Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

What is the difference between FIFO vs. LIFO?

- First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method.

- Last-in, first-out (LIFO) assumes the last inventory added will be the first sold.

- Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

Which companies use LIFO method?

To complete the election application, you will need to:

- Specify the goods to which the LIFO method will apply,

- Identify and describe the inventory method (s) you used in the prior year to value these goods, and

- Explain what goods the LIFO method will NOT be used for.

How do you calculate gross profit in LIFO?

What are the benefits of good stock rotation?

- Increases productivity and efficiency.

- Creates a more organised warehouse.

- Helps save time and money.

- Improves accuracy of inventory orders.

- Keeps customers coming back for more.

What is LIFO and FIFO with example?

First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method. Last-in, first-out (LIFO) assumes the last inventory added will be the first sold. Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

How do you calculate FIFO and LIFO reserve?

LIFO Reserve ExampleCOGS (FIFO) = COGS (LIFO) – changes in LIFO Reserve.COGS (FIFO) = 60,000 – (45,000-42,000) = 60,000 – 3,000 = $57,000.

How do you calculate cost of goods using FIFO?

With this method, companies add up the total cost of goods purchased or produced during a specified time. This amount is then divided by the number of items the company purchased or produced during that same period. This gives the company an average cost per item.

How is LIFO balance calculated?

2:356:53How to Calculate LIFO Inventory (Step By Step) - YouTubeYouTubeStart of suggested clipEnd of suggested clipSo in a period of rising prices what's gonna happen is your cost of goods sold. Under LIFO will beMoreSo in a period of rising prices what's gonna happen is your cost of goods sold. Under LIFO will be higher. Now think about it your most recent purchases you took the last purchases. Usually are more

What is LIFO reserve formula?

Calculating LIFO Reserve When preparing company financials for the LIFO method, the difference in costs in inventory between LIFO and FIFO is the LIFO reserve. Therefore, a company's LIFO reserve = (FIFO inventory) - (LIFO inventory).

How do you calculate LIFO COGS and FIFO COGS?

So LIFO reserve must be added to LIFO inventory to get the FIFO inventory. But FIFO COGS is lower, so a change in reserve must be subtracted from LIFO COGS to get FIFO COGS = LIFO COGS – (ending LIFO reserve – beginning LIFO reserve). For FIFO, if COGS is lower, then net income and retained earnings must be higher.

What is FIFO method with example?

Example of FIFO Imagine if a company purchased 100 items for $10 each, then later purchased 100 more items for $15 each. Then, the company sold 60 items. Under the FIFO method, the cost of goods sold for each of the 60 items is $10/unit because the first goods purchased are the first goods sold.

What is LIFO example?

Example of LIFO that buys coffee mugs from wholesalers and sells them on the internet. One Cup's cost of goods sold (COGS) differs when it uses LIFO versus when it uses FIFO. In the first scenario, the price of wholesale mugs is rising from 2016 to 2019.

How do you calculate cost of goods sold using LIFO?

To calculate COGS using LIFO:Keep a record of each acquisition price per the amount bought.Define how many items you are going to sell. Our LIFO method calculator would bring a result here.Take the last items and their respective prices. Select only the ones you sold.Multiply their prices by their amount.

How do you calculate gross profit using FIFO?

For example, suppose a company's oldest inventory cost $200, the newest cost $400, and it has sold one unit for $1,000. Gross profit would be calculated as $800 under LIFO and $600 under FIFO.

How do you calculate inventory value?

Inventory values can be calculated by multiplying the number of items on hand with the unit price of the items.

What is LIFO method?

Key Takeaways Last in, first out (LIFO) is a method used to account for inventory. Under LIFO, the costs of the most recent products purchased (or produced) are the first to be expensed. LIFO is used only in the United States and governed by the generally accepted accounting principles (GAAP).

1. Can I switch my accounting method?

According to the IRS, you can switch from one accounting method to another on a yearly basis. Switching back and forth between approaches, on the o...

2. What accounting method should I use for my crypto?

The Generally Accepted Accounting Principles (GAAP) in the United States allows tax calculation agencies and software to choose between LIFO and FI...

