Using FIFO

FIFO

FIFO is an acronym for first in, first out, a method for organising and manipulating a data buffer, where the oldest entry, or 'head' of the queue, is processed first. It is analogous to processing a queue with first-come, first-served behaviour: where the people leave the queue in the order in …

Why do companies use FIFO and LIFO?

Key takeaway: FIFO and LIFO allow businesses to calculate COGS differently. From a tax perspective, FIFO is more advantageous for businesses with steady product prices, while LIFO is better for businesses with rising product prices.

What companies use the LIFO method?

Here are some of the industries that often use the LIFO method:Automotive industries when needing to quickly ship.Petroleum-based production companies.Pharmaceutical industries with some products.

What type of company would use FIFO?

Companies must use FIFO for inventory if they are selling perishable goods such as food, which expires after a certain period of time. Companies selling products with relatively short demand cycles, such as designer fashion, also may have to pick FIFO to ensure they are not stuck with outdated styles in inventory.

When should a company use FIFO?

When Is First In, First Out (FIFO) Used? The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

Do companies usually use FIFO or LIFO?

Although there are other ways to calculate the cost of goods sold, most businesses use either the first-in-first-out (FIFO) or last-in-first-out (LIFO) method of accounting to value their inventory. FIFO means the items purchased first are sold first.

Do most companies use LIFO or FIFO?

Most companies prefer FIFO to LIFO because there is no valid reason for using recent inventory first, while leaving older inventory to become outdated. This is particularly true if you're selling perishable items or items that can quickly become obsolete.

Why would a company use LIFO?

The primary reason that companies choose to use an LIFO inventory method is that when you account for your inventory using the “last in, first out” method, you report lower profits than if you adopted a “first in, first out” method of inventory, known commonly as FIFO.

Does Nike use FIFO or LIFO?

Inventories are valued on a Ñrst-in, Ñrst-out (FIFO) basis. During the year ended May 31, 1999, the Company changed its method of determining cost for substantially all of its U.S. inventories from last-in, Ñrst-out (LIFO) to FIFO. See Note 11.

Where is LIFO used?

Last in, first out (LIFO) is a method used to account for inventory. Under LIFO, the costs of the most recent products purchased (or produced) are the first to be expensed. LIFO is used only in the United States and governed by the generally accepted accounting principles (GAAP).

When should LIFO be used?

During times of rising prices, companies may find it beneficial to use LIFO cost accounting over FIFO. Under LIFO, firms can save on taxes as well as better match their revenue to their latest costs when prices are rising.

What is LIFO and FIFO with example?

First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method. Last-in, first-out (LIFO) assumes the last inventory added will be the first sold. Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

Why do businesses use FIFO?

If your inventory costs are going down as time goes on, FIFO will allow you to claim a higher average cost-per-piece on newer inventory, which can help you save money on your taxes. Additionally, FIFO does not require as much recordkeeping as LIFO, because it assumes that older items are gone.

What is a FIFO?

FIFO is mostly recommended for businesses that deal in perishable products. The approach provides such ventures with a more accurate value of their profits and inventory. FIFO is not only suited for companies that deal with perishable items but also those that don’t fall under the category.

How does LIFO work?

Apart from reducing the tax liability, using the LIFO technique offers other benefits, such as: 1 It complies better with the matching principle, as it charges costs with the revenues of a similar period 2 Reduces the likelihood of write-downs of inventory if their fair market value has decreased 3 In some industries, it conforms with the actual physical flow of inventory, such as in extraction industries (i.e., coal, oil and gas)

What is LIFO system?

The LIFO system is founded on the assumption that the latest items to be stored are the first items to be sold. It is a recommended technique for businesses dealing in products that are not perishable or ones that don’t face the risk of obsolescence.

What are the benefits of LIFO?

Apart from reducing the tax liability, using the LIFO technique offers other benefits, such as: It complies better with the matching principle, as it charges costs with the revenues of a similar period. Reduces the likelihood of write-downs of inventory if their fair market value has decreased.

What is the LIFO method?

