Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

Why does Amazon use FIFO?

Summary

- Amazon recently hit an all-time high after rumors of the potential launch of its own shopping channel.

- Valuation analysis can provide useful information, but for some companies, it's better to use one method over another.

- In the case of Amazon, 'price to cash flow' is a better valuation metric than price/earnings.

What does FIFO stand for?

First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last.

What is the difference between FIFO vs. LIFO?

- First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method.

- Last-in, first-out (LIFO) assumes the last inventory added will be the first sold.

- Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

How is the FIFO method applied?

First In, First Out (FIFO) is part of an accounting method where assets which are acquired first are sold of first. The method FIFO considers the inventory as consisting of items bought in the end. The method of FIFO is contrary to another method LIFO in which goods purchased at last are sold first.

What is FIFO and when is it used?

FIFO stands for first in, first out, an easy-to-understand inventory valuation method that assumes that goods purchased or produced first are sold first. In theory, this means the oldest inventory gets shipped out to customers before newer inventory.

How do you record inventory using FIFO?

The FIFO method records the first items purchased as the items that were sold, and the last items purchased are the ones listed as inventory on hand.Record the amount of inventory on hand at the beginning of the period. ... Record the amount and dates of inventory purchased, as well as the price of each shipment.More items...

How do you calculate cost of goods sold using FIFO?

The First-in First-out (FIFO) method of inventory valuation is based on the assumption that the sale or usage of goods follows the same order in which they are bought....For the sale of 250 units:100 units at $2/unit = $200 in COGS.100 units at $3/unit = $300 in COGS.50 units at $4/unit = $200 in COGS.

When FIFO method is most suitable?

LIFO is a newer inventory cost valuation technique (accepted in the 1930s), which assumes that the newest inventory is sold first. LIFO gives a higher cost to inventory....Last-In, First-Out (LIFO)FIFO vs. LIFO - A ComparisonFIFOLIFOAssumes first items in inventory sold firstAssumes last items in inventory sold first5 more rows•May 21, 2021

How should food workers store food using FIFO?

The FIFO procedure follows 5 simple steps:Locate products with the soonest best before or use-by dates.Remove items that are past these dates or are damaged.Place items with the soonest dates at the front.Stock new items behind the front stock; those with the latest dates should be at the back.More items...•

How does FIFO affect the balance sheet?

FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet. As a result, FIFO can increase net income because inventory that might be several years old–which was acquired for a lower cost–is used to value COGS.

How does FIFO affect ending inventory?

Under FIFO, your Cost of Goods Sold (COGS) will be calculated using the unit cost of the oldest inventory first. The value of your ending inventory will then be based on the most recent inventory you purchased.

How does FIFO affect cost of goods sold?

(a) First-in, First-out (FIFO): Under FIFO, the cost of goods sold is based upon the cost of material bought earliest in the period, while the cost of inventory is based upon the cost of material bought later in the year. This results in inventory being valued close to current replacement cost.

How do you calculate FIFO perpetual inventory?

6:567:50Inventory costing - FIFO, Perpetual - YouTubeYouTubeStart of suggested clipEnd of suggested clipSo we have six hundred units sitting in inventory. And their total cost would be three thousandMoreSo we have six hundred units sitting in inventory. And their total cost would be three thousand dollars and that's the amount that would show up on the balance sheet under our inventory.

When using the FIFO inventory costing method the most recent costs are assigned to?

When using the FIFO inventory costing method, the most recent costs are assigned to the cost of goods sold. If the perpetual inventory system is used, the account entitled Merchandise Inventory is debited for purchases of merchandise.

What is LIFO and FIFO with example?

First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method. Last-in, first-out (LIFO) assumes the last inventory added will be the first sold. Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

What is first in, first out (FIFO)?

FIFO is an accounting technique that calculates the cost of inventory based on which stock came in first. Goods that have not been sold are assumed...

What are the disadvantages of FIFO method?

The main disadvantage of using the FIFO method is that it does not take into account specific sales from inventory batches. This can make it diffic...

What are the 5 benefits of FIFO first in first out?

There are several benefits of using the FIFO first in first out accounting method. These benefits include: It is a universally accepted method of c...

Why is FIFO the best method?

FIFO is considered the best method of accounting for inventory because it is a universally accepted standard, it is seen as being generally fair, a...

