The periodic inventory system is a software system that supports taking a periodic count of stock. Companies import stock numbers into the software, perform an initial physical review of goods and then import the data into the software to reconcile. Fifo With LIFO

FIFO and LIFO accounting

FIFO and LIFO accounting are methods used in managing inventory and financial matters involving the amount of money a company has tied up within inventory of produced goods, raw materials, parts, components, or feed stocks. They are used to manage assumptions of cost flows related to inventory, stock repurchases (if purchased at different prices), and various other accounting purposes.

Full Answer

How do you calculate periodic inventory?

Other features of periodic inventory software include:

- User-defined accounts set for different combinations of books and subsidiaries.

- Creation of journal entries in the background based on a scheduled script.

- Custom reports such as Journals Created Today, Journals Not Needed for Transactions Created Today, Error Reports and Modified Transactions.

How to calculate LIFO and FIFO?

These are the simple steps that help to convert a LIFO-based statement to a FIFO-based statement:

- First, you have to add the LIFO reserve to LIFO inventory

- Then, you have to deduct the excess cash that saved from lower taxes under LIFO (i:e. ...

- Very next, you have to increase the retained earnings component of shareholders’ equity by the LIFO reserve x (1-T)

- Finally, in the income statement, FIFO COGS = LIFO COGS – Δ LIFO Reserve

How to calculate LIFO perpetual?

LIFO perpetual inventory card (prepared above) can help compute cost of goods sold and ending inventory. a. Cost of goods sold (COGS): $560 + $336 + $168 + $436 = $1,500. b. Ending inventory:

240 + $84] = $324. When LIFO method is used in a perpetual inventory system, it is typically known as “LIFO perpetual system”.

What is LIFO method with example?

The advantages of LIFO method are as follows:

- LIFO method is easy to implement and understand.

- It provides tax benefits to the business organisations by reporting less profits and deferring Income Tax payment in the future years.

- LIFO method provides the benefit of matching the current cost with the current revenues thereby reducing the profits included in the inventory.

Is periodic inventory system FIFO?

In a periodic FIFO inventory system, companies apply FIFO by starting with a physical inventory. In this example, let's say the physical inventory counted 590 units of their product at the end of the period, or Jan. 31. Purchases over this period are in the following table.

How do you do LIFO periodic inventory?

Under a periodic LIFO system, you would wait until the end of the month and then record the sale, which means that you remove five units from the last layer recorded at the end of the month, which results in a charge to the cost of goods sold of $35 (5 units x $7 each).

How do you do FIFO periodic inventory?

2:024:57FIFO Periodic Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipBut we still have another 20 units because this is just 20 but we sold 40. So then the next 20 unitsMoreBut we still have another 20 units because this is just 20 but we sold 40. So then the next 20 units are gonna come out of this 30 from January 6 purchase. So that's 20 units at $40 a unit.

Is FIFO periodic or perpetual?

With perpetual FIFO, the first (or oldest) costs are the first removed from the Inventory account and debited to the Cost of Goods Sold account. Therefore, the perpetual FIFO cost flows and the periodic FIFO cost flows will result in the same cost of goods sold and the same cost of the ending inventory.

What is periodic inventory system?

A periodic inventory system measures the level of inventory and cost of goods sold through occasional physical counts. In contrast, the perpetual inventory system is a method that continuously monitors a business's inventory balance by automatically updating inventory records after each sale or purchase.

Is LIFO perpetual or periodic?

5:597:07LIFO Perpetual vs. Periodic - YouTubeYouTubeStart of suggested clipEnd of suggested clipSomething you don't even buy until December 12 months away if that's your accounting. Period if youMoreSomething you don't even buy until December 12 months away if that's your accounting. Period if you are using LIFO periodic.

What is FIFO periodic method?

What is the Periodic FIFO Method? Periodic FIFO is a cost flow tracking system that is used within a periodic inventory system. Under a periodic system, the ending inventory balance is only updated when there is a physical inventory count.

What are the most common inventory costing methods used under periodic system?

The four methods included are: specific identification, weighted average cost, first-in first-out (FIFO), and last-in first-out (LIFO).

What is LIFO used for?

LIFO periodic system is also extensively used by manufacturing companies for recording and costing materials. Consider the following example:

How many units were in inventory in 2016?

