With perpetual FIFO, the first (or oldest) costs are the first removed from the Inventory account and debited to the Cost of Goods Sold account. Therefore, the perpetual FIFO cost flows and the periodic FIFO cost flows will result in the same cost of goods sold and the same cost of the ending inventory. Confused? Send Feedback Perpetual LIFO

What is the difference between FIFO vs. LIFO?

- First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method.

- Last-in, first-out (LIFO) assumes the last inventory added will be the first sold.

- Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

What is FIFO inventory management method and why use it?

The advantages to the FIFO method are as follows:

- The method is easy to understand, universally accepted and trusted.

- FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first). ...

- Less waste (a company truly following the FIFO method will always be moving out the oldest inventory first).

How to calculate LIFO and FIFO?

These are the simple steps that help to convert a LIFO-based statement to a FIFO-based statement:

- First, you have to add the LIFO reserve to LIFO inventory

- Then, you have to deduct the excess cash that saved from lower taxes under LIFO (i:e. ...

- Very next, you have to increase the retained earnings component of shareholders’ equity by the LIFO reserve x (1-T)

- Finally, in the income statement, FIFO COGS = LIFO COGS – Δ LIFO Reserve

How to sell stock with FIFO or LIFO?

How to Sell Stock with LIFO or FIFO

- Cost Basis. When you buy a stock, the amount you pay is called your cost basis. ...

- LIFO and FIFO. LIFO and FIFO tells the IRS the order in which you want to sell off your stock. ...

- Example. Say you bought stock on three different days. ...

- Suitability. LIFO and FIFO shift around the timing of your taxes. ...

Does perpetual use FIFO?

Perpetual FIFO is a cost flow tracking system under which the first unit of inventory acquired is presumed to be the first unit consumed or sold.

How do you record perpetual inventory in FIFO?

0:446:22FIFO (Perpetual Inventory) - YouTubeYouTubeStart of suggested clipEnd of suggested clipWe had 10 units at $5 apiece so under beginning inventory. We write 10 at $5 equals 50 dollars so weMoreWe had 10 units at $5 apiece so under beginning inventory. We write 10 at $5 equals 50 dollars so we take our number of units 10 and multiply it by our unit cost of 5 to get that 50.

Is perpetual inventory FIFO or LIFO?

FIFO, LIFO, Perpetual, Periodic Under FIFO, it is assumed that items purchased first are sold first. Under LIFO, it is assumed that items purchased last are sold first. Perpetual inventory system updates inventory accounts after each purchase or sale.

What does FIFO result in?

FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet. As a result, FIFO can increase net income because inventory that might be several years old–which was acquired for a lower cost–is used to value COGS.

Why is FIFO the same for periodic and perpetual?

With perpetual FIFO, the first (or oldest) costs are the first removed from the Inventory account and debited to the Cost of Goods Sold account. Therefore, the perpetual FIFO cost flows and the periodic FIFO cost flows will result in the same cost of goods sold and the same cost of the ending inventory.

How do you solve a perpetual inventory system?

0:036:40Perpetual Inventory Accounting - YouTubeYouTubeStart of suggested clipEnd of suggested clipSo perpetual inventory is basically an inventory system where we're going to continuously update.MoreSo perpetual inventory is basically an inventory system where we're going to continuously update. The inventory account every time we have a purchase of inventory we have a sale of inventory.

Does perpetual inventory use LIFO?

Like first-in, first-out (FIFO), last-in, first-out (LIFO) method can be used in both perpetual inventory system and periodic inventory system. The following example explains the use of LIFO method for computing cost of goods sold and the cost of ending inventory in a perpetual inventory system.

How do you create a perpetual inventory record using LIFO?

0:156:13LIFO Perpetual Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipOkay so on January 1st they purchase 20 units at $35 a unit and then 5 days later they purchase 30MoreOkay so on January 1st they purchase 20 units at $35 a unit and then 5 days later they purchase 30 units for $40 a unit and then on January 8th. They sold 40 units now they also made a purchase later.

How does the purchase of inventory on account under the perpetual inventory method affect the financial statements?