How is FIFO implemented in stores?

In stores, FIFO is usually implemented by using the oldest receipts to calculate the cost of goods sold. This ensures that the most recent inventor...

What is FIFO method?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

What is FIFO in manufacturing?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense. Under FIFO, it is assumed that the cost of inventory purchased first will be recognized first. The dollar value of total inventory decreases in this process because inventory has been removed from the company’s ownership. The costs associated with the inventory may be calculated in several ways — one being the FIFO method.

What is the opposite of FIFO?

The opposite of FIFO is LIFO (Last In, First Out), where the last item purchased or acquired is the first item out. In inflationary economies, this results in deflated net income costs and lower ending balances in inventory when compared to FIFO.

What happens when FIFO assigns the oldest costs to the cost of goods sold?

In this situation, if FIFO assigns the oldest costs to the cost of goods sold, these oldest costs will theoretically be priced lower than the most recent inventory purchased at current inflated prices. This lower expense results in higher net income. Also, because the newest inventory was purchased at generally higher prices, the ending inventory balance is inflated.

What is FIFO accounting?

First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last. An alternative to FIFO, LIFO is an accounting method in which assets purchased or acquired last are disposed of first.

What are the advantages of first in first out?

What Are the Advantages of First In, First Out (FIFO)? The obvious advantage of FIFO is that it's most widely used method of valuing inventory globally. It is also the most accurate method of aligning the expected cost flow with the actual flow of goods which offers businesses a truer picture of inventory costs.

What is the benefit of using FIFO?

1. Better valuation of inventory . By using FIFO, the balance sheet shows a better approximation of the market value of inventory. The latest costs for manufacturing or acquiring the inventory are reflected in inventory, and therefore, the balance sheet reflects the approximate current market value.

What is FIFO expense?

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

Can you use LIFO in Canada?

Therefore, we can see that the balances for COGS and inventory depend on the inventory valuation method. For income tax purposes in Canada, companies are not permitted to use LIFO. However, US companies are able to use FIFO or LIFO.

Why is FIFO used?

FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual financial health. Here’s everything you need to know to decide if the FIFO method is right for you.

What is the FIFO method?

Short for first in, first out, the FIFO method is a popular strategy for fulfilling customer orders and assigning costs to your sold inventory for accounting purposes. The first in, first out (or FIFO) method is a strategy for assigning costs to goods sold. Essentially, it means your business sells the oldest items in your inventory first—at least ...

Why is the FIFO method better than the LIFO method?

Because of inflation, businesses using the FIFO method are often able to report higher profit margins than companies using the last in, first out (LIFO) method. That’s because the FIFO method matches older, lower-cost inventory items with higher current- cost revenue. Businesses on the LIFO system, on the other hand, see less of a margin between their current costs and their current revenue.

What is FIFO accounting?

That being said, FIFO is primarily an accounting method for assigning costs to your goods sold. So you don’t necessarily have to actually sell your oldest products first—you just account for the cost of goods sold using the oldest numbers. In other words, when determining your business’s cost of goods sold (COGS), ...

What is the first in first out method?

The first in, first out (or FIFO) method is a strategy for assigning costs to goods sold. Essentially, it means your business sells the oldest items in your inventory first—at least on paper, anyway. FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual ...

How many items were in the first sale of the FIFO?

The first sale (on October 9) consisted of 150 items—more than the first purchase order (or FIFO layer) included. So we applied the cost of the 100 items in the first FIFO layer to the first 100 items in the sales order. The cost of the remaining 50 items was taken from the next-oldest purchase order (FIFO layer 2).

Is FIFO better than LIFO?

FIFO is also more transparent and easier to use than LIFO. LIFO systems are easy to manipulate to make it look like your business is doing better than it is. But a FIFO system provides a more accurate reflection of the current value of your inventory. This is one of the reasons why the International Financial Reporting Standards (IFRS) Foundation requires businesses to use FIFO.

Why is FIFO accounting used?

FIFO method of accounting saves time, and money spends in calculating the exact inventory cost that is being sold because the recording of inventory is done in the same order as they are purchased or produced. Easy to understand.

What is FIFO valuation?