According to a physical count, 1,300 units were found in inventory on December 31, 2016. The company uses a periodic inventory system to account for sales and purchases of inventory. Required: Assuming a last-in, first-out (LIFO) cost flow assumption is used, compute: the cost of inventory on December 31, 2016.

How to calculate cost of units issued to factory?

Formula method: Under formula method, the cost of units issued to factory would be computed by deducting the cost of units in ending inventory from the total cost of units available for use during the month. The total cost of units available for use is equal to cost of units in beginning inventory plus cost of units purchased during the month.

What is the recent cost method?

Recent cost method: Under recent cost method, we would compute the total number of units sold during the year and then we would assign cost to these units using most recent costs incurred to purchase units. The computations are given below:

What is the last in first out method?

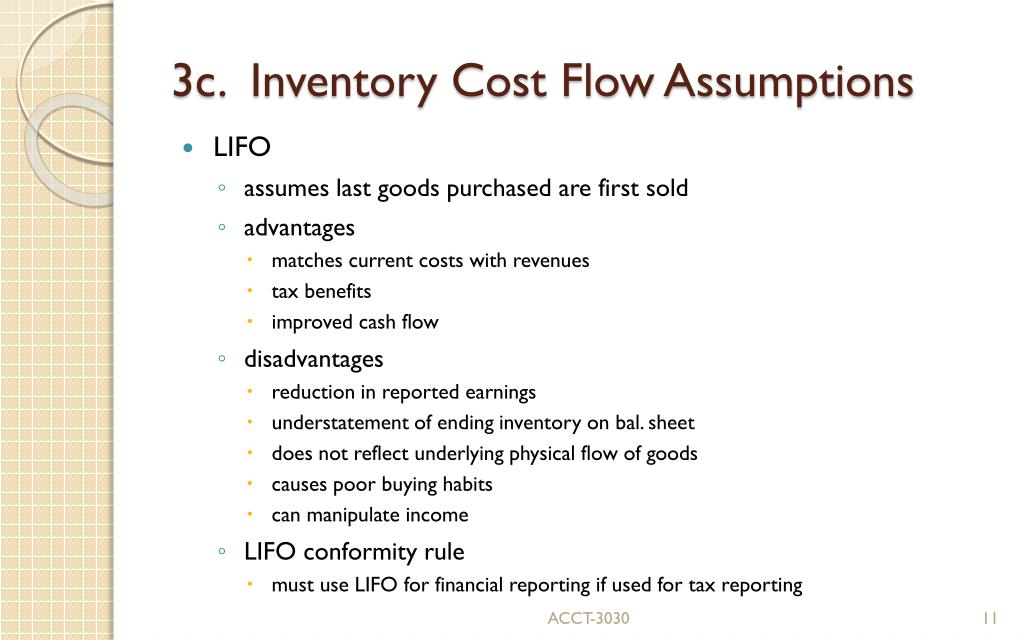

Under last-in, first-out (LIFO) method, the costs are charged against revenues in reverse chronological order i.e., the last costs incurred are first costs expensed . In other words, it assumes that the merchandise sold to customers or materials issued to factory has come from the most recent purchases. The ending inventory under LIFO would, therefore, consist of the oldest costs incurred to purchase merchandise or materials inventory.

How to calculate number of units sold in a year?

Number of units sold during the year = Units in beginning inventory + Units purchased during the year – Units in ending inventory

How many units of material were found in the store room in 2016?

On December 31, 2016, a physical count of inventory was made and 120 units of material were found in the store room. Required: Compute the total cost of inventory on December 31, 2016. Compute the total cost of units issued to factory during the month of December.

Definition & Example

The Periodic inventory system is also called a traditional inventory system. According to this system, the physical counting of inventory is made at the end of a certain period. This is the traditional costing system.

Example: In case of Increasing unit cost

The following information was found in the books of ABC Company for the month of January, 2019.

Under the weighted average cost (WAC) method

Weighted average cost (WAC) = Cost of goods available for sale / Units available for sale = 15,800 / 2,600 = Rs. 6.08

What is FIFO in inventory management?

FIFO (first in, first out) inventory management seeks to sell older products first so that the business is less likely to lose money when the products expire or become obsolete.

What is LIFO, and how does it work?

