Facts According to the Accounting for Management website, the main difference between the FIFO

FIFO and LIFO accounting

FIFO and LIFO accounting are methods used in managing inventory and financial matters involving the amount of money a company has tied up within inventory of produced goods, raw materials, parts, components, or feed stocks. They are used to manage assumptions of cost flows related to inventory, stock repurchases (if purchased at different prices), and various other accounting purposes.

What are the benefits of using weighted averages?

What are the Benefits of Using Weighted Averages?

- Definition of Weighted Average. In order to determine a weighted average, you must assign a value to each of the numbers that you want to average, and then multiply the ...

- Smooth Out Fluctuations. ...

- Accounts for Uneven Data. ...

- Assumes Equal Values are Equal. ...

What is the weighted average market capitalization?

Weighted average market capitalization is a type of market index in which each component is weighted according to the size of its total market capitalization. Market capitalization is the sum of the total value of a company’s outstanding shares multiplied by the price of one share.

Which companies use process costing system?

is used by companies that produce similar or identical units of product in batches employing a consistent process. Examples of companies that use process costing include Chevron Corporation (petroleum products), the Wrigley Company (chewing gum), and Pittsburgh Paints (paint). A job costing system

What is weighted average accounting?

The weighted average method is used to assign the average cost of production to a product. Weighted average costing is commonly used in the following situations: Inventory items are so intermingled that it is impossible to assign a specific cost to an individual unit; The accounting system is not sufficiently sophisticated to track FIFO or LIFO inventory layers; or

What is the difference between FIFO LIFO and average cost accounting?

FIFO (“First-In, First-Out”) assumes that the oldest products in a company's inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company's inventory have been sold first and uses those costs instead.

What is the difference between weighted average cost and average cost?

The average is the sum of all individual observations divided by the number of observations. In contrast, the weighted average is observation multiplied by the weight and added to find a solution. An average is a mathematical equation, whereas the weighted average is applied in the daily activities of finance.

Why weighted average method is considered more appropriate to FIFO and LIFO method?

It's the easiest calculation and the most logical approach, so unless there is a strong reason for using LIFO or weighted average, FIFO is the default. If you sell high volumes of small items, like nails and screws for example, and the costs change regularly, weighted average may make more sense.

Which is more accurate FIFO or weighted average?

In a time of decreasing inflation, the profit margins for a company will be higher under weighted average method as compared to FIFO method because the cost of goods sold will be an average figure under weighted average method which will be lower if costs are recorded under FIFO method.

What is always same in FIFO and weighted average method?

The first-in first-out inventory valuation method assumes that the first items into inventory are the first items used in production. The weighted average cost is equal to the total cost of all inventory items divided by the number of units.

Which is better FIFO, LIFO or weighted average?

Generally speaking, FIFO is preferable in times of rising prices, so that the costs recorded are low, and income is higher. Contrarily, LIFO is preferable in economic climates when tax rates are high because the costs assigned will be higher and income will be lower.

What happens when you change from FIFO to weighted average?

If company changes its inventory valuation method from FIFO to weighted average method then it is basically changing the principle of valuation as FIFO follows a particular cost flow assumption whereas weighted average method uses weighted average of the cost at which inventory was held at the beginning of the period ...

Why is the weighted average method preferred?

One of the main reasons companies choose weighted average costing over other costing methods is because it radically simplifies cost calculations and record keeping.

What is the weighted average method?

When it comes time for businesses to account for their inventory, they typically use one of three different primary accounting methodologies: the weighted average method, the first in, first out (FIFO) method, or the last in, first out (LIFO) method. The weighted average method is most commonly employed when inventory items are so intertwined ...

What is FIFO accounting?

The first in, first out (FIFO) accounting method relies on a cost flow assumption that removes costs from the inventory account when an item in someone’s inventory has been purchased at varying costs, over time. When a business uses FIFO, the oldest cost of an item in an inventory will be removed first when one of those items is sold. This oldest cost will then be reported on the income statement as part of the cost of goods sold.

What is the last in first out accounting method?

With this accounting technique, the costs of the oldest products will be reported as inventory. It should be understood that, although LIFO matches the most recent costs with sales on the income statement, the flow of costs does not necessarily have to match the flow of the physical units.

When to use weighted average?