Under the FIFO method of accounting inventory valuation, the goods which are purchased at the earliest are the first one to be removed from the inventory account. This results in remaining inventory at books to be valued at the most recent price for which the last stock of inventory is purchased. This results in inventory assets recorded on the balance sheet at the most recent costs.

What are the disadvantages of FIFO accounting?

One of the biggest disadvantages of FIFO accounting method is inventory valuation during inflation, First In First Out method will result in higher profits, and thus will results in higher “Tax Liabilities” in that particular period. This may result in increased tax charges and higher tax-related cash outflows.

What is the ending inventory formula?

Ending Inventory The ending inventory formula computes the total value of finished products remaining in stock at the end of an accounting period for sale. It is evaluated by deducting the cost of goods sold from the total of beginning inventory and purchases. read more

Is FIFO valuation a good measure?

FIFO method of inventory valuation is not an appropriate measure if the goods/materials purchased have fluctuation in their price patterns as this may results in misstated profits for the same period.

Does inflation increase operating expenses?

Normally in an inflationary environment, prices are always rising, which will cause an increase in operating expenses, but with FIFO accounting, the same inflation will cause an increase in ending inventory.

Is the first in first out method a good measure of inventory?

Use of First In First Out method is not a suitable measure of inventory in times of “ hyperinflation .”. During such times, there is no particular pattern of inflation, which may result in prices of goods to inflate drastically.

What is a FIFO?

FIFOs are commonly used in electronic circuits for buffering and flow control between hardware and software. In its hardware form, a FIFO primarily consists of a set of read and write pointers, storage and control logic. Storage may be static random access memory (SRAM), flip-flops, latches or any other suitable form of storage.

What does FIFO mean in computing?

In computing and in systems theory, FIFO an acronym for first in, first out (the first in is the first out) is a method for organising the manipulation of a data structure (often, specifically a data buffer) where the oldest (first) entry, or "head" of the queue, is processed first.

What is FIFO in disk scheduling?

Disk controllers can use the FIFO as a disk scheduling algorithm to determine the order in which to service disk I/O requests, where it is also known by the same FCFS initialism as for CPU scheduling mentioned before.

What is a synchronous FIFO?

Synchronicity. A synchronous FIFO is a FIFO where the same clock is used for both reading and writing. An asynchronous FIFO uses different clocks for reading and writing and they can introduce metastability issues.

When was the first FIFO implemented?

The first known FIFO implemented in electronics was by Peter Alfke in 1969 at Fairchild Semiconductor. Alfke was later a director at Xilinx .

What are some examples of FIFO?

Examples of FIFO status flags include: full, empty, almost full, and almost empty. A FIFO is empty when the read address register reaches the write address register. A FIFO is full when the write address register reaches the read address register. Read and write addresses are initially both at the first memory location and the FIFO queue is empty.

What is a hardware FIFO?

A hardware FIFO is used for synchronization purposes. It is often implemented as a circular queue, and thus has two pointers :

Methods of calculating inventory cost

As inventory is usually purchased at different rates (or manufactured at different costs) over an accounting period, there is a need to determine what cost needs to be assigned to inventory.

First In First Out (FIFO)

This method assumes that inventory purchased first is sold first. Therefore, inventory cost under FIFO method will be the cost of latest purchases. Consider the following example:

Example

Bike LTD purchased 10 bikes during January and sold 6 bikes, details of which are as follows:

How to implement FIFO?

There are a few other considerations to make when implementing FIFO procedures. Things you can do to make the process easier include: 1 Label items efficiently: Using a clear labeling process like sequential pallet licensing can help you identify the oldest items in the warehouse so you know what to ship out first.#N#Make older items most accessible: When implementing FIFO procedures, it is important that the older items are the most accessible in the warehouse. Make considerations in the put-away process to store product to make material handling easy. 2 Stack the pallets appropriately: When organizing the warehouse, it is important that new pallets are not stacked on old pallets. Should older pallets be stored under new pallets, more material movement is required for FIFO procedures. Stacking pallets appropriately makes the fulfillment process easier.

Why use FIFO?

A FIFO system can be ideal in a number of warehousing situations. In fact, many warehouses rely on FIFO procedures for inventory management. Taking advantage of FIFO procedures can help you boost efficiency and throughput in your warehouse.

How does FIFO reduce inflation?