3. How does the crypto market scenario affect LIFO accounting?

When calculating gains using LIFO, in a bull market (the crypto market is heading up and the cost basis is lower than the fair market value), you’l...

4. How does the crypto market scenario affect FIFO accounting?

When the crypto market is heading up (bull market) and the cost basis is lower than the fair market value, FIFO accounting methods can often lead t...

Which is better, LIFO or FIFO?

Many times, the LIFO calculation is considered a better accounting method than FIFO because of inflation, when the cost of assets is on a rise.

What does LIFO mean?

LIFO is short for Last-In-First-Out. Using this method, the coins that you acquired last, will be the first ones that you sell.

Does ZenLedger calculate crypto taxes?

ZenLedger easily calculates your crypto taxes and also finds opportunities for you to save money and trade smarter. Get started for free now or learn more about our tax professional prepared plans!

Is LIFO the same as FIFO?

In the absence of inflation, both LIFO and FIFO give the same outcomes. However, if inflation is substantial, the accounting system you choose might have a significant impact on your taxes. FIFO is considered the most traditional method of accounting, but LIFO can help you save a lot on your taxes.

Why is it dangerous to jump back and forth between LIFO and FIFO?

It is extremely dangerous for companies to jump back and forth between LIFO and FIFO because it will anger investors and pique the interest of the IRS. Most companies choose one method and stick with it.

What does FIFO mean in accounting?

The acronyms LIFO (last in, first out) and FIFO (first in, first out) are inventory management terms that help companies to keep track of inventory costs and profit generated. Most companies calculate both and use each number based on the company’s accepted accounting practices. Inventory that is “first in, first out” means ...

Which method of valuation results in more income?

The FIFO method generally results in more income for the company because it utilizes older inventory which is generally less costly. The LIFO method results in less income because it tends to use newer and more expensive inventory. Average Cost. The average cost of inventory is another valuation method that would fall somewhere between LIFO ...

What is the FIFO calculator?

Fifo calculator uses the first in first out method to find inventory value/cost for the first sold goods

Which is better, FIFO or LIFO?

If the opposite it’s true, and the ending inventory costs are going down, then FIFO costing approach might be better. Since inventory prices usually increase, most businesses are highly prefer to use LIFO costing

Why is LIFO more difficult to maintain than FIFO?

LIFO ending inventory approach is more difficult to maintain than the FIFO as it can result in older inventory that never being shipped or sold . Also, lifo results in more complex records and even accounting practices because the unsold inventory prices do not leave the accounting system.

Why is LIFO not used in IFRS?

The IFRS (International Financial Reporting Standards) prohibits LIFO inventory method because of the potential distortions it may have on a firm’s profitability and financial statements. For instance, LIFO valuation method can understate a firm’s earnings for the purposes of keeping taxable income low.

How to calculate cost of goods sold?

If you want to calculate Cost of Goods Sold (COGS) concerning the LIFO method, then you ought to find out the cost of your most recent inventory, and simply multiply it by the cost of inventory sold.

What is FIFO method?

FIFO method is used for cost flow assumption purposes, these assumptions are referred to as the method of moving the cost of a company’s product that is out of its inventory to its cost of goods sold.

What is FIFO in inventory management?

No doubt, good inventory management scenario is that the oldest items should be sold first, while the most recently purchased goods remain in inventory. First in first out (FIFO) method of ending inventory involves matching the oldest produced goods with revenues.

What is Fifo Lifo finder?

Fifo Lifo finder uses the average cost method in order to find the COG sold and inventory value.

What does FIFO mean in accounting?

What do the accountancy terms FIFO and LIFO mean? The methods FIFO (First In First Out) and LIFO (Last In First Out) define methods used to gather inventory units and determine the Cost of Goods Sold (COGS).

What does FIFO mean in inventory?

