What is FIFO inventory management method and why use it?

The advantages to the FIFO method are as follows:

- The method is easy to understand, universally accepted and trusted.

- FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first). ...

- Less waste (a company truly following the FIFO method will always be moving out the oldest inventory first).

How to calculate cost of goods sold using FIFO method?

Inputs:

- First of all, you just have to enter the quantity of each unit purchases

- Then, you have to add the quantity of the price/unit you purchased

- Also, the lifo fifo method calculator provides you with options of adding more purchases “one by one” or multiple

- Then, you have to enter the total units sold from your number of purchases

What is the FIFO inventory method?

What is FIFO Inventory Valuation Method?

- First In First Out Inventory Method Examples. ABC Corporation uses the FIFO method of inventory valuation for the month of December. ...

- Reason for Using FIFO Method of Inventory Valuation. ...

- Advantages. ...

- Disadvantages. ...

- Video on FIFO Inventory Method

- Recommended Articles. ...

How to calculate 'available to sell' inventory?

Inventory Formula

- Methods For Calculating Ending Inventory. ...

- Examples of Inventory Formula (With Excel Template) Let’s take an example to understand the calculation of Inventory in a better manner. ...

- Explanation Of Inventory. ...

- Relevance and Uses of Inventory Formula. ...

- Inventory Formula Calculator

- Recommended Articles. ...

What is FIFO in accounting?

FIFO is the default method of determining inventory value. If you want to use LIFO, you must meet some specific requirements and file an application using IRS Form 970.

What is the difference between LIFO and FIFO?

Under FIFO, the cost of goods sold will be lower and the closing inventory will be higher. However, in times of falling prices, the opposite will hold. 2 . FIFO is the default method of determining inventory value.

What is FIFO in 2021?

Updated February 07, 2021. FIFO is one of several ways to calculate the cost of inventory in a business. The other common inventory calculation methods are LIFO (last-in, first-out) and average cost. FIFO, which stands for "first-in, first-out," is an inventory costing method that assumes that the first items placed in inventory are the first sold.

Why do we value inventory?

One reason for valuing inventory is to determine its value for inventory financing purposes . Another reason for valuing inventory is that inventory costs are included in the cost of goods sold, which reduces business income for tax purposes.

What is specific identification?

Instead of using FIFO, some businesses use one of these other inventory costing methods : Specific identification is used when specific items can be identified. For example, the cost of antiques or collectibles, fine jewelry, or furs can be determined individually, usually through appraisals.

Is inventory cost deductible on taxes?

Like other legitimate business costs, the cost of the products you buy to resell can be deducted from your business income to reduce your taxes.

How to calculate FIFO?

To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

What does FIFO mean?

FIFO is an acronym. It stands for “First-In, First-Out” and is used for cost flow assumption purposes. Cost flow assumptions refers to the method of moving the cost of a company’s product out of its inventory to its cost of goods sold.

What is LIFO in accounting?

LIFO stands for “Last-In, First-Out”. LIFO is the opposite of the FIFO method and it assumes that the most recent items added to a company’s inventory are sold first. The company will go by those inventory costs in the COGS (Cost of Goods Sold) calculation. The LIFO method for financial accounting may be used over FIFO when the cost ...

What is the difference between FIFO and LIFO?

The FIFO (“First-In, First-Out”) method means that the cost of a company’s oldest inventory is used in the COGS (Cost of Goods Sold) calculation. LIFO (“Last-In, First-Out”) means that the cost of a company’s most recent inventory is used instead. Here’s What We’ll Cover:

Why use LIFO or FIFO?

The LIFO method for financial accounting may be used over FIFO when the cost of inventory is increasing, perhaps due to inflation. Using FIFO means the cost of a sale will be higher because the more expensive items in inventory are being sold off first.

When calculating COGS, what is the company going to go by?

Therefore, when calculating COGS (Cost of Goods Sold), the company will go by those specific inventory costs. Although the oldest inventory may not always be the first sold, the FIFO method is not actually linked to the tracking of physical inventory, just inventory totals. However, FIFO makes this assumption in order for ...

What is FIFO valuation?

Under the FIFO method of accounting inventory valuation, the goods which are purchased at the earliest are the first one to be removed from the inventory account. This results in remaining inventory at books to be valued at the most recent price for which the last stock of inventory is purchased. This results in inventory assets recorded on the balance sheet at the most recent costs.

Why is FIFO accounting used?

FIFO method of accounting saves time, and money spends in calculating the exact inventory cost that is being sold because the recording of inventory is done in the same order as they are purchased or produced. Easy to understand.

What are the disadvantages of FIFO accounting?

