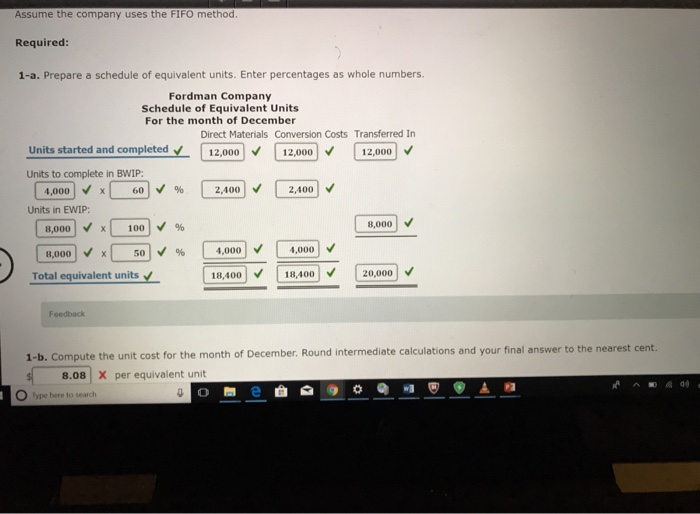

Equivalent units under FIFO method are calculated using the following formula: Equivalent units for each cost component = (100% − A) × B + C + D × E Where, A = percentage of completion at the end of last period B = units in opening work in process

...

Example.

| Direct Materials | Conversion Costs | |

|---|---|---|

| Equivalent units in beginning WIP [D=A×C] | 2,000 | 6,000 |

| Units started and completed in current period | 185,000 | 185,000 |

How do you calculate equivalent units?

What is Full Time Equivalent (FTE)?

- FTEs in the Workplace. Labor Force KPIs How can we monitor the labor force? ...

- Calculating FTEs. This is how a company, on average, calculates the average yearly number of hours that a full-time employee works.

- The Importance of Determining FTEs. ...

- Related Readings. ...

How do you calculate cost per equivalent unit?

Key Concepts and Summary

- costs added during the period

- costs of the units in ending inventory

- costs started and transferred during the period

- costs in the beginning inventory and costs added during the period

How do you calculate equivalent units of production?

Calculate Equivalent Units of Production. Here’s the formula: The number of partially completed units x percentage of completion = equivalent units of production. Plugging in the information that you have from the parts maker, there are 300 partially completed units. These 300 units are 50 percent completed.

What are the total equivalent units for conversion costs?

Total equivalent units (conversion costs) = 190,000 + 5,000 * 60% = 193,000 units As we can see, the direct materials are calculated at 100% because direct materials costs are incurred at the ...

How do you find equivalent units?

Equivalent units. are calculated by multiplying the number of physical (or actual) units on hand by the percentage of completion of the units. If the physical units are 100 percent complete, equivalent units will be the same as the physical units.

How do you calculate equivalent units under weighted average FIFO?

4:568:35Cost Per Equivalent Unit-- FIFO Method vs. Weighted-average MethodYouTubeStart of suggested clipEnd of suggested clipBeginning working process for direct materials 8,000 for conversion costs. And then. We go withMoreBeginning working process for direct materials 8,000 for conversion costs. And then. We go with costs. Added during the period. So that's one hundred and seventy five thousand one hundred and sixty.

How do you calculate EUP using FIFO?

FIFO Costing EUP Calculation for Conversion Costs As with direct materials, under FIFO costing, beginning WIP units for EUP are calculated by multiplying beginning WIP units by the percentage remaining to be completed at the beginning of the period with respect to conversion costs.

How do you find the equivalent cost per unit?

