What are the disadvantages of the FIFO accounting method?

FIFO, Average Cost ... It is possible for some investors to use the average cost method of accounting, which averages the cost basis for all shares in the portfolio, and taxable gains are ...

How to use the FIFO method?

The advantages to the FIFO method are as follows:

- The method is easy to understand, universally accepted and trusted.

- FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first). ...

- Less waste (a company truly following the FIFO method will always be moving out the oldest inventory first).

What is the difference between FIFO vs. LIFO?

- First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method.

- Last-in, first-out (LIFO) assumes the last inventory added will be the first sold.

- Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

How to calculate sales revenue FIFO?

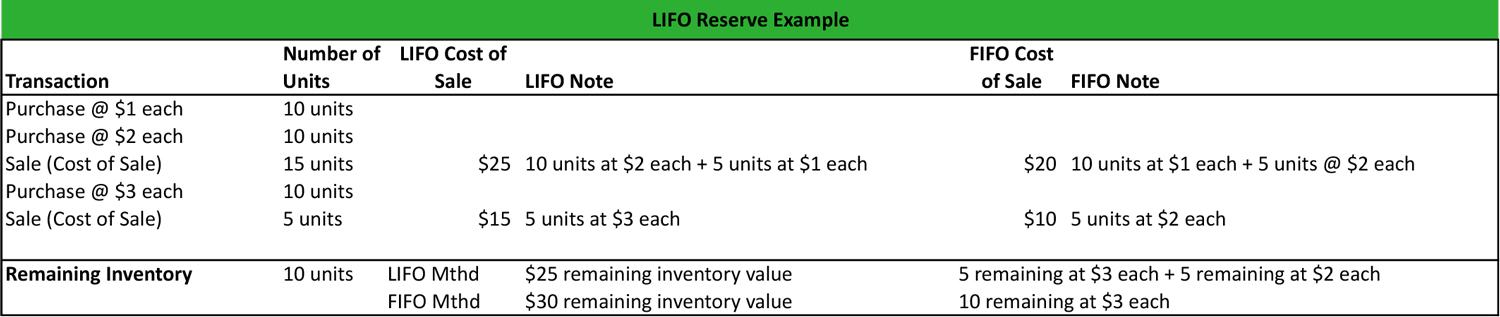

These are the simple steps that help to convert a LIFO-based statement to a FIFO-based statement:

- First, you have to add the LIFO reserve to LIFO inventory

- Then, you have to deduct the excess cash that saved from lower taxes under LIFO (i:e. ...

- Very next, you have to increase the retained earnings component of shareholders’ equity by the LIFO reserve x (1-T)

- Finally, in the income statement, FIFO COGS = LIFO COGS – Δ LIFO Reserve

What is FIFO explain with an example?

The FIFO method requires that what comes in first goes out first. For example, if a batch of 1,000 items gets manufactured in the first week of a month, and another batch of 1,000 in the second week, then the batch produced first gets sold first. The logic behind the FIFO method is to avoid obsolescence of inventory.

What is the FIFO method rule?

FIFO stands for first in, first out, an easy-to-understand inventory valuation method that assumes that goods purchased or produced first are sold first. In theory, this means the oldest inventory gets shipped out to customers before newer inventory.

How do you calculate return on FIFO?

8:1213:34Perpetual Inventory with Returns (FIFO, LIFO and Average Cost)YouTubeStart of suggested clipEnd of suggested clipAnd your cost of goods sold we look through the cost of goods sold column. We would add up the 240.MoreAnd your cost of goods sold we look through the cost of goods sold column. We would add up the 240. Plus the 150.

How do you calculate gross profit using FIFO?

For example, suppose a company's oldest inventory cost $200, the newest cost $400, and it has sold one unit for $1,000. Gross profit would be calculated as $800 under LIFO and $600 under FIFO.

How do you calculate cost of goods sold using the FIFO periodic inventory method?

1:554:57FIFO Periodic Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipSo then the next 20 units are gonna come out of this 30 from January 6 purchase. So that's 20 unitsMoreSo then the next 20 units are gonna come out of this 30 from January 6 purchase. So that's 20 units at $40 a unit. So we add those together and that gives us $1,500. As our cost of goods sold.

How do you calculate FIFO perpetual inventory?

4:346:22FIFO (Perpetual Inventory) - YouTubeYouTubeStart of suggested clipEnd of suggested clipWe need to sell an additional 10 on top of that 15. So that 10 comes from our inventory group at $8MoreWe need to sell an additional 10 on top of that 15. So that 10 comes from our inventory group at $8 apiece so under cost of goods sold. We have 15 units at $6. And then 10 units at $8.

What is LIFO and FIFO with example?

First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method. Last-in, first-out (LIFO) assumes the last inventory added will be the first sold. Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

How do you treat sales return in FIFO?

