What is the formula for the cost of goods sold?

What is the COGs Formula

- On January 1st, your business has $100,000 of inventory on the shelf

- Throughout January, you’re business purchases and receives $25,000 of inventory, while simultaneously selling through some of your inventory on the shelf to fulfill customer orders

- On January 31st, you have a total inventory balance of $95,000. How much inventory did you use? ...

What items make up the cost of goods sold?

What’s included in cost of goods sold?

- The parts or machines required to create the product.

- All supplies required in the production of the product.

- Shipping parts and equipment to the warehouse to create the product, including containers, freight, fuel surcharges, etc.

- The workforce (people) who put the products together, ship the parts, etc.

How do you calculate sales with cost of goods sold?

What Is the Cost of Goods Sold Formula?

- Method One. At the beginning of the year, the beginning inventory is the value of inventory, which is actually the end of the previous year.

- Method Two. The cost of goods made or bought is adjusted according to change in inventory. ...

- Uses of COGS in Other Formulas. ...

- Handling Inventory Cost Changes. ...

How to account for cost of goods sold?

Use the retail inventory method to estimate ending inventory.

- Calculate the ratio of cost to retail using the formula (cost / retail price).

- For example, suppose you sold vacuum cleaners for $250 each, and the cost is $175. ...

- Calculate the cost of goods available for sale with the formula (cost of beginning inventory + cost of purchases).

What is the formula for calculating cost of goods sold?

At a basic level, the cost of goods sold formula is: Starting inventory + purchases − ending inventory = cost of goods sold.

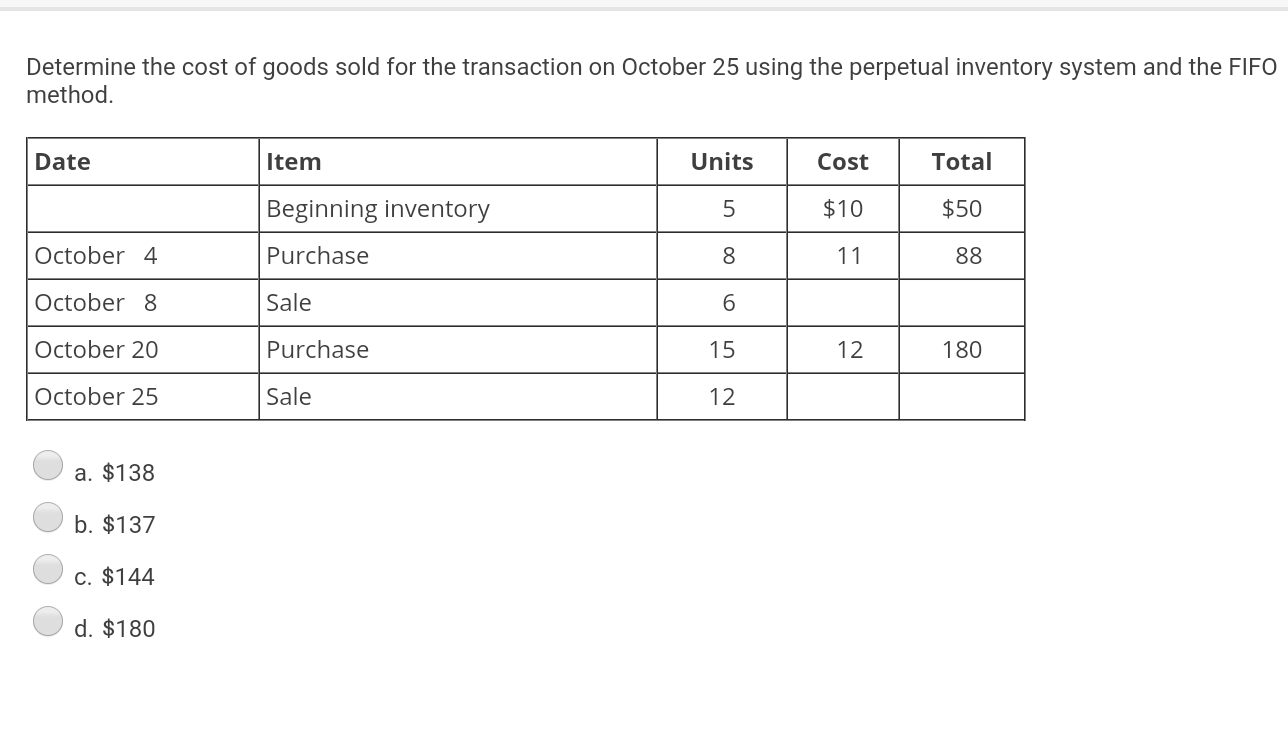

How does FIFO affect cost of goods sold?

