The formula to compute equivalent units of production under FIFO method is given below: Equivalent units under FIFO method = Percentage of work done on beginning inventory in current period + Units started and completed during current period + Percentage of work done on ending inventory in current period

How do you calculate equivalent units in FIFO?

Equivalent units under FIFO method are calculated using the following formula: Equivalent units for each cost component = (100% − A) × B + C + D × E. Where, A = percentage of completion at the end of last period. B = units in opening work in process.

How does the FIFO method work?

First, the FIFO method divides the units transferred out into two parts – the units completed and transferred out that belong to beginning inventory and the units completed and transferred out that belong to production started during the period.

What are beginning and ending inventories in FIFO?

In FIFO, both beginning and ending inventories are essentially converted to an equivalent units basis. The equivalent units belonging to beginning inventory represent the work done during the current period to complete the units that were not completed in the previous period.

Which expense is expensed first in the FIFO system?

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

How do you calculate units started and completed?

Therefore, the started and completed unit of 75,000 units was computed by deducting the ending WIP (5,000 units) and beginning WIP (10,000 units) from the total units to account for of 90,000 units....1-on-1 CMA Coaching Support.Beginning WIP10,000Started units this period80,000Total units to account for90,0001 more row

How do you find units in FIFO?

5:547:52Cost Per Equivalent Unit, FIFO Method, Part 1 - YouTubeYouTubeStart of suggested clipEnd of suggested clipNow we can go about calculating the cost per equivalent unit. So we need to know under the FIFOMoreNow we can go about calculating the cost per equivalent unit. So we need to know under the FIFO method we're going to need to know the cost that were added during the period.

How do you calculate units completed and transferred?

To calculate the goods transferred out, simply take the units transferred out times the sum of the two equivalent unit costs (materials and conversion) because all items transferred to the next department are complete with respect to materials and conversion, so each unit brings all its costs.

How do you find number of units?

Units digit of a number is the digit in the one's place of the number. i.e It is the rightmost digit of the number. For example, the units digit of 243 is 3, the units digit of 39 is 9.

How do you find number of units produced?

To compute the number of units manufactured, start with the number of units of work-in-process in beginning inventory (Beginning). Add the number of units of direct materials put into production (Inputs) and then subtract the number of units of work-in-process in ending inventory (Outputs).

How is the equivalent unit calculation affected when direct materials are added at the beginning?

If direct materials are added at the beginning of the process, the number of beginning WIP units would be multiplied by zero percent because all of the direct materials were consumed in the prior period.

How do you calculate equivalent units under weighted average FIFO?

4:568:35Cost Per Equivalent Unit-- FIFO Method vs. Weighted-average MethodYouTubeStart of suggested clipEnd of suggested clipBeginning working process for direct materials 8,000 for conversion costs. And then. We go withMoreBeginning working process for direct materials 8,000 for conversion costs. And then. We go with costs. Added during the period. So that's one hundred and seventy five thousand one hundred and sixty.

What is the FIFO method?

Key Takeaways. First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last.

What is FIFO expense?

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

What is the benefit of using FIFO?

1. Better valuation of inventory . By using FIFO, the balance sheet shows a better approximation of the market value of inventory. The latest costs for manufacturing or acquiring the inventory are reflected in inventory, and therefore, the balance sheet reflects the approximate current market value.

What is the term for the days required for a business to receive inventory, sell the inventory, and collect cash from

It considers the cost of goods sold, relative to its average inventory for a year or in any a set period of time. Operating Cycle. Operating Cycle An Operating Cycle (OC) refers to the days required for a business to receive inventory, sell the inventory, and collect cash from the sale.

Can you use LIFO in Canada?

Therefore, we can see that the balances for COGS and inventory depend on the inventory valuation method. For income tax purposes in Canada, companies are not permitted to use LIFO. However, US companies are able to use FIFO or LIFO.

Explanation

This article explains the computation of equivalent units of production under FIFO method. The concept of equivalent units has been explained in the previous article of this chapter – equivalent units of production – weighted average method.

Formula

The formula to compute equivalent units of production under FIFO method is given below:

What is equivalent unit in process costing?

Equivalent units under FIFO method of process costing are the number of finished units that could have been prepared in a process during a period had there been no unfinished units, either in opening WIP or closing WIP.

What is equivalent unit?

Equivalent units are relevant only for costs incurred during the period: which includes costs incurred on completing the opening WIP (i.e. the unfinished part), cost incurred on units started/added and transferred out and cost incurred on units in closing work in process.

Equivalent Units Formula

Equivalent units are calculated by multiply the number of physical units in work in process by the estimated percentage of completion of the units.

How to Calculate Equivalent?

As a simple example, suppose a business has 300 units of a product in work in process and they are estimated to be 40% complete. Using the equivalent units of production formula we get:

Estimating the Percentage of Completion

In the example above we simply stated that the estimated percentage of completion was 40%. In practice the percentage of completion needs to be based on each factor of production such as direct materials, direct labor, and manufacturing overheads.

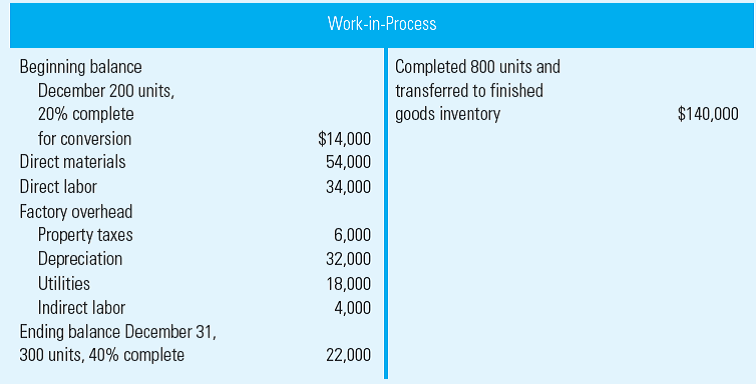

Equivalent Units FIFO Method Example

The following example is used to demonstrate how the equivalent units FIFO method is used to allocate production costs between completed and partially completed units.

Physical Units

The table below summarizes the movement of physical units during the accounting period.

Equivalent Units FIFO Method

The next step is to convert the physical units in production shown above (10,000) into equivalent units.

Allocating the Cost of Production

To allocate the cost of production to completed units and work in process we now simply multiply each equivalent unit by its respective cost per equivalent unit as follows:

Example of First-In, First-Out

- Company A reported beginning inventories of 100 units at $2/unit. Also, the company made purchases of: 1. 100 units @ $3/unit 2. 100 units @ $4/unit 3. 100 units @ $5/unit If the company sold 250 units, the order of cost expenses would be as follows: As illustrated above, the cost of goods sold (COGS)Cost of Goods Sold (COGS)Cost of Goods Sold (COG...

FIFO vs. LIFO

- To reiterate, FIFO expenses the oldest inventories first. In the following example, we will compare FIFO to LIFO (last in first out)Last-In First-Out (LIFO)The Last-in First-out (LIFO) method of inventory valuation is based on the practice of assets produced or acquired last being the first to be. LIFO expenses the most recent costs first. Consider the same example above. Recall that un…

Impact of FIFO Inventory valuation Method on Financial Statements

- Recall the comparison example of First-In First-Out and LIFO. The two methods yield different inventory and COGS. Now it is important to consider the impact of using FIFO on a company’s financial statements?

Key Takeaways from First-In First-Out

- FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold.

- It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system.

- It provides a poor matching of revenue with expenses.

Related Reading

- CFI is a global provider of financial analyst training and career advancement for finance professionals, including the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll t…