Using FIFO generates these results: Cost of goods sold: Selling the older (cheaper) units first generates a lower cost of goods sold than LIFO

FIFO and LIFO accounting

FIFO and LIFO accounting are methods used in managing inventory and financial matters involving the amount of money a company has tied up within inventory of produced goods, raw materials, parts, components, or feed stocks. They are used to manage assumptions of cost flows related to inventory, stock repurchases (if purchased at different prices), and various other accounting purposes.

Full Answer

What is FIFO and how does it work?

FIFO stands for “First-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company’s inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation. How Do You Calculate FIFO?

How do you calculate FIFO?

How Do You Calculate FIFO? To calculate COGS (Cost of Goods Sold) using the FIFO method, determine the cost of your oldest inventory. Multiply that cost by the amount of inventory sold.

What are the advantages and disadvantages of FIFO method?

Advantages of FIFO method The first in first out (FIFO) method of inventory valuation has the following advantages for business organization: FIFO method saves money and time in calculating the exact cost of the inventory being sold because the cost will depend upon the most former cash flows of purchases to be used first.

Does FIFO increase net income?

FIFO gives us a good indication of ending inventory value, but it also increases net income because inventory that might be several years old is used to value COGS. And although increasing net income sounds good, remember that it also has the potential to increase the amount of taxes that a company must pay.

.gif)

What does FIFO result in?

FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet. As a result, FIFO can increase net income because inventory that might be several years old–which was acquired for a lower cost–is used to value COGS.

How do you work out FIFO?

To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

How do you find ending inventory using FIFO?

According to the FIFO method, the first units are sold first, and the calculation uses the newest units. So, the ending inventory would be 1,500 x 10 = 15,000, since $10 was the cost of the newest units purchased.

How does FIFO affect cost of goods sold?

(a) First-in, First-out (FIFO): Under FIFO, the cost of goods sold is based upon the cost of material bought earliest in the period, while the cost of inventory is based upon the cost of material bought later in the year. This results in inventory being valued close to current replacement cost.

How do you calculate cost of goods sold and ending inventory using FIFO?