(a) First-in, First-out (FIFO): Under FIFO, the cost of goods sold is based upon the cost of material bought earliest in the period, while the cost of inventory is based upon the cost of material bought later in the year. This results in inventory being valued close to current replacement cost.

What is FIFO method with example?

Example of FIFO Imagine if a company purchased 100 items for $10 each, then later purchased 100 more items for $15 each. Then, the company sold 60 items. Under the FIFO method, the cost of goods sold for each of the 60 items is $10/unit because the first goods purchased are the first goods sold.

What is the FIFO formula?

FIFO stands for “First-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company's inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation.

Why is COGS lower in FIFO?

More on FIFO Since FIFO (first-in, first out) is moving the older/lower costs to the cost of goods sold, the recent/higher costs are in inventory. The lower cost of goods sold generally results in larger amounts of gross profit, net income, taxable income, income tax payments, and certain financial ratios.

What does FIFO mean in accounting?

FIFO is an acronym. It stands for “First-In, First-Out” and is used for cost flow assumption purposes. Cost flow assumptions refers to the method of moving the cost of a company’s product out of its inventory to its cost of goods sold. Inventory refers to:

What is the difference between FIFO and LIFO?

The FIFO (“First-In, First-Out”) method means that the cost of a company’s oldest inventory is used in the COGS (Cost of Goods Sold) calculation. LIFO (“Last-In, First-Out”) means that the cost of a company’s most recent inventory is used instead. Here’s What We’ll Cover:

Why use LIFO or FIFO?

The LIFO method for financial accounting may be used over FIFO when the cost of inventory is increasing, perhaps due to inflation. Using FIFO means the cost of a sale will be higher because the more expensive items in inventory are being sold off first.

When calculating COGS, what is the company going to go by?

Therefore, when calculating COGS (Cost of Goods Sold), the company will go by those specific inventory costs. Although the oldest inventory may not always be the first sold, the FIFO method is not actually linked to the tracking of physical inventory, just inventory totals. However, FIFO makes this assumption in order for ...

What is FIFO in inventory?

FIFO is also adaptable to both types of inventory cycles: perpetual (inventory taken year-round constantly) or periodic (inventory taken certain times of the year)

What is FIFO in grocery?

The FIFO inventory method is popular with grocery stores and other stores that sell perishables, but it has plenty of applications for other retailers as well. As a retailer, you probably aren’t ordering every bit of your inventory at the same time for a number of reasons. The available inventory from vendors consistently changes.

What is FIFO in COGS?

FIFO means you would calculate your COGS as $15 + $25 = $40 as your COGs expense. Your remaining bookend set, the one priced at $10, is the cost of the most recent merchandise.

Why do you use FIFO?

Using FIFO helps you mitigate your inflation losses because, as the cost of goods rises, you’re able to adjust your prices of the previous stock and sell it at a higher cost as inflation dictates.

Is inventory considered an asset?

Calculating your inventory lets you keep an eye on your business’ performance and its overall assets. Unsold inventory is considered an asset, and when it’s sitting there, you need to know exactly how it affects your bottom line as well as how it relates to taxes.

Can you stock inventory all at once?

You don’t have the room for a huge stock of inventory all at once. Inventory is seasonal, and you won’t stock it when out of season. With all of these variables affecting inventory, it’s probable that inventory will flow consistently into your store rather than arriving as one huge order.

Does Erply POS use FIFO?

If you haven’t learned FIFO inventory calculation yet as a way of calculating your inventory, it’s time to start. Erply POS uses FIFO and features its practices built into the system to offer you a no-hassle way of calculating your inventory valuation.

What is the difference between LIFO and FIFO?

