FIFO uses the principle that when items are acquired first, they are also sold first. The FIFO process is a straightforward way to track the flow of inventory, sales profits and the cost of producing and storing goods. Businesses use FIFO to simplify accounting on a balance sheet.

What is the FIFO method used for?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

How does FIFO affect the balance sheet?

By using FIFO, the balance sheet shows higher quality information about inventory. It does not affect the most recent purchases, thus providing high-quality information about the valuation of inventory.

What is an example of a FIFO charge?

These assigned costs are based on the order in which the product was used, and for FIFO, it is based on what arrived first. For example, if 100 items were purchased for $10 and 100 more items were purchased next for $15, FIFO would assign the cost of the first item resold of $10.

Which expense is expensed first in the FIFO system?

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

How do you solve using FIFO?

How Do You Calculate FIFO? To calculate COGS (Cost of Goods Sold) using the FIFO method, determine the cost of your oldest inventory. Multiply that cost by the amount of inventory sold.

How would you explain the FIFO principle?

FIFO is “first in first out” and simply means you need to label your food with the dates you store them, and put the older foods in front or on top so that you use them first. This system allows you to find your food quicker and use them more efficiently.

What are the 5 main reasons for using FIFO?

5 Benefits of FIFO Warehouse StorageIncreased Warehouse Space. Goods can be packed more compactly to free up extra floor space in the warehouse.Warehouse Operations are More Streamlined. ... Keeps Stock Handling to a Minimum. ... Enhanced Quality Control. ... Warranty Control.

What is FIFO advantages and disadvantages?

This method is useful for materials which are subject to obsolescence and deterioration In periods of rising prices, the FIFO method produces higher profits and results in higher tax liability because lower cost is charged to production Conversely in periods of falling, prices.

How is FIFO implemented in stores?

To implement the FIFO method, you must load the goods on one side and unload them on the other.Carton Flow picking system:High-density live storage system for boxes and light products. The product moves along rollers from the loading to the unloading area.

Is FIFO left to right?

The cone system works as follows: carts are positioned from left to right and the cone shows the ´oldest´ cart, which means it is the first cart to be taken out of the FIFO by the downstream station. When the oldest cart is taken out, the employee moves the cone one position to the right, the new ´oldest´ cart.

Why is FIFO the best method?

FIFO is more likely to give accurate results. This is because calculating profit from stock is more straightforward, meaning your financial statements are easy to update, as well as saving both time and money. It also means that old stock does not get re-counted or left for so long it becomes unusable.

What is advantage of FIFO method?

Advantages of FIFO method FIFO method saves money and time in calculating the exact cost of the inventory being sold because the cost will depend upon the most former cash flows of purchases to be used first. It is a simple concept which is easy to understand.

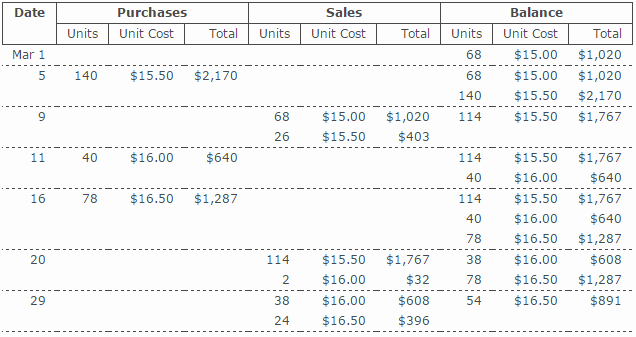

What is FIFO example?

First-In, First-Out (FIFO) is one of the methods commonly used to estimate the value of inventory on hand at the end of an accounting period and the cost of goods sold during the period....Example.Mar 1Beginning Inventory68 units @ $15.00 per unit20Sale116 units @ $19.50 per unit29Sale62 units @ $21.00 per unit4 more rows•Jun 9, 2019

When should you not use FIFO?

1: Batch Processing If you are moving or processing your parts in boxes or batches, then it will be difficult to maintain a FiFo within the box. It is possible using some creative numbering scheme, but unless there is a compelling reason to do so, the effort is not worth the benefit.

Why do companies switch from LIFO to FIFO?

For this and other reasons, CPAs may be called upon to advise companies switching from LIFO to FIFO (first in, first out) or average cost. A change from LIFO to FIFO typically would increase inventory and, for both tax and financial reporting purposes, income for the year or years the adjustment is made.

What are the limitations of FIFO?

The first-in, first-out (FIFO) accounting method has two key disadvantages. It tends to overstate gross margin, particularly during periods of high inflation, which creates misleading financial statements. Costs seem lower than they actually are, and gains seem higher than they actually are.

What is FIFO method?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

What is FIFO in manufacturing?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense. Under FIFO, it is assumed that the cost of inventory purchased first will be recognized first. The dollar value of total inventory decreases in this process because inventory has been removed from the company’s ownership. The costs associated with the inventory may be calculated in several ways — one being the FIFO method.

What is the opposite of FIFO?

The opposite of FIFO is LIFO (Last In, First Out), where the last item purchased or acquired is the first item out. In inflationary economies, this results in deflated net income costs and lower ending balances in inventory when compared to FIFO.

What is FIFO accounting?

First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last. An alternative to FIFO, LIFO is an accounting method in which assets purchased or acquired last are disposed of first.

What are the advantages of first in first out?

What Are the Advantages of First In, First Out (FIFO)? The obvious advantage of FIFO is that it's most widely used method of valuing inventory globally. It is also the most accurate method of aligning the expected cost flow with the actual flow of goods which offers businesses a truer picture of inventory costs.

What is the benefit of using FIFO?

1. Better valuation of inventory . By using FIFO, the balance sheet shows a better approximation of the market value of inventory. The latest costs for manufacturing or acquiring the inventory are reflected in inventory, and therefore, the balance sheet reflects the approximate current market value.

What is FIFO expense?

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

Can you use LIFO in Canada?

Therefore, we can see that the balances for COGS and inventory depend on the inventory valuation method. For income tax purposes in Canada, companies are not permitted to use LIFO. However, US companies are able to use FIFO or LIFO.