The weighted average method, which is mainly utilized to assign the average cost of production to a given product, is most commonly employed when inventory items are so intertwined that it becomes difficult to assign a specific cost to an individual unit. This is frequently the case when the inventory items in question are identical to one another.

Does LIFO match the flow of costs?

It should be understood that, although LIFO matches the most recent costs with sales on the income statement, the flow of costs does not necessarily have to match the flow of the physical units. Generally speaking, FIFO is preferable in times of rising prices, so that the costs recorded are low, and income is higher.

What is the difference between FIFO and Weighted Average?

The inventory will be excluded from a business based on an average cost of all goods present in a business. FIFO method will report higher profits if inflation is rising and vice versa. Weighted average method will report higher profits if inflation is decreasing and vice versa.

What is the difference between FIFO and FIFO?

Primary distinction: The primary difference between the two methods is the cost ascertained to the inventory that is dispatched or sold by a business. In FIFO method, the basic assumption followed is that inventory which is acquired first or enters the business first will be the first to exit.

What is weighted average method?

In weighted average method, the inventory will be dispatched on the basis of a weighted average of costs of all the inventory present in a business at the time of dispatch. It means that for every dispatch a new cost will be calculated and allocated to the inventory if the business follows a perpetual system of inventory valuation which is more ...

How does inventory valuation affect financial figures?

Impact on financial figures: The method of inventory valuation can affect the important financial figures of a company especially revenues and profits. In a time of rising inflation, the profits for a company will be shown increased under FIFO method as compared to weighted average method, because the goods will be sold on higher prices but ...

What is FIFO in inventory?

FIFO is an inventory valuation method in which inventory is dispatched on a first-in-first-out basis. So, inventory acquired/manufactured first is dispatched first, thus following a chronological order.

Why is FIFO important?

Inventory valuation is important because it affects many other vital figures especially those written in the financial statements of a business e.g. cost of goods sold, gross profit, the value of closing inventory mentioned in total assets etc.

Is FIFO easier to implement than weighted average?

FIFO method is easier to implement as it is easily understandable by the management of a company while the implementation of weighted average method for inventory valuation is more tedious and time consuming exercise. Although, the idea of weighted average method can be understood easily there are increased chances of errors while applying it in real life.

What is FIFO method?

FIFO Method - What It Is, Why & How to Use It. FIFO is a method of valuing inventory and cost of goods sold (COGS). FIFO is an acronym for First In, First Out. With the FIFO method, the assumption is made that the first products purchased (put...

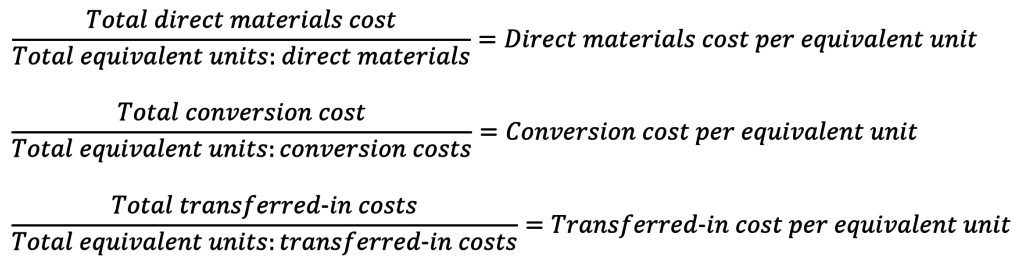

What are the two methods of cost allocation?

There are two methods that can be used to allocate costs in a process costing system. They are weighted-average or FIFO (First In First Out). Accountants and business owners can decide which method to use based on their preference for simplicity or accuracy. Of course, there are differences between the two methods.

Why do businesses use operating leverage?

Businesses use operating leverage to keep costs fixed when they expect extraordinary sales volume. Keeping costs fixed means that businesses can carry more of that revenue to net profit. The...

Does the spreadsheet for business process costing use the weighted average method?

Yes, I know that the Spreadsheets for Business Process Costing example workbook uses the weighted-average method. Confession: it wasn’t until I wrote this post that I really explored the difference between the two methods. If it ever makes sense to redo the process costing example workbook, I will use the FIFO method.

Is beginning WIP factored in unit reconciliation?

You’ll notice that Beginning WIP units aren’t factored into the unit reconciliation calculation for the weighted-average method. With the weighted-average method, Beginning WIP is considered to be started & completed in the current month.

Which method is used by manufacturing companies who mass-produce a bunch of the same product?