FIFO can reduce the impact of inflation on suppliers, retailers and ecommerce businesses. Because the old product is the first sold, it might have cost less to make than newer inventory. This keeps prices accurate and helps retailers and ecommerce businesses manage inventory and profits.

What is a FIFO warehouse?

The FIFO procedure for distribution is a solid strategy to choose if the products in your warehouse have a shelf life. Items like batteries, beauty products, fashion and apparel, nutraceuticals and supplements all need to move quickly. If you're warehousing products with an expiration date, FIFO warehousing procedures might be for you. When using a FIFO method, the oldest inventory moves first.

Why is FIFO important?

Inflation slowly makes things more expensive. Employing FIFO procedures can help minimize the impact of rising prices. Because the older inventory that cost less to make is shipped out first, ecommerce businesses and retailers can better manage their profits and inventory.

What does FIFO mean in warehouse management?

FIFO stands for First In, First Out. It is as simple as it sounds. When using this method of warehouse management, the oldest stock of inventory is shipped out first. The newest inventory stays until the oldest is shipped out to stores or directly to consumers.

How does FIFO improve quality?

Implementing an effective FIFO process can help improve quality control. In doing so, customer satisfaction can increase. Shipping out older stock efficiently can mean that customers receive consistent products. Customers are less likely to get obsolete products because stock is rotated adequately.

What is a fifo and a fifo?

While both FIFO and LIFO are a way to manage inventory, the marketable goods produced by a company usually dictate which method to choose. FIFO is typically used for perishable products like food and beverages or stock that may become obsolete if it isn't sold within a certain period of time. LIFO however is often used for products that aren't affected by the amount of time spent in inventory or where the flow of product fits the LIFO method.

What is FIFO in business?

The marketable goods produced by a company usually dictate which method to choose. FIFO is typically used for perishable products like food and beverages or stock that may become obsolete or expire if it isn't sold within a certain time. LIFO, however, is often used for products that aren't affected by time spent in inventory or where the flow of product fits the LIFO method.

Why use FIFO vs LIFO?

FIFO vs. LIFO for flow of goods. Many companies choose to use FIFO because it more closely mimics the actual flow of goods in and out of inventory. It's considered a simpler system with less spoilage and waste of materials.

How is FIFO inventory calculated?

FIFO inventory cost is calculated by determining the cost of the oldest stock and multiplying that amount by the number of items sold.

What is FIFO in inventory?

What is FIFO? First in, first out is a method to value inventory and calculate the cost of goods sold. FIFO items are the oldest products in an inventory because they were the first stock to be added after purchase or production. FIFO uses the principle that when items are acquired first, they are also sold first.

What is the outcome of FIFO?

In the FIFO outcome, the cost of inventory is lower, resulting in higher profits but more taxable income.

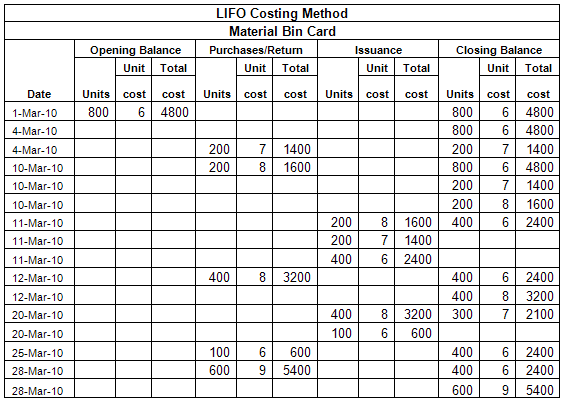

What is LIFO method?

Using the LIFO method, more recent stock can be valued higher than older goods when there is a price increase. LIFO works well using the matching principle, which is used to charge costs along with revenues during the same period of inventory calculations. Read more: A Guide To the Inflation Rate.