How does the purchase of inventory on account under the perpetual inventory method affect the financial statements? Total assets and total liabilities both increase. The term "FOB Shipping Point" means: The buyer pays the shipping cost.

How does FIFO affect the balance sheet?

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

What is perpetual inventory system?

A perpetual inventory system is a program that continuously estimates your inventory based on your electronic records, not a physical inventory. This system starts with the baseline from a physical count and updates based on purchases made in and shipments made out.

How does FIFO affect cost of goods sold?

(a) First-in, First-out (FIFO): Under FIFO, the cost of goods sold is based upon the cost of material bought earliest in the period, while the cost of inventory is based upon the cost of material bought later in the year. This results in inventory being valued close to current replacement cost.

B1. Perpetual FIFO

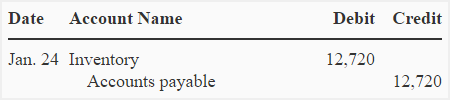

Under the perpetual system the Inventory account is constantly (or perpetually) changing. When a retailer purchases merchandise, the retailer debit...

B2. Perpetual LIFO

Under the perpetual system the Inventory account is constantly (or perpetually) changing. When a retailer purchases merchandise, the retailer debit...

B3. Perpetual Average

Under the perpetual system the Inventory account is constantly (or perpetually) changing. When a retailer purchases merchandise, the costs are debi...

Comparison of Cost Flow Assumptions

Below is a recap of the varying amounts for the cost of goods sold, gross profit, and ending inventory that were calculated above.The example assum...

What is a perpetual FIFO?

With perpetual FIFO, the first (or oldest) costs are the first removed from the Inventory account and debited to the Cost of Goods Sold account. Therefore, the perpetual FIFO cost flows and the periodic FIFO cost flows will result in the same cost of goods sold and the same cost of the ending inventory.

Why is a perpetual LIFO entry needed?

An entry is needed at the time of the sale in order to reduce the balance in the Inventory account and to increase the balance in the Cost of Goods Sold account. If the costs of the goods purchased rise throughout the entire year, perpetual LIFO will result in a lower cost of goods sold and a higher net income than periodic LIFO.

How many entries are recorded in a perpetual system?

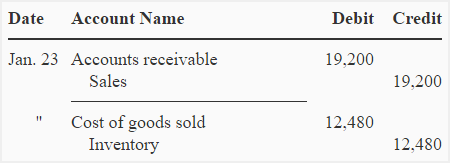

Under the perpetual system, two entries are recorded when merchandise is sold: (1) the amount of the sale is debited to Accounts Receivable or Cash and is credited to Sales, and (2) the cost of the merchandise sold is debited to the account Cost of Goods Sold and is credited to Inventory. (Note: Under the periodic system the second entry is not made.)

What is perpetual inventory?

When using the perpetual system, the Inventory account is constantly (or perpetually) changing. The Inventory account is updated for every purchase and every sale. Under the perpetual system, two transactions are recorded at the time that the merchandise is sold: (1) the amount of the sale is debited to Accounts Receivable or Cash ...

What is FIFO expense?

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

What is the benefit of using FIFO?

1. Better valuation of inventory . By using FIFO, the balance sheet shows a better approximation of the market value of inventory. The latest costs for manufacturing or acquiring the inventory are reflected in inventory, and therefore, the balance sheet reflects the approximate current market value.

Can you use LIFO in Canada?

Therefore, we can see that the balances for COGS and inventory depend on the inventory valuation method. For income tax purposes in Canada, companies are not permitted to use LIFO. However, US companies are able to use FIFO or LIFO.

What is FIFO accounting?

In accounting, First In, First Out (FIFO) is the assumption that a business issues its inventory to its customers in the order in which it has been acquired. Under the FIFO Method, inventory acquired by the earliest purchase made by the business is assumed to be issued first to its customers.

Which inventory system provides the same value of ending inventory under the FIFO method?

As we shall see in the following example, both periodic and perpetual inventory systems provide the same value of ending inventory under the FIFO method.