One of the biggest disadvantages of FIFO accounting method is inventory valuation during inflation, First In First Out method will result in higher profits, and thus will results in higher “Tax Liabilities” in that particular period. This may result in increased tax charges and higher tax-related cash outflows.

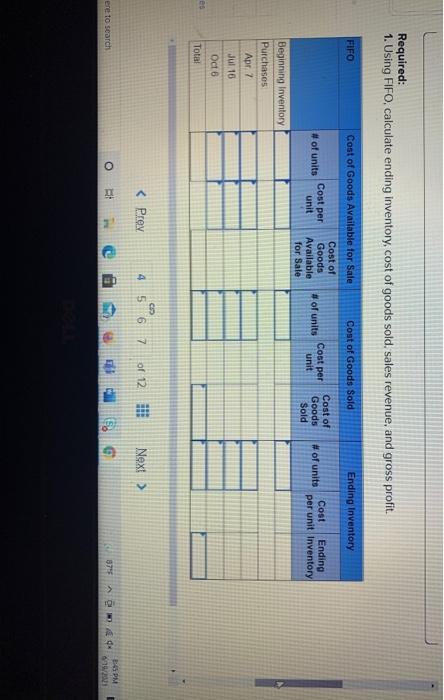

What method does ABC use for inventory valuation?

ABC Corporation uses the FIFO method of inventory valuation for the month of December. During that month, it records the following transactions:

What is the ending inventory formula?

Ending Inventory The ending inventory formula computes the total value of finished products remaining in stock at the end of an accounting period for sale. It is evaluated by deducting the cost of goods sold from the total of beginning inventory and purchases. read more

Which method of inventory valuation gives the most accurate calculation of the inventory and sales profit?

A business which is in the trading of perishable items generally sells the items which are purchased earliest first, FIFO method of inventory valuation generally gives the most accurate calculation of the inventory and sales profit. Other examples include retail businesses that sell foods or other products with an expiration date.

How are inventory costs reported?

Inventory costs are reported either on the balance sheet, or they are transferred to the income statement as an expense to match against sales revenue. When inventories are used up in production or are sold, their cost is transferred from the balance sheet to the income statement as cost of goods sold.

Why use LIFO method?

For some companies, there are benefits to using the LIFO method for inventory costing. For example, those companies that sell goods that frequently increase in price might use LIFO to achieve a reduction in taxes owed.

How to find average cost of goods sold?

This amount is then divided by the number of items the company purchased or produced during that same period . This gives the company an average cost per item. To determine the cost of goods sold, the company then multiplies the number of items sold during the period by the average cost per item.

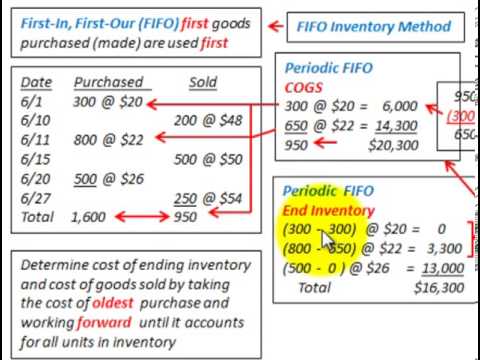

What is the first in first out method?

Companies frequently use the first in, first out (FIFO) method to determine the cost of goods sold or COGS. The FIFO method assumes the first products a company acquires are also the first products it sells. The company will report the oldest costs on its income statement, whereas its current inventory will reflect the most recent costs. FIFO is a good method for calculating COGS in a business with fluctuating inventory costs.

Why is the average cost method important?

The simplicity of the average cost method is one of its main benefits. It takes less time and labor to implement an average cost method , thereby reducing company costs. The method works best for companies that sell large numbers of relatively similar products.

Is FIFO a good method for calculating COGS?

FIFO is a good method for calculating COGS in a business with fluctuating inventory costs. While the LIFO inventory valuation method is accepted in the United States, it is considered controversial and prohibited by the International Financial Reporting Standards (IFRS).

Is FIFO cash flow assumption accurate?

While an actual sales pattern may not follow the FIFO cash flow assumption exactly, it is still an accurate method for determining COGS and allowed by both generally accepted accounting principles (GAAP) and International Financial Reporting Standards (IFRS).

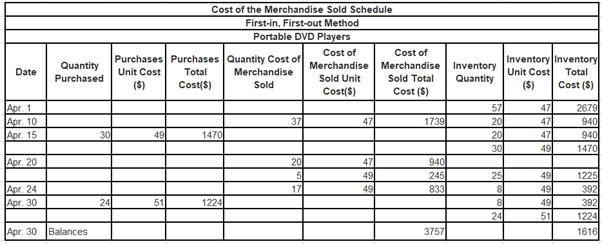

What is FIFO in inventory?