Which you should use depends in large part on preference. It also depends on your ability to conceptualize what is taking place. A process costing system is primarily used by manufacturing companies who mass-produce a bunch of the same product.

Is the FIFO method more accurate?

The weighted-average method might be considered simpler. But, the FIFO method might be considered more accurate. That being said, once the groundwork is laid for a FIFO process costing system, calculations should be made automatically and require a minimum of effort on your part. That is…if everything’s set up correctly.

What is the difference between FIFO and weighted average?

The key difference between FIFO and weighted average is that FIFO is an inventory valuation method where the first purchased goods are sold first whereas weighted average method uses the average inventory levels to calculate inventory value. 1.

What is FIFO in accounting?

What is FIFO? FIFO operates under the principle which states that first purchased goods are the ones that should be sold first. In most companies, this is very similar to the actual flow of goods; thus, FIFO is considered to be the most theoretically accurate inventory valuation system among others.

What is the advantage of weighted average method?

The main advantage of weighted average method is that it evens out effects of widely varying prices due to the average use of price. Further, this is a convenient and simple method of inventory valuation. However, the issue of inventory may not reflect the prevailing economic values.

What is FIFO in inventory?

FIFO is an inventory valuation method where the first purchased goods are sold first. Weighted average method uses the average inventory levels to calculate inventory value. FIFO is the most commonly used inventory valuation method. Usage of weighted average method is less compared to FIFO.

Standard Costing: FIFO

First In First Out (FIFO) means the first inventory in will also be the first inventory to be sold. Depending on our Inventory system, we can use either FIFO Periodic or FIFO Perpetual.

Standard Costing: Weighted Average

The weighted average method weighs the average cost of Inventory, over the period. Depending on our Inventory system, we can use either Weighted Average Periodic or Weighted Average Perpetual.

Sign Up!

Click our Sign Up button (top of page) to receive updates, additional exam prep information and to connect with our community.

Weighted Average vs. FIFO vs. LIFO: An Overview

Weighted Average

- The weighted average method, which is mainly utilized to assign the average cost of production to a given product, is most commonly employed when inventory items are so intertwined that it becomes difficult to assign a specific cost to an individual unit. This is frequently the case when the inventory items in question are identical to one another. Furthermore, this method assumes …

First In, First Out

- The first in, first out (FIFO) accounting method relies on a cost flow assumption that removes costs from the inventory account when an item in someone’s inventory has been purchased at varying costs, over time. When a business uses FIFO, the oldest cost of an item in an inventory will be removed first when one of those items is sold. This oldest cost will then be reported on the in…

Last In, First Out

- The last in, first out (LIFO) accounting method assumes that the latest items bought are the first items to be sold. With this accounting technique, the costs of the oldest products will be reported as inventory. It should be understood that, although LIFO matches the most recent costs with sales on the income statement, the flow of costs does not necessarily have to match the flow o…

Weighted Average vs. FIFO vs. LIFO Example

- Consider this example: Suppose you own a furniture store and you purchase 200 chairs for $10 per unit. The next month, you buy another 300 chairs for $20 per unit. At the end of an accounting period, let's assume you sold 100 total chairs. The weighted average costs, using both FIFO and LIFO considerations are as follows: 1. 200 chairs at $10 per chair = $2,000. 300 chairs at $20 pe…

Key Difference – FIFO vs Weighted Average

What Is FIFO?

- FIFO operates under the principle which states that first purchased goods are the ones that should be sold first. In most companies, this is very similar to the actual flow of goods; thus, FIFO is considered to be the most theoretically accurate inventory valuation system among others. E.g. ABC Ltd. is a bookstore that sells study material (books) to universities. Consider the following …

What Is Weighted average?

- This method values inventory by dividing the cost of the goods available for sale by the number of goods, thus calculating an average cost. This helps to arrive at a value that does not represent oldest or latest units. Considering the same example, E.g. Total number of books, 1000 books @ $ 250 = $ 250,000 1500 books @ $ 200 = $ 300,000 1850 books @ $ 315 = $ 582,750 Cost of a bo…

Summary – FIFO vs Weighted Average

- While both FIFO and weighted average are popular inventory valuation methods, companies can decide which method to use based on their discretion. The difference between the two depends on the way the inventory is issued; one method sells the goods purchased first (FIFO) and the other calculates the average price for the total inventory (weighted av...