Example of First-In, First-Out

FIFO vs. LIFO

- To reiterate, FIFO expenses the oldest inventories first. In the following example, we will compare FIFO to LIFO (last in first out)Last-In First-Out (LIFO)The Last-in First-out (LIFO) method of inventory valuation is based on the practice of assets produced or acquired last being the first to be. LIFO expenses the most recent costs first. Consider the same example above. Recall that un…

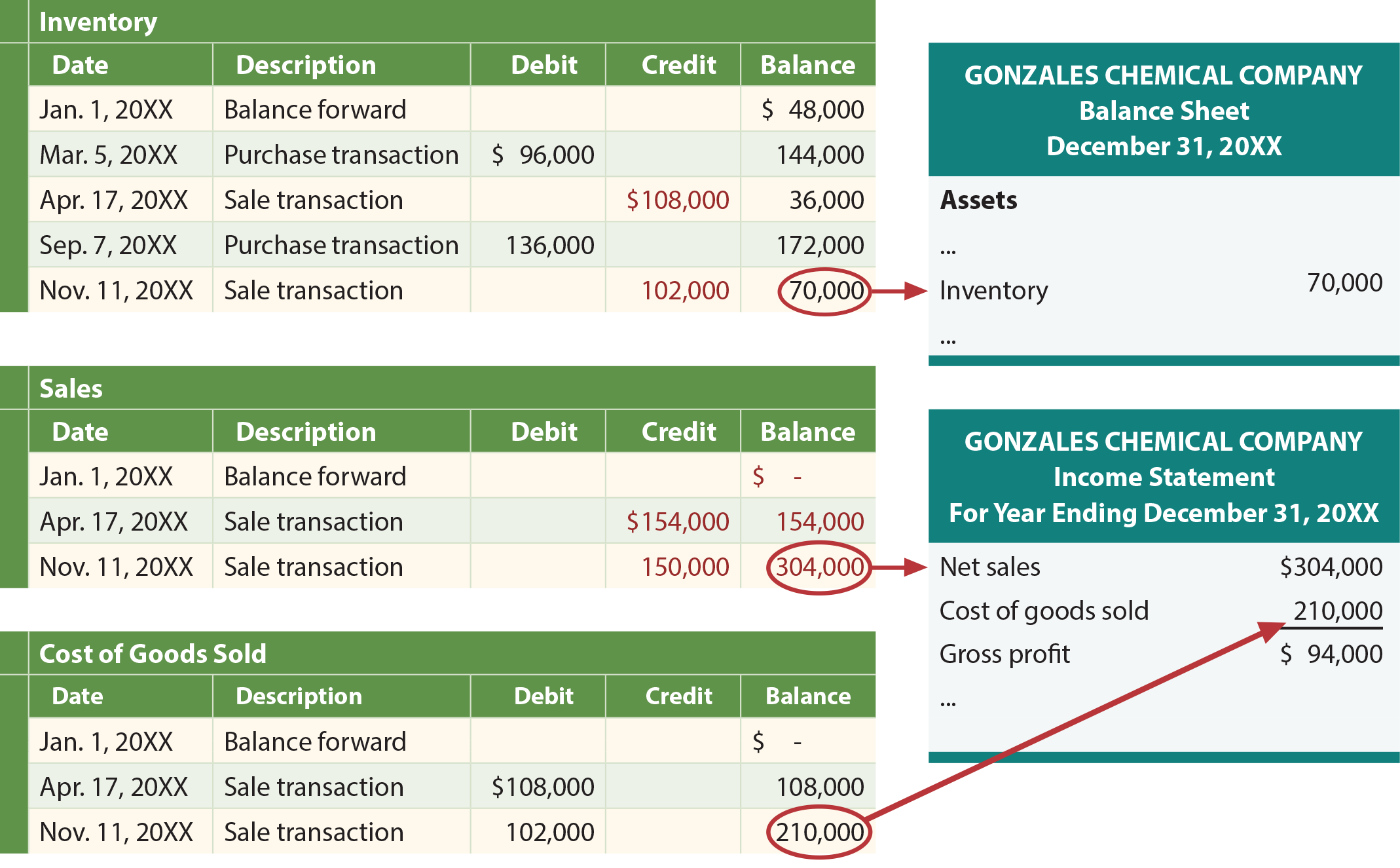

Impact of FIFO Inventory valuation Method on Financial Statements

- Recall the comparison example of First-In First-Out and LIFO. The two methods yield different inventory and COGS. Now it is important to consider the impact of using FIFO on a company’s financial statements?

Key Takeaways from First-In First-Out

- FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold.

- It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system.

- It provides a poor matching of revenue with expenses.

Related Reading

- CFI is a global provider of financial analyst training and career advancement for finance professionals, including the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll t…