They are taken out of stock at the price at which they were purchased. Sales returns are shown as a negative in the OUT column as they represent a reduction in sales. The cost price of the goods returned is recorded at the most recent purchase price included in the sale transaction that they related to.

What is the FIFO method of food storage?

FIFO is “first in first out” and simply means you need to label your food with the dates you store them, and put the older foods in front or on top so that you use them first. This system allows you to find your food quicker and use them more efficiently.

Why is FIFO the best method?

FIFO is more likely to give accurate results. This is because calculating profit from stock is more straightforward, meaning your financial statements are easy to update, as well as saving both time and money. It also means that old stock does not get re-counted or left for so long it becomes unusable.

What is FIFO and LIFO example?

Ending Inventory per LIFO: 1,000 units x $8 = $8,000. Remember that the last units in (the newest ones) are sold first; therefore, we leave the oldest units for ending inventory. Ending Inventory per FIFO: 1,000 units x $15 each = $15,000.

What does FIFO product rotation mean?

FIFO stands for First-In First-Out. It is a stock rotation system used for food storage. You put items with the soonest best before or use-by dates at the front and place items with the furthest dates at the back.

What is FIFO expense?

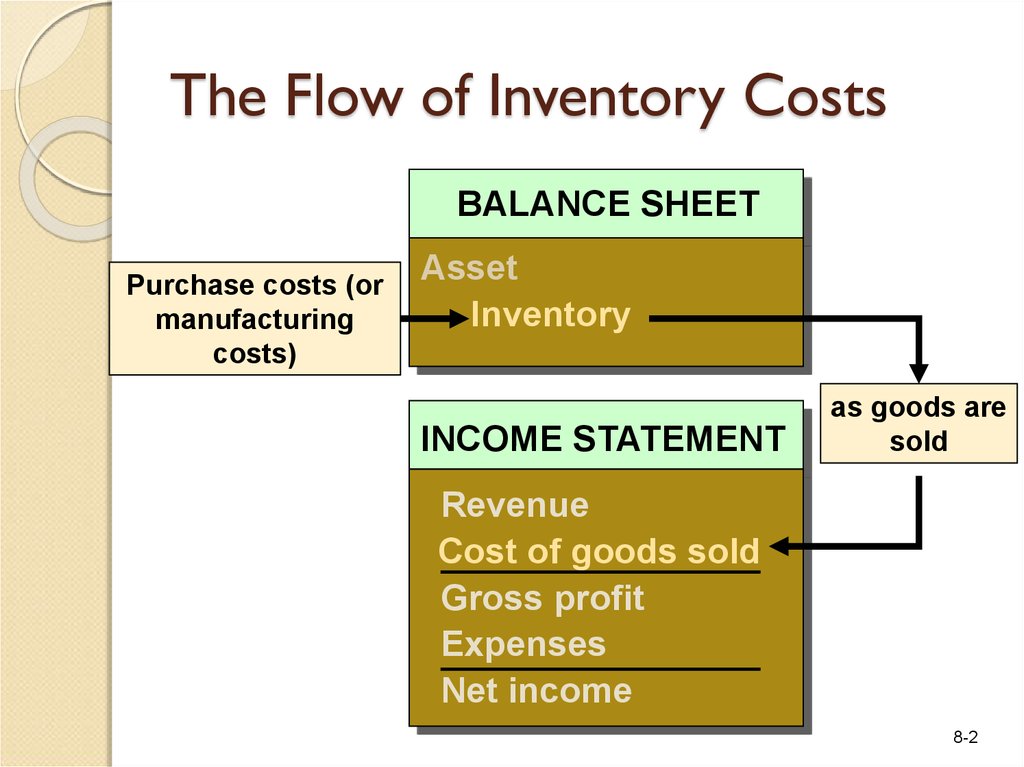

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

What is the benefit of using FIFO?

1. Better valuation of inventory . By using FIFO, the balance sheet shows a better approximation of the market value of inventory. The latest costs for manufacturing or acquiring the inventory are reflected in inventory, and therefore, the balance sheet reflects the approximate current market value.

What is the term for the days required for a business to receive inventory, sell the inventory, and collect cash from

It considers the cost of goods sold, relative to its average inventory for a year or in any a set period of time. Operating Cycle. Operating Cycle An Operating Cycle (OC) refers to the days required for a business to receive inventory, sell the inventory, and collect cash from the sale.

Can you use LIFO in Canada?

Therefore, we can see that the balances for COGS and inventory depend on the inventory valuation method. For income tax purposes in Canada, companies are not permitted to use LIFO. However, US companies are able to use FIFO or LIFO.

What does FIFO mean in accounting?

FIFO stands for “First-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company’s inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation.

Why do investors value FIFO?