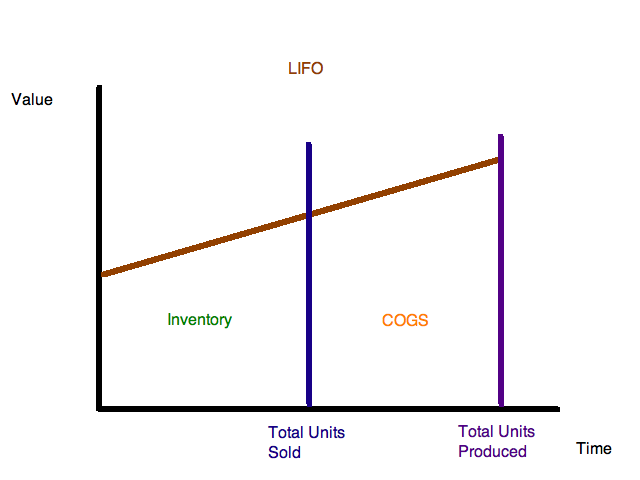

Whenever there are price increases, such as in an inflationary period, the LIFO method has the impact of recording the sale of higher-priced items first while the cheaper, older products are maintained as stock. Doing so causes a firm’s cost of goods sold to increase and the net income to decrease.

What are the drawbacks of LIFO?

One of its drawbacks is that it does not correspond to the normal physical flow of most inventories. Also, the LIFO approach tends to understate the value of the closing stock and overstate COGS, which is not accepted by most taxation authorities.

What are the advantages of FIFO?

The biggest advantage of FIFO lies in its simplicity. It is easy to use, generally accepted and trusted, and it follows the natural physical flow of inventory. Another advantage is that there’s less wastage when it comes to the deterioration of materials.

What is FIFO in accounting?

FIFO and LIFO are methods used in the cost of goods sold calculation. FIFO (“First-In, First-Out”) assumes that the oldest products in a company’s inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company’s inventory have been sold first ...

Why are FIFO profits more accurate?

Although this may mean less tax for a company to pay under LIFO, it also means stated profits with FIFO are much more accurate because older inventory reflects the actual costs of that inventory. If profits are naturally high under FIFO, then the company becomes that much more attractive to investors.

What is LIFO reserve?

The LIFO reserve is the amount by which a company’s taxable income has been deferred, as compared to the FIFO method. The remaining unsold 350 televisions will be accounted for in “inventory”.

Is LIFO more attractive than FIFO?

You can see how for Ted, the LIFO method may be more attractive than FIFO. This is because the LIFO number reflects a higher inventory cost, meaning less profit and less taxes to pay at tax time. The LIFO reserve in this example is $31,250.

Can a company use unsold inventory to calculate cost of goods?

Lastly, the product needs to have been sold to be used in the equation. A company cannot apply unsold inventory to the cost of goods calculation.

Is LIFO legal in the US?

Under GAAP, LIFO is legal. Outside the United States, LIFO is not permitted as an accounting practice. This is why you’ll see some American companies use the LIFO method on their financial statements, and switch to FIFO for their international operations.

What is a LIFO?

LIFO and FIFO are the two most common inventory methods that are used by a company. The goal is to properly account for cost of purchased inventory on the balance sheet. Generally, a business can calculate its inventory either directly or through profits shown in the income statement and the cash flow statement.

What is LIFO in accounting?

LIFO or "last-in, first-out" is a method of accounting for inventory that assumes an inventory unit which is bought first will come out last. It also means that the first unit to be sold is the last inventory that comes into the warehouse. Under LIFO, if there is the last units of inventory purchased were bought at the highest price, ...

What are the advantages of LIFO?

There are several advantages of LIFO for inventory accounting method: 1) Easy to compare current costs with current income, 2) If prices increase then the price of goods becomes conservative, 3) Operating profit is not affected by profit or loss from price fluctuations, 4) More tax savings.

Why is LIFO used?

LIFO is well used in inventory accounting to increase the cost of goods sold by a company. It is also used to reduce net profits, which can then reduce corporate tax liability. So, it is not surprising that LIFO is much more desirable when the corporate tax rate is higher.

What does FIFO mean in warehouse?