The last in, first out method of inventory entails using current prices to calculate the cost of goods sold, as opposed to using what was paid for the inventory already in stock. If the price of such goods has increased since the initial purchase, the cost of goods sold will be higher and thereby reduce profits and tax burdens. Nonperishable commodities – like petroleum, metals and chemicals – are frequently subject to LIFO accounting.

How are FIFO and LIFO similar?

However, they are similar in one regard: Both depend on the product remaining the same, with price being the only fluctuating element. FIFO and LIFO influence a company's earnings on paper.

Why is FIFO a good valuation method?

For businesses that need to impress investors, this becomes an ideal method of valuation, until the higher tax liability is considered. Because FIFO results in a lower recorded cost per unit, it also records a higher level of pretax earnings. And with higher profits, companies will likewise face higher taxes.

Why is LIFO important?

The principle of LIFO is highly dependent on how the price of goods fluctuates based on the economy. If a company holds inventory for a long time, holding on to products may prove quite advantageous in hedging profits for taxes. LIFO allows for higher after-tax earnings due to the higher cost of goods. At the same time, these companies risk that the cost of goods will go down in the event of an economic downturn and cause the opposite effect for all previously purchased inventory.

How to calculate cost of goods under FIFO?

To calculate the cost of goods under FIFO, begin by determining the cost of your oldest inventory, said Stephanie Ng, a CPA and founder of the CPA exam preparation website I Pass the CPA Exam. "Then, multiply this cost by the number of inventory items sold to determine the costs associated with the sale of inventory using FIFO," Ng said.

What would happen if the US ban LIFO?

If the United States were to ban LIFO, the country would clear an obstacle to adopting IFRS, thu s streamlining accounting for global corporations. Because of the current discrepancy, however, U.S.-based companies that use LIFO must convert their statements to FIFO in the footnotes of their financial statements.

What happens to the last units of inventory purchased in LIFO?

Under LIFO, if there is the last units of inventory purchased were bought at the highest price, then the units are sold first. Lower-priced older units remain in the inventory.

What does FIFO mean in warehouse?

FIFO (First-In, First-Out) As the name suggests, FIFO means the first entry comes out first. This method assumes that the first units to enter warehouse are sold first. So, the oldest items are sold first. This system is usually used by companies with perishable inventory.

What is LIFO in accounting?

LIFO or "last-in, first-out" is a method of accounting for inventory that assumes an inventory unit which is bought first will come out last. It also means that the first unit to be sold is the last inventory that comes into the warehouse. Under LIFO, if there is the last units of inventory purchased were bought at the highest price, ...

What is a LIFO?

LIFO and FIFO are the two most common inventory methods that are used by a company. The goal is to properly account for cost of purchased inventory on the balance sheet. Generally, a business can calculate its inventory either directly or through profits shown in the income statement and the cash flow statement.

What are the advantages of LIFO?

There are several advantages of LIFO for inventory accounting method: 1) Easy to compare current costs with current income, 2) If prices increase then the price of goods becomes conservative, 3) Operating profit is not affected by profit or loss from price fluctuations, 4) More tax savings.

Why is LIFO used?

LIFO is well used in inventory accounting to increase the cost of goods sold by a company. It is also used to reduce net profits, which can then reduce corporate tax liability. So, it is not surprising that LIFO is much more desirable when the corporate tax rate is higher.

How does inventory costing affect a company?

Applying different inventory costing methods affects the company's profits as well as the amount of taxes to be paid annually.

What is LIFO in accounting?

LIFO means last-in, first-out, and refers to the value that businesses assign to stock when the last items they put into inventory are the first ones sold. The products in the ending inventory are either leftover from the beginning inventory or those the company purchased earlier in the period. LIFO in periodic systems starts its calculations with a physical inventory. In this example, we also say that the physical inventory counted 590 units of their product at the end of the period, or Jan. 31. We use the same table (inventory card) for this example as in the periodic FIFO example.

Why do companies use periodic inventory?

The company uses a periodic inventory system to account for sales and purchases of stock. It helps the cost of goods sold calculation without taking periodic inventory count. Perpetual inventory system gives continuing information needed to keep maximum and minimum inventory levels by analyzing the appropriate timing of purchase. This ability of modern cloud-based inventory management softwares to get integrated with all the systems makes perpetual inventory system more practical.

What is cost flow assumption?