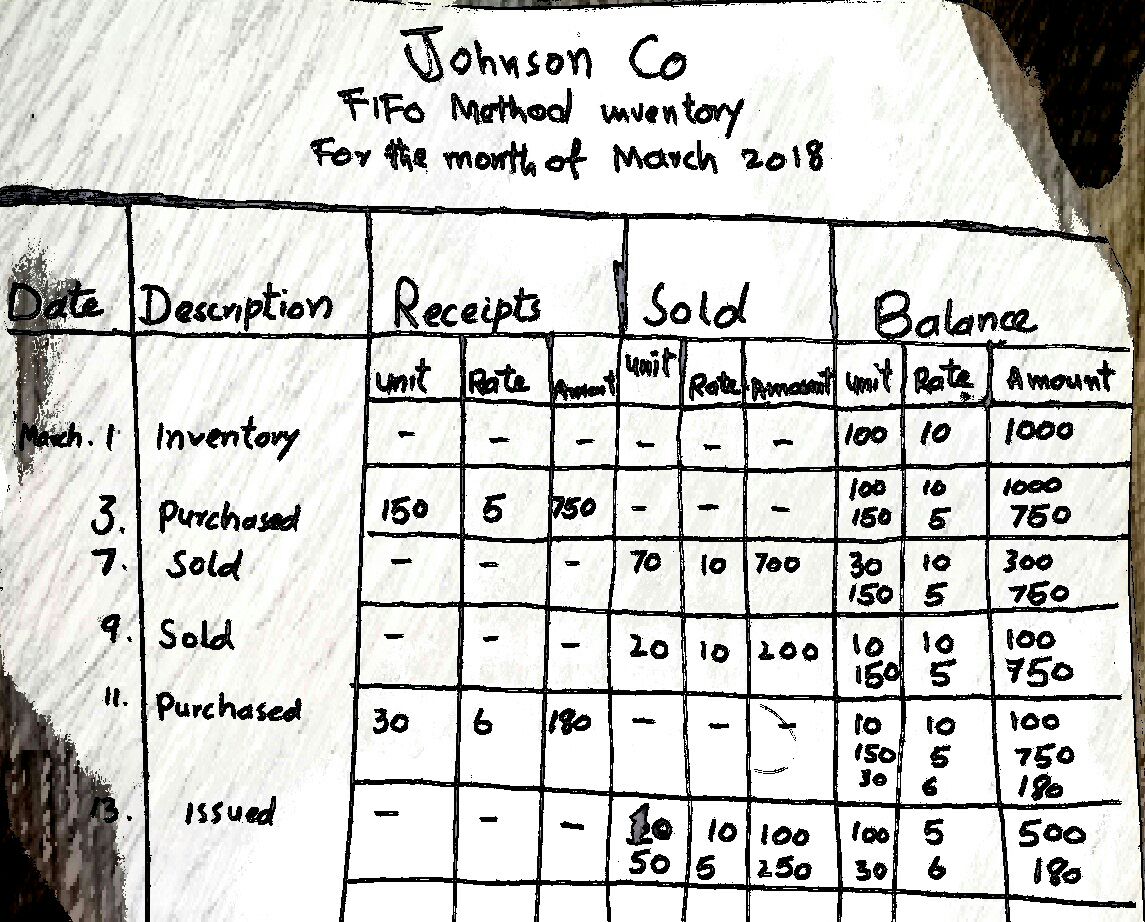

FIFO (First in First Out) means that the inventory which has been received first will be sold first. In other words, an ascending order will be followed. In the above example, the cost of 250 units had to be determined. Thus, the first hundred units received in January and the remaining 150 from Feb were used.

How to calculate ending inventory?

And to calculate the ending inventory, the new purchases are added to it, minus the exact cost of goods sold.

Why is FIFO easier to understand?

As such, FIFO is just following that natural flow of inventory, meaning less chance of mistakes when it comes to bookkeeping.

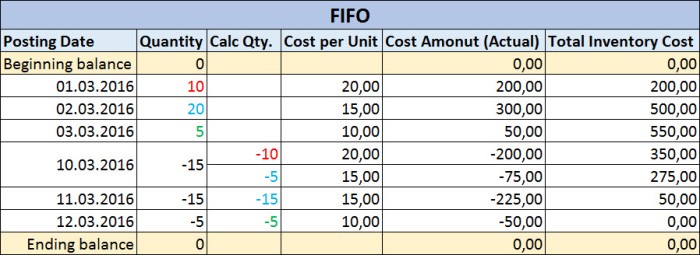

What is LIFO reserve?