Under FIFO, the cost of goods sold will be lower and the closing inventory will be higher. However, in times of falling prices, the opposite will hold. 2 . FIFO is the default method of determining inventory value.

What is FIFO in 2021?

Updated February 07, 2021. FIFO is one of several ways to calculate the cost of inventory in a business. The other common inventory calculation methods are LIFO (last-in, first-out) and average cost. FIFO, which stands for "first-in, first-out," is an inventory costing method that assumes that the first items placed in inventory are the first sold.

Is inventory cost deductible on taxes?

Like other legitimate business costs, the cost of the products you buy to resell can be deducted from your business income to reduce your taxes.

Why is cost of goods sold important?

The cost of goods sold (COGS) is an incredibly important metric for your business. Not only is it important for taxes— it is a deductible expense after all —it is an important part of understanding the overall health of your business. Properly calculating your cost of goods sold allows you to determine a “true cost.”.

What is the inventory costing method?

The inventory costing method your company chooses will directly affect the value of the cost of goods sold during each accounting period. There are three inventory costing methods: First In, First Out (FIFO). As the title implies, the first products acquired during the accounting period will be sold.

What is the beginning inventory?

Your beginning inventory is the inventory value at the beginning of the accounting period or the value of the inventory left over from the previous accounting period. Cost of goods. The cost of goods is the cost of any product bought or made throughout the accounting period.

How much is Hallsen's Q2 inventory?

Hallsen, Inc. has a quarterly accounting period. Their Q2 beginning inventory had a value of $7000. The goods purchased over Q2 are valued at $4000, and the ending inventory is valued at $3000.

What is included in the cost of revenue?

In addition to production costs, the cost of revenue also includes costs such as marketing, shipping and distribution, commissions, and discounts applied. Like the cost of goods sold, the cost of revenue does not include any indirect costs.

What is direct cost?

Direct costs will be directly tied to a “cost object,” the product or service, and includes costs related to the production or acquisition of that “cost product.”. These costs can be fixed or variable—they can fluctuate. Generally speaking, direct costs include the direct labor expenses and the direct material costs.

Is COGS a business expense?

COGS is a deductible business expense. The IRS has a detailed explanation of how to calculate your cost of goods sold properly. You must follow the set rules and regulations when calculating and filing. Otherwise, you run the risk of an audit later.

What is FIFO expense?

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

What is the benefit of using FIFO?

1. Better valuation of inventory . By using FIFO, the balance sheet shows a better approximation of the market value of inventory. The latest costs for manufacturing or acquiring the inventory are reflected in inventory, and therefore, the balance sheet reflects the approximate current market value.

What is the valuation of goods?

valuation is based on the assumption that the sale or usage of goods follows the same order in which they are bought. In other words, under the first-in, first-out method, the earliest purchased or produced goods are sold/removed and expensed first. Therefore, the most recent costs remain on the balance sheet, while the oldest costs are expensed ...

What is the term for the days required for a business to receive inventory, sell the inventory, and collect cash from

It considers the cost of goods sold, relative to its average inventory for a year or in any a set period of time. Operating Cycle. Operating Cycle An Operating Cycle (OC) refers to the days required for a business to receive inventory, sell the inventory, and collect cash from the sale.

Can you use LIFO in Canada?

Therefore, we can see that the balances for COGS and inventory depend on the inventory valuation method. For income tax purposes in Canada, companies are not permitted to use LIFO. However, US companies are able to use FIFO or LIFO.

Fifo and Lifo

What do the accountancy terms FIFO and LIFO mean? The methods FIFO (First In First Out) and LIFO (Last In First Out) define methods used to gather inventory units and determine the Cost of Goods Sold (COGS).

How to calculate FIFO and LIFO?

Consider that there is a watch manufacturing company that gets its units for the last 6 months as follows.

Fifo vs Lifo

If you have a look at the cost of COGS in LIFO, it is more than COGS in FIFO because the order in which the units have been consumed is not the same. In this example as well, we needed to determine the COGS of 250 units.

Ending Inventory

It is the actual amount of products that are available for sale at the end of an auditing period.

References

Business News Daily. (2020, August 28). FIFO vs LIFO: What Is the Difference?