Investors and banking institutions value FIFO because it is a transparent method of calculating cost of goods sold. It is also easier for management when it comes to bookkeeping, because of its simplicity.

Why is FIFO preferred?

The advantages to the FIFO method are as follows: The method is easy to understand, universally accepted and trusted. FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first).

Why is the LIFO method understated?

The value of remaining inventory, assuming it is not-perishable, is also understated with the LIFO method because the business is going by the older costs to acquire or manufacture that product. That older inventory may, in fact, stay on the books forever. Investors and banking institutions value FIFO because it is a transparent method ...

What is inventory sold?

The “inventory sold” refers to the cost of purchased goods (with the intention of reselling), or the cost of produced goods (which includes labor, material & manufacturing overhead costs). Keep in mind that the prices paid by a company for its inventory often fluctuate. These fluctuating costs must be taken into account.

Is FIFO overstating profit?

A company also needs to be careful with the FIFO method in that it is not overstating profit. This can happen when product costs rise and those later numbers are used in the cost of goods calculation, instead of the actual costs.

Is the FIFO method legal?

Both are legal although the LIFO method is often frowned upon because bookkeeping is far more complex and the method is easy to manipulate.

Why use LIFO method?

For some companies, there are benefits to using the LIFO method for inventory costing. For example, those companies that sell goods that frequently increase in price might use LIFO to achieve a reduction in taxes owed.

What is the last in first out method?

Last in, first out (LIFO) is another inventory costing method a company can use to value the cost of goods sold. This method is the opposite of FIFO. Instead of selling its oldest inventory first, companies that use the LIFO method sell its newest inventory first. Under this scenario, the last item in is the first item out.

Is FIFO a good method for calculating COGS?

FIFO is a good method for calculating COGS in a business with fluctuating inventory costs. While the LIFO inventory valuation method is accepted in the United States, it is considered controversial and prohibited by the International Financial Reporting Standards (IFRS).

Is FIFO cash flow assumption accurate?

While an actual sales pattern may not follow the FIFO cash flow assumption exactly, it is still an accurate method for determining COGS and allowed by both generally accepted accounting principles (GAAP) and International Financial Reporting Standards (IFRS).

What is FIFO accounting?

In accounting, First In, First Out (FIFO) is the assumption that a business issues its inventory to its customers in the order in which it has been acquired. Under the FIFO Method, inventory acquired by the earliest purchase made by the business is assumed to be issued first to its customers.

How does a perpetual inventory system work?

Perpetual. The example above shows how a perpetual inventory system works when applying the FIFO method. Perpetual inventory systems are also known as continuous inventory systems because they sequentially track every movement of inventory. On the other hand, Periodic inventory systems are used to reverse engineer the value of ending inventory.

Example-LIFO periodic system in a manufacturing company

While the business may not be literally selling the newest or oldest inventory, it uses this assumption for cost accounting purposes. If the cost of buying inventory were the same every year, it would make no difference whether a business used the LIFO or the FIFO methods. But costs do change because, for many products, the price rises every year.

Free Financial Statements Cheat Sheet

Although the oldest inventory may not always be the first sold, the FIFO method is not actually linked to the tracking of physical inventory, just inventory totals. However, FIFO makes this assumption in order for the COGS calculation to work.

Last-in, first-out (LIFO) method in a periodic inventory system

The company will go by those inventory costs in the COGS (Cost of Goods Sold) calculation. This article explains the use of first-in, first-out (FIFO) method in a periodic inventory system. If you want to read about its use in aperpetual inventory system, read “first-in, first-out (FIFO) method in perpetual inventory system” article.

A2. Periodic LIFO

Then, for internal purposes – such as in the case of investor reporting – the same company can use the FIFO method of inventory accounting, which reports lower costs and higher margins.

What does FIFO mean in inflation?

In a normal inflationary environment, this means that the cost of goods sold will be relatively low in comparison to current costs, which will increase the amount of taxable income; also, the inventory value reported on the balance sheet will approximately match current costs. The FIFO concept also applies to the actual usage of inventory.

Why is FIFO important?

When inventory items have a relatively short life span, it can be of considerable importance to structure the warehousing storage system so that the oldest items are presented to pickers first. Doing so reduces the risk of inventory spoilage.

What is FIFO 2021?

FIFO is an acronym for first in, first out. It is a cost layering concept under which the first goods purchased are assumed to be the first goods sold. The concept is used to devise the valuation of ending inventory, which in turn is used to calculate the cost of goods sold.

How much should ABC inventory be in March?

Based on the FIFO concept, the first ten units that ABC purchased should be charged to the cost of goods sold, on the theory that the first units into inventory should be the first ones removed from it. Thus, the cost of goods sold in March should be $50, while the value of the inventory at the end of March should be $70.