FIFO (First-In, First-Out) As the name suggests, FIFO means the first entry comes out first. This method assumes that the first units to enter warehouse are sold first. So, the oldest items are sold first. This system is usually used by companies with perishable inventory.

Which takes the most investment of funds?

Inventory usually takes the most investment of funds. One way to calculate the profits generated by a company is to track sales revenues and all the costs involved in producing the goods.

What does FIFO mean in inventory?

FIFO stands for “first in, first out” and assumes the first items entered into your inventory are the first ones you sell. LIFO, also known as “last in, first out,” assumes the most recent items entered into your inventory will be the ones to sell first. The inventory valuation method you choose will depend on your tax situation, ...

What is the LIFO method?

Recordkeeping. If you choose to use the LIFO method of inventory valuation, you will need a recordkeeping system that allows you to determine when you access older “layers” of inventory and then apply the cost of that older inventory accurately.

What is the best way to value inventory?

There are a number of ways you can value your inventory, and choosing the best inventory valuation method for your business depends on a variety of factors. FIFO and LIFO are the two most common inventory valuation methods. FIFO stands for “first in, first out” and assumes the first items entered into your inventory are the first ones you sell.

What is inventory flow?

Inventory flow: Most businesses sell the oldest items in stock first. Think of a grocery store or a clothing boutique: In both of these types of businesses, stock loses its value with time, and so the older items are pushed to the front of the shelves to help them sell quicker.

Can you use LIFO or FIFO valuation?

Inventory flow. For spools of craft wire, you can reasonably use either LIFO or FIFO valuation. For perishable goods — like groceries — or other items that lose their value with time, using LIFO valuation doesn’t make sense because you will always try to sell older inventory first.

Can you use LIFO for inventory?

You can choose to value all your inventory using LIFO, or you can use LIFO just for certain goods you carry. Once you elect to use LIFO for your inventory valuation, you cannot switch back to FIFO or another inventory valuation method without express permission from the IRS. To request a change in inventory valuation from the IRS, ...

Is LIFO more onerous than FIFO?

Recordkeeping: When comparing FIFO vs. LIFO, the recordkeeping requirements for LIFO are typically more onerous than those for FIFO. This is because the inventory in a business that uses LIFO is “layered,” meaning older inventory can be held for long periods of time.

What is FIFO vs LIFO?

FIFO is a more realistic and logical approach of inventory valuation compared to LIFO. There is a risk of stocks, getting obsolete and outdated in case of LIFO, as goods are used from old stock, this risk can be reduced if FIFO is used. Unlike LIFO, record maintenance is easier in FIFO, as several layering is less.

What happens if you use LIFO?

If LIFO is used, only old inventory will remain in stock, and its purchase price will have a lesser chance of going below its carrying value. Carrying Value Carrying value is the book value of assets in a company's balance sheet, computed as the original cost less accumulated depreciation/impairments.

What is FIFO in accounting?

FIFO is the globally and widely used method for inventory valuation. While US GAAP allows adopting LIFO as well as FIFO, but in the international scenarios, FIFO is widely used, and IFRS restricts the use of LIFO for inventory valuation. Under LIFO, stock in hand represents the oldest stock, while in FIFO, stock in hand represents the latest stock.

Why is the LIFO method not attractive?

Investment potential. Using the LIFO method may not attract potential investors, as the use of LIFO leads to lower net income. Using the FIFO method helps the investors to understand the current scenario. It helps to attract investors.

Why use LIFO method?

So ultimately, the benefit of using the LIFO method for a company is that it can report a lower Net Income and hence defer its tax liabilities during the times of high inflation.

What does LIFO mean in stock?

LIFO stands for Last In, First Out, which implies that the inventory which was added last to the stock will be removed from the stock first. So the inventory will leave the stock in an order reverse of that in which it was added to the stock.

What does "in inventory leave the stock" mean?

It means that whenever the inventory is reported as sold (either after conversion to finished goods or as it is), its cost will be taken equal to the cost of the oldest inventory present in the stock.

Why do companies use LIFO?

A final reason that companies elect to use LIFO is that there are fewer inventory write-downs under LIFO during times of inflation. An inventory write-down occurs when the inventory is deemed to have decreased in price below its carrying value .

What is LIFO for businesses?