First-in, first-out (FIFO) method in periodic inventory system. Under first-in, first-out (FIFO) method, the costs are chronologically charged to cost of goods sold (COGS) i.e., the first costs incurred are first costs charged to cost of goods sold (COGS).

What is FIFO in accounting?

The company makes a physical count at the end of each accounting period to find the number of units in ending inventory. The company then applies first-in, first-out (FIFO) method to compute the cost of ending inventory.

How to calculate cost of goods sold?

Formula method: Under formula method, the cost of goods sold would be computed as follows: Cost of goods sold = Cost of units in beginning inventory + Cost of units purchased during the period – Cost of units in ending inventory.

What is the end of periodic inventory?

In a periodic inventory system when a sale is made, the entry to record the cost of goods sold is not made. At the end of accounting period, the quantity of inventory on hand (ending inventory) is found by a physical count and if the FIFO method is used to compute the cost of ending inventory, the cost of most recent purchases are used.

How to calculate number of units issued?

Number of units issued = Units in beginning inventory + Units purchased during the period – Units in ending inventory

What is FIFO in inventory management?

No doubt, good inventory management scenario is that the oldest items should be sold first, while the most recently purchased goods remain in inventory. First in first out (FIFO) method of ending inventory involves matching the oldest produced goods with revenues.

What is the FIFO calculator?

Fifo calculator uses the first in first out method to find inventory value/cost for the first sold goods

Why is LIFO more difficult to maintain than FIFO?

LIFO ending inventory approach is more difficult to maintain than the FIFO as it can result in older inventory that never being shipped or sold . Also, lifo results in more complex records and even accounting practices because the unsold inventory prices do not leave the accounting system.

Why is LIFO not used in IFRS?

The IFRS (International Financial Reporting Standards) prohibits LIFO inventory method because of the potential distortions it may have on a firm’s profitability and financial statements. For instance, LIFO valuation method can understate a firm’s earnings for the purposes of keeping taxable income low.

How to calculate cost of goods sold?

If you want to calculate Cost of Goods Sold (COGS) concerning the LIFO method, then you ought to find out the cost of your most recent inventory, and simply multiply it by the cost of inventory sold.

What is the difference between COGS and inventory cost?

Under fifo, the COGS (cost of goods sold) is depends upon the cost of material bought earliest in the period, while the inventory cost is depends upon the cost of material bought later in the year. Remember that the outcomes in inventory cost being closed to current replacement cost.

What is FIFO method?

FIFO method is used for cost flow assumption purposes, these assumptions are referred to as the method of moving the cost of a company’s product that is out of its inventory to its cost of goods sold.

What does FIFO stand for in a store?

First In First Out (FIFO) assumes that every time units are taken from store, they are issued from the oldest available lot first and next lot to be consumed only if needed.

When do entities purchase inventory?

Entities purchase inventory as and when they feel the need or based on a particular method for example Economic Order Quantity (EOQ). Often the the purchase price is different every time order is placed. Therefore, the price of each purchase lot is different from each other as you can see in the data at left

What is the FIFO method of ending inventory?

This method of calculating ending inventory is formed from the belief that companies sell their oldest items first to keep the newest items in stock. It's important to note that during inflationary periods, the FIFO method will result in a higher ending inventory amount.

What is the ending inventory value derived from the FIFO method?

The ending inventory value derived from the FIFO method shows the current cost of the product based on the most recent item purchased.

What is the ending inventory formula for invest media?

This means that the ending inventory for this period for Invest Media would be 2,250 x 10 = $22,500.

Why is ending inventory important?

This formula provides companies with important insight as to the total value of products still for sale at the end of an accounting period. Learning how much ending inventory is can help a company form better marketing and sales plans to sell more products in the future.

What is the last in first out method?

The last-in, first-out method is when a company determines its ending inventory by looking at the cost of the last item purchased. This method assumes that the price of the last product bought is also the cost of the first item sold and that the most recent items bought were the first sold. The LIFO method takes into account the most recent items bought first in terms of the cost of goods sold and allocates older items bought in the ending inventory.

What is ending inventory?

Ending inventory is a term used to describe the monetary value of a product still up for sale at the end of an accounting period. This number is required to determine the cost of goods sold (COGS) and the ending inventory balance. A company's ending inventory should be included on its balance sheet and is especially important when reporting ...

Does LIFO decrease inventory value?

You should note that during inflationary times, using the LIFO method can result in lower net income values and a decreased ending inventory value.