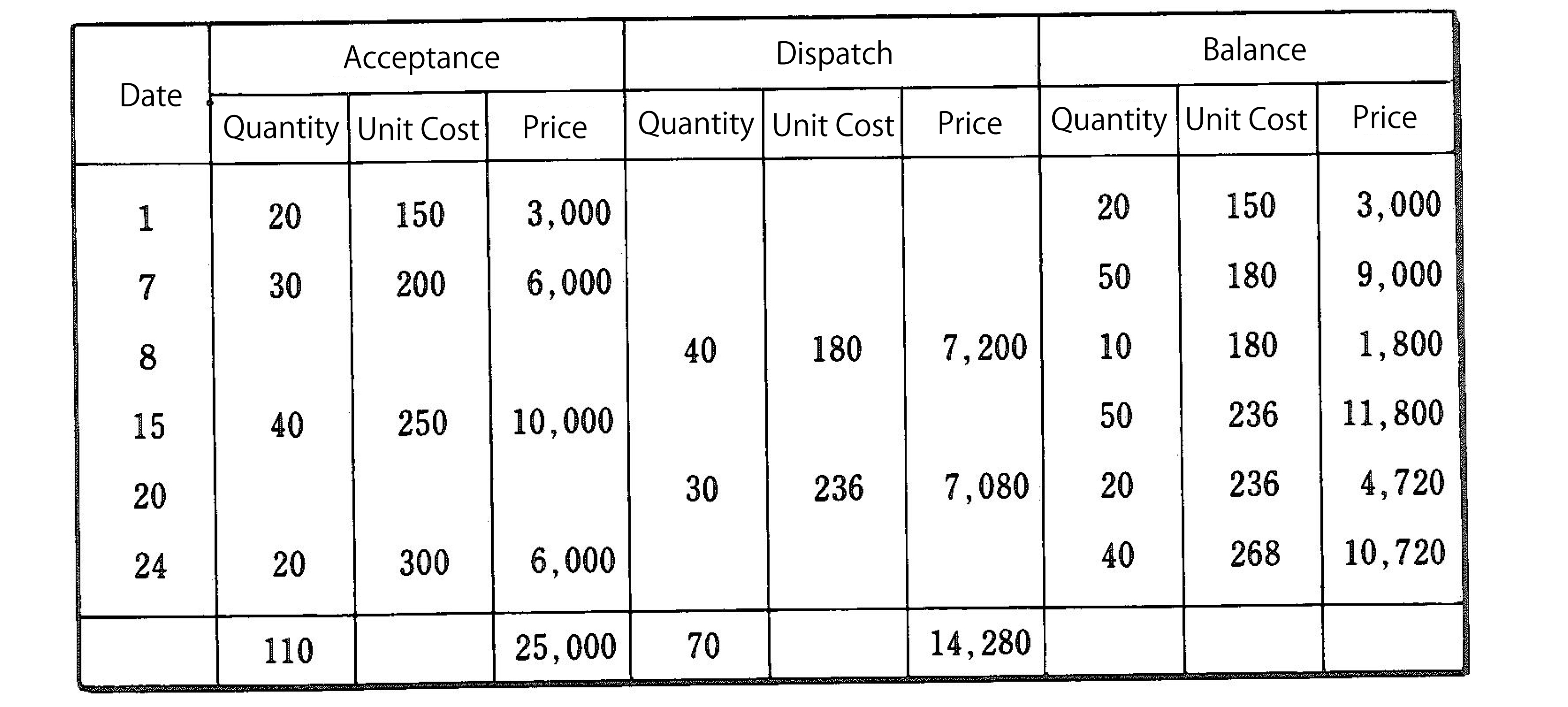

2:478:04FIFO Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipWe don't know which ones they were that we actually sold it could have been any of these so that'sMoreWe don't know which ones they were that we actually sold it could have been any of these so that's why we make an assumption. We make a cost flow assumption to tell us which units we're going to

How do you calculate cost of goods sold using the FIFO periodic inventory method?

2:024:57FIFO Periodic Inventory Method - YouTubeYouTubeStart of suggested clipEnd of suggested clipSo then the next 20 units are gonna come out of this 30 from January 6 purchase. So that's 20 unitsMoreSo then the next 20 units are gonna come out of this 30 from January 6 purchase. So that's 20 units at $40 a unit. So we add those together and that gives us $1,500. As our cost of goods sold.

Why FIFO method is used?

FIFO (first in, first out) inventory management seeks to sell older products first so that the business is less likely to lose money when the products expire or become obsolete. LIFO (last in, first out) inventory management applies to nonperishable goods and uses current prices to calculate the cost of goods sold.

What FIFO means?

First In First OutFIFO = First In First Out FIFO means that products stored first are to be retrieved first.

How do you find the gross profit in FIFO?

For example, suppose a company's oldest inventory cost $200, the newest cost $400, and it has sold one unit for $1,000. Gross profit would be calculated as $800 under LIFO and $600 under FIFO.

Does FIFO give a higher or lower cost of sales?

Generally speaking, FIFO is preferable in times of rising prices, so that the costs recorded are low, and income is higher.

What happens to FIFO when prices fall?

The FIFO method can help lower taxes (compared to LIFO) when prices are falling. However, for the most part, prices tend to rise over the long term, meaning FIFO would produce a higher net income and tax bill over the long term.

Does FIFO increase assets?

This will reduce your Cost of Goods Sold, increasing your net income. You will also have a higher ending inventory value on your balance sheet, increasing your assets. This can benefit early businesses looking to get loans and funding from investors.

What is FIFO method?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

What is FIFO in manufacturing?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense. Under FIFO, it is assumed that the cost of inventory purchased first will be recognized first. The dollar value of total inventory decreases in this process because inventory has been removed from the company’s ownership. The costs associated with the inventory may be calculated in several ways — one being the FIFO method.