Cost flow assumptions are inventory costing methods in a periodic system that businesses use to calculate COGS and ending inventory. Beginning inventory and purchases are the input that accountants use to calculate the cost of goods available for sale. They then apply this figure to whichever cost flow assumption the business chooses to use, whether FIFO, LIFO or the weighted average. Most accounting software use a perpetual inventory system to track and update inventory purchases, sales and the cost of goods in real time.

What does it mean to combine two inventory methods?

By combining the two inventory methods, it means that the financial statements will be most accurate per the periodic method. The periodic inventory system does not update the general ledger account Inventory when a company purchases goods to be resold.

Why is periodic inventory different from perpetual inventory?

As a result, businesses can have inventory spread over more than one physical location while maintaining a centralized inventory management system. A periodic inventory system differs from the perpetual inventory method because there is no continuous record taken to determine the inventory value.

What is the difference between periodic and perpetual inventory?

The difference between the periodic and perpetual inventory systems. The periodic system relies upon an occasional physical count of the inventory to determine the ending inventory balance and the cost of goods sold, while the perpetual system keeps continual track of inventory balances.

How does the perpetual inventory system work?

Rather than staying dormant as it does with the periodic method, the Inventory account balance under the perpetual average is changing whenever a purchase or sale occurs. Under the perpetual system, there are continual updates to the cost of goods sold account as each sale is made. In the latter case, this means it can be difficult to obtain a precise cost of goods sold figure prior to the end of the accounting period.

Periodic Inventory Method

An additional expense includes training employees on how to operate them. Saving inventory and storage costs-since you’ll always be up-to-date with inventory count, you won’t have to stock more than required, assuming sales will be higher.

When You Should Use Periodic Inventory Method

Last in, first out is a valuation method that applies the most recent inventory costs to the cost of goods sold. It serves to make the costs on the income statement best approximate current costs. The inventory left over is valued at the oldest costs, which makes the balance sheet valuation lower than with other methods when prices are rising.

Netsuite Can Help Provide Visibility Into Your Inventory

It encompasses the money invested in producing goods, along with labor and material costs. As soon as the change is applied, the inventory on hand changes, which allows you to be well aware of your stock levels. Unlike the periodic inventory method, you can calculate the cost of goods sold frequently as the changes in the inventory.

Fifo

With LIFO costing, the accounting assumes that the newest inventory has been sold first. That means retained earnings the cost of goods sold and available for sale are based on the most recent valuation of a product.

Lifo In Periodic Inventory System

No additional training for employees –since a perpetual inventory software isn’t required, businesses with periodic inventory systems don’t need to focus on technical employee training. Hassle-free –periodic inventory system requires physical inventory counts after a specific interval of time.

What is the difference between LIFO and LIFO perpetual?

The reason is that under LIFO periodic system, the total of sales (or issues) is matched with the total of purchases (including beginning inventory, if any) at the end of the period whereas under LIFO perpetual system, each sale (or issue) is matched with the immediate preceding purchases.

Was there inventory in July?

There was no inventory in hand at the beginning of the month of July. Required: Compute the cost of goods sold during the month and inventory in hand at the end of the month under: LIFO periodic system. LIFO perpetual system.

Is LIFO periodic or perpetual?

The reason is that the LIFO periodic system does not take into account the exact dates involved but LIFO perpetual does.

What Is FIFO, and How Does It Work?

What Is LIFO, and How Does It Work?

- The last in, first out method of inventory entails using current prices to calculate the cost of goods sold, as opposed to using what was paid for the inventory already in stock. If the price of such goods has increased since the initial purchase, the cost of goods sold will be higher and thereby reduce profits and tax burdens. Nonperishable commodities – like petroleum, metals and chemi…

FIFO and LIFO Similarities and Differences

- FIFO and LIFO are quite different inventory management techniques. However, they are similar in one regard: Both depend on the product remaining the same, with price being the only fluctuating element. FIFO and LIFO influence a company’s earnings on paper. FIFO is most successful when used in an industry in which the price of a product remains stea...

Restrictions on The Use of LIFO

- LIFO is banned by International Financial Reporting Standards (IFRS), a set of common rules for accountants who work across international borders. While many nations have adopted IFRS, the United States still operates under the guidelines of generally accepted accounting principles (GAAP). If the United States were to ban LIFO, the country would clear an obstacle to adopting IF…