, because of its simplicity.

Which countries use FIFO?

Outside the United States, many countries, such as Canada, India and Russia are required to follow the rules set down by the IFRS (International Financial Reporting Standards) Foundation. The IFRS provides a framework for globally accepted accounting standards, among them is the requirements that all companies calculate cost of goods sold using the FIFO method. As such, many businesses, including those in the United States, make it a policy to go with FIFO.

What is FIFO accounting?

In accounting, First In, First Out (FIFO) is the assumption that a business issues its inventory to its customers in the order in which it has been acquired. Under the FIFO Method, inventory acquired by the earliest purchase made by the business is assumed to be issued first to its customers.

Which inventory system provides the same value of ending inventory under the FIFO method?

As we shall see in the following example, both periodic and perpetual inventory systems provide the same value of ending inventory under the FIFO method.

How to find cost valuation of ending inventory?

To find the cost valuation of ending inventory, we need to track the cost of inventory received and assign that cost to the correct issue of inventory according to the FIFO assumption.

What is the value of ending inventory based on?

In the FIFO Method, the value of ending inventory is based on the cost of the most recent purchases.

What is FIFO in accounting?

The company makes a physical count at the end of each accounting period to find the number of units in ending inventory. The company then applies first-in, first-out (FIFO) method to compute the cost of ending inventory.

What is FIFO in inventory?

First-in, first-out (FIFO) method in periodic inventory system. Under first-in, first-out (FIFO) method, the costs are chronologically charged to cost of goods sold (COGS) i.e., the first costs incurred are first costs charged to cost of goods sold (COGS).

How to calculate cost of goods sold?

Formula method: Under formula method, the cost of goods sold would be computed as follows: Cost of goods sold = Cost of units in beginning inventory + Cost of units purchased during the period – Cost of units in ending inventory.

How to calculate number of units issued?

Number of units issued = Units in beginning inventory + Units purchased during the period – Units in ending inventory

What is FIFO method?

The use of FIFO method is very common to compute cost of goods sold and the ending balance of inventory under both perpetual and periodic inventory systems. The example given below explains the use of FIFO method in a perpetual inventory system. If you want to understand its use in a periodic inventory system, read “ first-in, ...

What is FIFO in inventory?

The first-in, first-out (FIFO) method is a widely used inventory valuation method that assumes that the goods are sold (by merchandising companies) or materials are issued to production department (by manufacturing companies) in the order in which they are purchased. In other words, the costs to acquire merchandise or materials are charged ...

What is FIFO in fine electronics?

The Fine Electronics company uses perpetual inventory system to account for acquisition and sale of inventory and first-in, first-out (FIFO) method to compute cost of goods sold and for the valuation of ending inventory. The company has made the following purchases and sales during the month of January 2016.

Can you compute the cost of goods sold and ending inventory?

With the help of the above inventory card, we can easily compute the cost of goods sold and ending inventory.

Example of First-In, First-Out

- Company A reported beginning inventories of 100 units at $2/unit. Also, the company made purchases of: 1. 100 units @ $3/unit 2. 100 units @ $4/unit 3. 100 units @ $5/unit If the company sold 250 units, the order of cost expenses would be as follows: As illustrated above, the cost of goods sold (COGS)Cost of Goods Sold (COGS)Cost of Goods Sold (COG...

FIFO vs. LIFO

- To reiterate, FIFO expenses the oldest inventories first. In the following example, we will compare FIFO to LIFO (last in first out)Last-In First-Out (LIFO)The Last-in First-out (LIFO) method of inventory valuation is based on the practice of assets produced or acquired last being the first to be. LIFO expenses the most recent costs first. Consider the same example above. Recall that un…

Impact of FIFO Inventory valuation Method on Financial Statements

- Recall the comparison example of First-In First-Out and LIFO. The two methods yield different inventory and COGS. Now it is important to consider the impact of using FIFO on a company’s financial statements?

Key Takeaways from First-In First-Out

- FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold.

- It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system.

- It provides a poor matching of revenue with expenses.

Related Reading

- CFI is a global provider of financial analyst training and career advancement for finance professionals, including the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll t…

Why Value Inventory?

Inventory Costing Explained

- The calculation of inventory cost is an important part of filing your business tax return. Like other legitimate business costs, the cost of the products you buy to resell can be deducted from your business income to reduce your taxes. At the beginning of the year, you have an initial inventory of products in various stages of completion or ready to be sold. During the year, you buy more inve…

Calculating Inventory Cost Using FIFO

- Here is how inventory cost is calculated using the FIFO method: Assume a product is made in three batches during the year. The costs and quantity of each batch are: 1. Batch 1: Quantity 2,000 pieces, Cost to produce $8000 2. Batch 2: Quantity 1,500 pieces, Cost to produce $7000 3. Batch 3: Quantity 1,700 pieces, Cost to produce $7700 4. Total produ...

Other Costing Methods

- Instead of using FIFO, some businesses use one of these other inventory costing methods: 1. Specific identificationis used when specific items can be identified. For example, the cost of antiques or collectibles, fine jewelry, or furs can be determined individually, usually through appraisals. 2. LIFO costing ("last-in, first-out") considers the last produced products as being tho…