Businesses that sell products that rise in price every year benefit from using LIFO. When prices are rising, a business that uses LIFO can better match their revenues to their latest costs.

Why is LIFO so controversial?

The higher COGS under LIFO decreases net profits and thu s creates a lower tax bill for One Cup. This is why LIFO is controversial; opponents argue that during times of inflation, LIFO grants an unfair tax holiday for companies. In response, proponents claim that any tax savings experienced by the firm are reinvested and are of no real consequence to the economy. Furthermore, proponents argue that a firm's tax bill when operating under FIFO is unfair (as a result of inflation).

How does LIFO work?

How Last in, First out (LIFO) Works. Under LIFO, a business records its newest products and inventory as the first items sold. The opposite method is FIFO, where the oldest inventory is recorded as the first sold. While the business may not be literally selling the newest or oldest inventory, it uses this assumption for cost accounting purposes.

Why is LIFO used?

When prices are rising, it can be advantageous for companies to use LIFO because they can take advantage of lower taxes. Many companies that have large inventories use LIFO, such as retailers or automobile dealerships.

What is the LIFO method?

Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first . This method is banned under the International Financial Reporting Standards ...

Why do supermarkets use LIFO?

For example, many supermarkets and pharmacies use LIFO cost accounting because almost every good they stock experiences inflation. Many convenience stores—especially those that carry fuel and tobacco—elect to use LIFO because the costs of these products have risen substantially over time.

Why use FIFO?

When using FIFO, you’ll have to more accurately display what you paid for the oldest inventory, whether that be more or less . Profits will often seem higher when using FIFO, which is more attractive to investors.

Why is FIFO important?

The FIFO method will help you to maximize profits on your inventory without having to risk as many variables. As you’d probably guess, based on the pros and cons, FIFO makes sense for many more business models and is seen to be more of an industry standard.

What is the opposite of LIFO?

The FIFO method is opposite to LIFO in that, the items that have been in your warehouse the longest would be sold first. This is a standard method at grocery stores and other similar suppliers where products will deteriorate or expire with age.

What is the LIFO method?

The LIFO method uses the practice of taking the items that were last received into your warehouse and selling them or shipping them first. So, selling or shipping the newest, most recent items first. When using the LIFO method, you’ll more easily be able to manipulate financial statements and tax documents in your favor.

Is LIFO compatible with IFRS?

Not compatible with the IFRS (International Financial Reporting Standards) accounting method. Lower earnings which can discourage investors. As you can see, there are quite a few variables that determine whether your warehouse will see success using the LIFO to manage inventory within the warehouse.

Last In, First Out

- The LIFO system is founded on the assumption that the latest items to be stored are the first items to be sold. It is a recommended technique for businesses dealing in products that are not perishable or ones that don’t face the risk of obsolescence. Whenever there are price increases, such as in an inflationary period, the LIFO method has the impact of recording the sale of higher …

First In, First Out

- With FIFO, the assumption is that the first items to be produced are also the first items to be sold. For example, let’s say a grocery receives 30 units of milk on Mondays, Thursdays, and Saturdays. The store owner will put the older milk at the front of the shelf, with the hopes that the Monday shipment will sell first. Under the first-in, first-out technique, the store owner will assume that all …

Why Use FIFO?

- The biggest advantage of FIFO lies in its simplicity. It is easy to use, generally accepted and trusted, and it follows the natural physical flow of inventory. Another advantage is that there’s less wastage when it comes to the deterioration of materials. Since the first items acquired are also the first ones to be sold, there is effective utilization and management of inventory.

Wrap Up

- The LIFO vs. FIFO methods are different accounting treatments for inventory that produce different results. Although LIFO is an attractive choice for those looking to keep their taxable incomes low, the FIFO method provides a more accurate financial picture of a company’s finances and is easier to implement.

Related Readings

- Thank you for reading our guide on LIFO vs. FIFO accounting methods. CFI offers the Financial Modeling & Valuation Analyst (FMVA)®certification program for those looking to take their careers to the next level. To learn more, the following resources will be helpful: 1. Days Inventory Outstanding 2. Day Sales Outstanding 3. Inventory Turnover 4. Lead Time