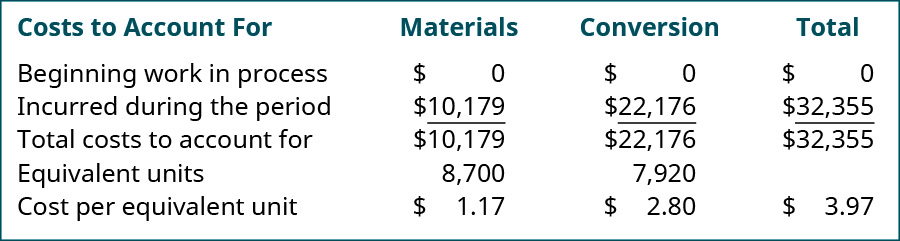

The cost per equivalent units for materials is the total of the material costs for the beginning work in process inventory plus the cost of material transferred in to the department plus the total of material costs incurred during the period.

How does the computation of equivalent units under the FIFO method differ from the computation of equivalent units under the weighted average method?

According to the Accounting for Management website, the main difference between the FIFO and weighted average method is in the treatment of beginning work-in-process or unfinished goods inventory. The weighted average method includes this inventory in computing process costs, while the FIFO method keeps it separate.

What is equivalent units production?

It is the number of completed units of an item that a company could theoretically have produced, given the amount of direct materials, direct labor, and manufacturing overhead costs incurred during that period for the items not yet completed.

What are equivalent units?

Equivalent units describe how much work has been done on a certain number of physical items. To simply calculate equivalent units, you can multiply the number of physical items by the percentage of the work done on them. For two items that are 50% done, you would have one equivalent unit (2 x 50% = 1).

How is the cost per equivalent unit calculated quizlet?

We calculate the cost per equivalent unit by adding together the cost of beginning Work in Process Inventory and the cost added during the period. We divide the total dollar amount by the number of equivalent units we previously calculated.

What is the FIFO cost method?

The FIFO cost method assumes that the cost that enters the department first will exit the department first, just like the name: first in will be first out. Equivalent units are the units that are currently in production, multiplied by the percentage of those units that are complete or those that are in progress.

What is equivalent unit?

The units that are currently in production multiplied by the percentage of those that are complete or those that are in process are called equivalent units. It accounts for all the costs related to a department's production. Equivalent units are used to prepare the production cost report.

What is equivalent unit?

Equivalent units are relevant only for costs incurred during the period: which includes costs incurred on completing the opening WIP (i.e. the unfinished part), cost incurred on units started/added and transferred out and cost incurred on units in closing work in process.

What is equivalent unit in process costing?

Equivalent units under FIFO method of process costing are the number of finished units that could have been prepared in a process during a period had there been no unfinished units, either in opening WIP or closing WIP.

Equivalent Units Formula

Equivalent units are calculated by multiply the number of physical units in work in process by the estimated percentage of completion of the units.

How to Calculate Equivalent?

As a simple example, suppose a business has 300 units of a product in work in process and they are estimated to be 40% complete. Using the equivalent units of production formula we get:

Estimating the Percentage of Completion

In the example above we simply stated that the estimated percentage of completion was 40%. In practice the percentage of completion needs to be based on each factor of production such as direct materials, direct labor, and manufacturing overheads.

Equivalent Units FIFO Method Example

The following example is used to demonstrate how the equivalent units FIFO method is used to allocate production costs between completed and partially completed units.

Physical Units

The table below summarizes the movement of physical units during the accounting period.

Equivalent Units FIFO Method

The next step is to convert the physical units in production shown above (10,000) into equivalent units.

Allocating the Cost of Production

To allocate the cost of production to completed units and work in process we now simply multiply each equivalent unit by its respective cost per equivalent unit as follows:

Equivalent Units Formula

How to Calculate equivalent?

- The formula to compute equivalent units of production under FIFO method is given below: Equivalent units under FIFO method = Percentage of work done on beginning inventory in current period + Units started and completed during current period + Percentage of work done on ending inventory in current period See the application of this formula in the f...

Estimating The Percentage of Completion

Equivalent Units FIFO Method Example

Physical Units

Equivalent Units FIFO Method

Allocating The Cost of Production