What is the opposite of FIFO?

The opposite of FIFO is LIFO (Last In, First Out), where the last item purchased or acquired is the first item out. In inflationary economies, this results in deflated net income costs and lower ending balances in inventory when compared to FIFO.

What is FIFO accounting?

First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last. An alternative to FIFO, LIFO is an accounting method in which assets purchased or acquired last are disposed of first.

What are the advantages of first in first out?

What Are the Advantages of First In, First Out (FIFO)? The obvious advantage of FIFO is that it's most widely used method of valuing inventory globally. It is also the most accurate method of aligning the expected cost flow with the actual flow of goods which offers businesses a truer picture of inventory costs.

Why is FIFO preferred?

The advantages to the FIFO method are as follows: The method is easy to understand, universally accepted and trusted. FIFO follows the natural flow of inventory (oldest products are sold first, with accounting going by those costs first).

Why do investors value FIFO?

Investors and banking institutions value FIFO because it is a transparent method of calculating cost of goods sold. It is also easier for management when it comes to bookkeeping, because of its simplicity.

Why is the LIFO method understated?

The value of remaining inventory, assuming it is not-perishable, is also understated with the LIFO method because the business is going by the older costs to acquire or manufacture that product. That older inventory may, in fact, stay on the books forever. Investors and banking institutions value FIFO because it is a transparent method ...

What does FIFO mean in accounting?

FIFO stands for “First-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company’s inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation.

Is FIFO overstating profit?

A company also needs to be careful with the FIFO method in that it is not overstating profit. This can happen when product costs rise and those later numbers are used in the cost of goods calculation, instead of the actual costs.

Is the FIFO method legal?

Both are legal although the LIFO method is often frowned upon because bookkeeping is far more complex and the method is easy to manipulate.

What is the FIFO method?

FIFO stands for first in, first out, an easy-to-understand inventory valuation method that assumes that goods purchased or produced first are sold first. In theory, this means the oldest inventory gets shipped out to customers before newer inventory.

What method of inventory management should you use?

Of course, you should consult with an accountant but the FIFO method is often recommended for inventory valuation purposes.

Leave inventory management to the pros

ShipBob’s tech-enabled retail fulfillment solution is designed for fast-growing B2B ecommerce and direct-to-consumer brands .

FIFO FAQs

Here are answers to the most common questions about the FIFO inventory method.

Why is FIFO accounting used?

FIFO method of accounting saves time, and money spends in calculating the exact inventory cost that is being sold because the recording of inventory is done in the same order as they are purchased or produced. Easy to understand.

What are the disadvantages of FIFO accounting?

One of the biggest disadvantages of FIFO accounting method is inventory valuation during inflation, First In First Out method will result in higher profits, and thus will results in higher “Tax Liabilities” in that particular period. This may result in increased tax charges and higher tax-related cash outflows.

Is the first in first out method a good measure of inventory?

Use of First In First Out method is not a suitable measure of inventory in times of “ hyperinflation .”. During such times, there is no particular pattern of inflation, which may result in prices of goods to inflate drastically.

Does inflation increase operating expenses?

Normally in an inflationary environment, prices are always rising, which will cause an increase in operating expenses, but with FIFO accounting, the same inflation will cause an increase in ending inventory.

What is FIFO in accounting?

The First-In, First-Out (FIFO) method assumes that the first unit making its way into inventory–or the oldest inventory–is the sold first. For example, let's say that a bakery produces 200 loaves of bread on Monday at a cost of $1 each, and 200 more on Tuesday at $1.25 each. FIFO states that if the bakery sold 200 loaves on Wednesday, the COGS ( on the income statement) is $1 per loaf because that was the cost of each of the first loaves in inventory. The $1.25 loaves would be allocated to ending inventory ( on the balance sheet ).