The LIFO reserve is the amount by which a company’s taxable income has been deferred, as compared to the FIFO method. The remaining unsold 350 televisions will be accounted for in “inventory”.

How to calculate COGS?

To calculate COGS (Cost of Goods Sold) using the LIFO method, determine the cost of your most recent inventory. Multiply that cost by the amount of inventory sold.

What is FIFO in accounting?

FIFO and LIFO are methods used in the cost of goods sold calculation. FIFO (“First-In, First-Out”) assumes that the oldest products in a company’s inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company’s inventory have been sold first ...

What is the problem with a company switching to the LIFO method?

The problem with a company switching to the LIFO method is that the older inventory may stay on the books forever, and that older inventory (if not perishable or obsolete) will not reflect current market values. It will be understated.

Why are FIFO profits more accurate?

Although this may mean less tax for a company to pay under LIFO, it also means stated profits with FIFO are much more accurate because older inventory reflects the actual costs of that inventory. If profits are naturally high under FIFO, then the company becomes that much more attractive to investors.

Is FIFO a LIFO?

FIFO and LIFO are assumptions only. The methods are not actually linked to the tracking of physical inventory, just inventory totals. This does mean a company using the FIFO method could be offloading more recently acquired inventory first, or vice-versa with LIFO. However, in order for the cost of goods sold (COGS) calculation to work, both methods have to assume inventory is being sold in their intended orders.

Why is LIFO not accurate?

As a result, LIFO doesn't provide an accurate or up-to-date value of inventory because the valuation is much lower than inventory items at today's prices.

Why is LIFO not realistic?

LIFO is not realistic for many companies because they would not leave their older inventory sitting idle in stock.

Why is FIFO better than COGS?

FIFO can be a better indicator of the value for ending inventory because the older items have been used up while the most recently acquired items reflect current market prices. For most companies, FIFO is the most logical choice since they typically use their oldest inventory first in the production of their goods, which means the valuation of COGS reflects their production schedule.

What is the first in first out method?

The First-In, First-Out (FIFO) method assumes that the oldest unit of inventory is the sold first. LIFO is not realistic for many companies because they would not leave their older inventory sitting idle in stock. FIFO is the most logical choice since companies typically use their oldest inventory first in the production of their goods.

What accounting method is used to determine inventory costs?

The accounting method that a company uses to determine its inventory costs can have a direct impact on its key financial statements (financials)—balance sheet, income statement, and statement of cash flows. The U.S. generally accepted accounting principles (GAAP) allow businesses to use one of several inventory accounting methods: first-in, ...

When sales are recorded using the FIFO method, what is the oldest inventory?

When sales are recorded using the FIFO method, the oldest inventory–that was acquired first–is used up first. FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet.

How much is ending inventory in LIFO?

Ending Inventory per LIFO: 1,000 units x $8 = $8,000. Remember that the last units in (the newest ones) are sold first; therefore, we leave the oldest units for ending inventory.

Why use LIFO method?

For some companies, there are benefits to using the LIFO method for inventory costing. For example, those companies that sell goods that frequently increase in price might use LIFO to achieve a reduction in taxes owed.

How to find average cost of goods sold?

This amount is then divided by the number of items the company purchased or produced during that same period . This gives the company an average cost per item. To determine the cost of goods sold, the company then multiplies the number of items sold during the period by the average cost per item.

What is the first in first out method?

Companies frequently use the first in, first out (FIFO) method to determine the cost of goods sold or COGS. The FIFO method assumes the first products a company acquires are also the first products it sells. The company will report the oldest costs on its income statement, whereas its current inventory will reflect the most recent costs. FIFO is a good method for calculating COGS in a business with fluctuating inventory costs.

Is FIFO a good method for calculating COGS?

FIFO is a good method for calculating COGS in a business with fluctuating inventory costs. While the LIFO inventory valuation method is accepted in the United States, it is considered controversial and prohibited by the International Financial Reporting Standards (IFRS).

Is FIFO cash flow assumption accurate?

While an actual sales pattern may not follow the FIFO cash flow assumption exactly, it is still an accurate method for determining COGS and allowed by both generally accepted accounting principles (GAAP) and International Financial Reporting Standards (IFRS).