How to find cost valuation of ending inventory?

To find the cost valuation of ending inventory, we need to track the cost of inventory received and assign that cost to the correct issue of inventory according to the FIFO assumption.

What is the value of ending inventory based on?

In the FIFO Method, the value of ending inventory is based on the cost of the most recent purchases.

What is LIFO inventory method?

The LIFO inventory method assumes that the cost of the latest units purchased are. the last to be allocated to cost of goods sold. the first to be allocated to cost of goods sold. the first to be allocated to ending inventory. not allocated to cost of goods sold or ending inventory.

How many journal entries does a company need to use a perpetual inventory system?

A company which uses a perpetual inventory system needs two journal entries when it sells merchandise. A company which uses a perpetual inventory system debits inventory and credits cost of goods sold when it sells merchandise. None of the answer choices are correct.

What is the difference between a perpetual and periodic inventory system?

A perpetual inventory system computes cost of goods sold only at the end of the accounting period. A periodic inventory system computes cost of goods sold each time a sale occurs. A perpetual inventory system provides better control over inventories than does a periodic inventory system.

What does the cost of the earliest units purchased assume?

It assumes that the cost of the earliest units purchased are the last to be allocated to the beginning inventory. It assumes that the cost of the earliest units purchased are the first to be allocated to cost of goods sold. It assumes that the cost of the earliest units purchased are the first to be allocated to cost of goods sold.

Why is an assumption about cost flow necessary?

the first to be allocated to cost of goods sold. An assumption about cost flow is necessary. because it is required by the income tax regulation. because prices usually change, and tracking which units have been sold is difficult. even when there is no change in the purchase price on inventory.

When using the periodic system, what is the physical inventory count used to determine?

When using the periodic system the physical inventory count is used to determine. only the sales value of goods in the ending inventory. only the cost of merchandise sold during the period. both the cost of the goods in ending inventory and the sales value of goods sold during the period.

What is Periodic LIFO?

In a periodic LIFO system, inventory records are only updated at the end of a reporting period.

When are layers stripped away in LIFO?

Under a periodic LIFO system, however, layers are only stripped away at the end of the period, so that only the very last layers are depleted.

What is LIFO in inventory?

The basic concept underlying perpetual LIFO is the last in, first out (LIFO) cost layering system. Under LIFO, you assume that the last item entering inventory is the first one to be used. For example, consider stocking the shelves in a food store, where a customer purchases the item in front, which was likely to be the last item added to the shelf by a clerk. These LIFO transactions are recorded under the perpetual inventory system, where inventory records are constantly updated as inventory-related transactions occur.

Is LIFO more common than periodic?

The costing results of a perpetual LIFO system are more common than a periodic LIFO system, since most inventory is now tracked using computerized systems that maintain inventory records on a real-time basis.

What is the difference between LIFO and LIFO perpetual?

The reason is that under LIFO periodic system, the total of sales (or issues) is matched with the total of purchases (including beginning inventory, if any) at the end of the period whereas under LIFO perpetual system, each sale (or issue) is matched with the immediate preceding purchases.

Is LIFO periodic or perpetual?

The reason is that the LIFO periodic system does not take into account the exact dates involved but LIFO perpetual does.

Example of First-In, First-Out

FIFO vs. LIFO

- To reiterate, FIFO expenses the oldest inventories first. In the following example, we will compare FIFO to LIFO (last in first out)Last-In First-Out (LIFO)The Last-in First-out (LIFO) method of inventory valuation is based on the practice of assets produced or acquired last being the first to be. LIFO expenses the most recent costs first. Consider the same example above. Recall that un…

Impact of FIFO Inventory valuation Method on Financial Statements

- Recall the comparison example of First-In First-Out and LIFO. The two methods yield different inventory and COGS. Now it is important to consider the impact of using FIFO on a company’s financial statements?

Key Takeaways from First-In First-Out

- FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold.

- It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system.

- It provides a poor matching of revenue with expenses.

Related Reading

- CFI is a global provider of financial analyst training and career advancement for finance professionals, including the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll t…