Why is FIFO better than COGS?

FIFO can be a better indicator of the value for ending inventory because the older items have been used up while the most recently acquired items reflect current market prices. For most companies, FIFO is the most logical choice since they typically use their oldest inventory first in the production of their goods, which means the valuation of COGS reflects their production schedule.

Why is LIFO not accurate?

As a result, LIFO doesn't provide an accurate or up-to-date value of inventory because the valuation is much lower than inventory items at today's prices.

Why would COGS be higher under LIFO?

In an inflationary environment, the current COGS would be higher under LIFO because the new inventory would be more expensive. As a result, the company would record lower profits or net income for the period. However, the reduced profit or earnings means the company would benefit from a lower tax liability.

What is LIFO method?

LIFO. When sales are recorded using the LIFO method, the most recent items of inventory are used to value COGS and are sold first. In other words, the older inventory, which was cheaper, would be sold later.

What is the first in first out method?

The First-In, First-Out (FIFO) method assumes that the oldest unit of inventory is the sold first. LIFO is not realistic for many companies because they would not leave their older inventory sitting idle in stock. FIFO is the most logical choice since companies typically use their oldest inventory first in the production of their goods.

When sales are recorded using the FIFO method, what is the oldest inventory?

When sales are recorded using the FIFO method, the oldest inventory–that was acquired first–is used up first. FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet.

What are the advantages of using FIFO?

Advantages of FIFO. Simple to use. Yields are ending inventory amount on the balance sheet comprising more current costs than if the weighted average or LIFO is used. Usually produces a cost flow that approximates physical flow better than does weighted average or LIFO.

Why do companies use FIFO?

In an economy of rising prices (during inflation), it is common for beginning companies to use FIFO for reporting the value of merchandise to bolster their balance sheet. As the older and cheaper goods are sold, the newer and more expensive goods remain as assets on the company’s books.

What are the disadvantages of FIFO?

Disadvantages of FIFO. It does not match recent costs with current revenue, as well as LIFO, does. Yields a higher taxable income than LIFO or weighted average during periods of rising prices.

What is the first in first out method?

Under the first-in-first-out method, the earliest costs (first costs) are assigned to the cost of goods sold, and the remaining costs (the more recent costs) are assigned to ending inventory.

Does FIFO increase income?

On the other hand, FIFO increases net income (due to the age of the inventory being used in the cost of goods sold), and Increased net income can increase taxes owed.

First In First Out

In accounting, First In, First Out (FIFO) is the assumption that a business issues its inventory to its customers in the order in which it has been acquired.

Example 1 (Perpetual)

Bill sells a specific model of a toaster on his website for $12 apiece.

FIFO: Periodic Vs. Perpetual

The example above shows how a perpetual inventory system works when applying the FIFO method.

Example 2 (Periodic)

In the first example, we worked out the value of ending inventory using the FIFO perpetual system at $92.

What is the advantage of FIFO method?

The first in first out (FIFO) method of inventory valuation has the following advantages for business organization: FIFO method saves money and time in calculating the exact cost of the inventory being sold because the cost will depend upon the most former cash flows of purchases to be used first.

Why is FIFO not appropriate?

FIFO will not be an appropriate measure if the materials/goods purchased have fluctuating price patterns, because this can result in misstated profits for the same period as different costs of same goods during that same period are recorded.

What is the first in first out method of inventory valuation?

The first in first out (FIFO) method of inventory valuation has the following advantages for business organization: 1 FIFO method saves money and time in calculating the exact cost of the inventory being sold because the cost will depend upon the most former cash flows of purchases to be used first. 2 It is a simple concept which is easy to understand. Even a layman can grab the idea with little explanation. The managers with little to no accounting information would be able to understand it easily. 3 It is a fairly practical approach to use, as sometimes it becomes difficult to identify the costs of the products sold at the point of sale and FIFO rectifies the matter. 4 It is a widely used and accepted approach of valuation which increases its comparability and consistency. 5 It makes manipulation of the income reported in financial statements difficult, as under FIFO policy there remains no vagueness about the values to be used in cost of sales figure of profit/loss statement. 6 FIFO will show increased gross and net profits in times of increasing prices of goods.#N#Cost of sales = opening stock + Purchases – closing stock#N#This is because the “cost of sales” consists of figure of inventory and as first inventories will have less cost than recent inventories during inflation, the profits reported would be higher.

What are the disadvantages of using a FIFO valuation method?

The major disadvantages of using a FIFO inventory valuation method are given below: One of the biggest disadvantage of FIFO approach of valuation for inventory/stock is that in the times of inflation it results in higher profits, due to which higher “Tax Liabilities” incur . It can result in increased cash out flows in relation to tax charges.

Why does FIFO show increased gross and net profits?

This is because the “cost of sales” consists of figure of inventory and as first inventories will have less cost than recent inventories during inflation, the profits reported would be higher.

Is FIFO a measure of hyperinflation?

FIFO may not be a suitable measure in times of “hyper inflation”. In such times there exist no reasonable pattern of inflation and prices of goods could inflate drastically.

What is the FIFO method?

As FIFO method assumes inventory first to be received will be the first to be applied in production therefore, cheaper material will be used in production. Because of this cost of production (or simply cost of sales) will decrease and relatively expensive material will be held as closing stock and thus value of closing stock will increase.

What is FIFO in accounting?

FIFO – First in First out is one of the many different ways to value inventory for reporting purposes. It is one of different cost flow assumptions according to which inventory units that are received first by the entity will be the first ones to be sent to production hall for processing or consumption i.e.

FIFO vs. LIFO

- To reiterate, FIFO expenses the oldest inventories first. In the following example, we will compare FIFO to LIFO (last in first out)Last-In First-Out (LIFO)The Last-in First-out (LIFO) method of inventory valuation is based on the practice of assets produced or acquired last being the first to be. LIFO expenses the most recent costs first. Consider the same example above. Recall that un…

Impact of FIFO Inventory valuation Method on Financial Statements

- Recall the comparison example of First-In First-Out and LIFO. The two methods yield different inventory and COGS. Now it is important to consider the impact of using FIFO on a company’s financial statements?

Key Takeaways from First-In First-Out

- FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold.

- It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system.

- FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold.

- It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system.

- It provides a poor matching of revenue with expenses.

Related Reading

- CFI is a global provider of financial analyst training and career advancement for finance professionals, including the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll t…

What Is The FIFO Method?

- FIFO stands for first in, first out, an easy-to-understand inventory valuation methodthat assumes that goods purchased or produced first are sold first. In theory, this means the oldest inventory gets shipped out to customers before newer inventory. To calculate the value of ending inventory, the cost of goods sold (COGS) of the oldest inventory is...

What’s The Difference Between FIFO vs. LIFO?

- LIFO stands for last in, first out, which assumes goods purchased or produced last are sold first (and the inventory that was most recently purchased will be sent to customers before the oldest inventory). It is an alternative valuation method and is only legally used by US-based businesses. FIFO, on the other hand, is the most common inventory valuation method in most countries, acc…

What Method of Inventory Management Should You use?

- Of course, you should consult with an accountant but the FIFO method is often recommended for inventory valuation purposes. If you sell a product that requires fulfilling older inventory first for quality purposes (especially if you sell perishables and other types of time-sensitive goods), the FIFO method will follow the natural flow of inventory, providing accurate numbers. For retailers d…

Leave Inventory Management to The Pros

- ShipBob’s tech-enabled retail fulfillment solution is designed for fast-growing B2B ecommerce and direct-to-consumer brands. For inventory tracking purposes and accurate fulfillment, ShipBob uses a lot tracking system that includes a lot feature, allowing you to separate items based on their lot numbers. When you send us a lot item, it will not be sold with other non-lot items, or oth…