To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO

FIFO and LIFO accounting

FIFO and LIFO accounting are methods used in managing inventory and financial matters involving the amount of money a company has tied up within inventory of produced goods, raw materials, parts, components, or feed stocks. They are used to manage assumptions of cost flows related to inventory, stock repurchases (if purchased at different prices), and various other accounting purposes.

How to determine the value of inventory using FIFO?

Calculate the value of the inventory sold during the period. Using FIFO, list the beginning inventory and the first shipments of inventory as being sold first. Using the earlier example with 60 ...

Which is a better method LIFO or FIFO?

FIFO assumes that cheaper items are sold first, generating a higher profit than LIFO. However, when the more expensive items are sold in later months, profit is lower. LIFO generates lower profits in early periods and more profit in later months. FIFO is the easier method to use, and most businesses stick with the FIFO method.

What is FIFO inventory costing and why use it?

It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company’s inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation. How Do You Calculate FIFO? What Are the Advantages of FIFO?

Which inventory method is best for tax purposes?

- Cost. Simply value the item at your purchase price plus any shipping fees etc.

- Lower of cost or market. You would compare the cost of each item with the market value on a specific valuation date each year.

- Retail. You would add the retail value (i.e. your selling price) and then subtract a set mark-up percentage to determine the cost.

What is FIFO method with example?

Example of FIFO Imagine if a company purchased 100 items for $10 each, then later purchased 100 more items for $15 each. Then, the company sold 60 items. Under the FIFO method, the cost of goods sold for each of the 60 items is $10/unit because the first goods purchased are the first goods sold.

What is the FIFO procedure?

FIFO is “first in first out” and simply means you need to label your food with the dates you store them, and put the older foods in front or on top so that you use them first. This system allows you to find your food quicker and use them more efficiently.

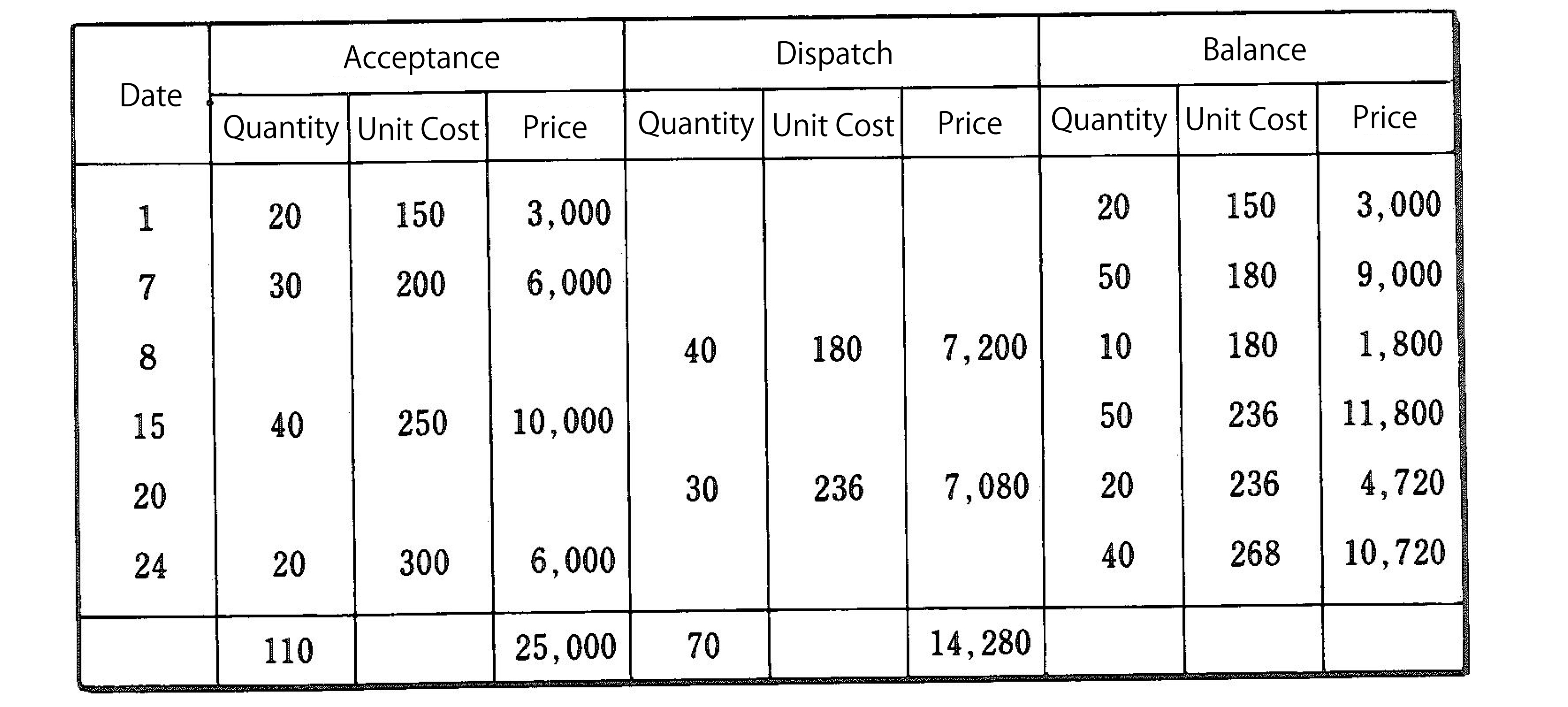

How do you calculate FIFO perpetual inventory?

6:567:50Inventory costing - FIFO, Perpetual - YouTubeYouTubeStart of suggested clipEnd of suggested clipSo we have six hundred units sitting in inventory. And their total cost would be three thousandMoreSo we have six hundred units sitting in inventory. And their total cost would be three thousand dollars and that's the amount that would show up on the balance sheet under our inventory.

How does FIFO costing work?

What is FIFO costing? In simplest terms, FIFO (first-in, first-out) costing allows you to track the cost of an item/SKU based on its cost at purchase order receipt, and apply this cost against each shipment of the item until the receipt quantity is exhausted.

Why is FIFO the best method?

FIFO is more likely to give accurate results. This is because calculating profit from stock is more straightforward, meaning your financial statements are easy to update, as well as saving both time and money. It also means that old stock does not get re-counted or left for so long it becomes unusable.

Where do you use FIFO method in distribution?

The FIFO method applies to both warehouse management and accounting where it's used as an inventory valuation method. With accurate inventory valuation methods, a company's financial statements reflect reality as accurately as possible.

How do you find cost of goods using FIFO?

With this method, companies add up the total cost of goods purchased or produced during a specified time. This amount is then divided by the number of items the company purchased or produced during that same period. This gives the company an average cost per item.

How do you write a journal entry for FIFO?

1:339:35FIFO Inventory (Part 2) Journal Entries - YouTubeYouTubeStart of suggested clipEnd of suggested clipNow how much was my sale I sold 100 units at $5 each so I'm gonna debit accounts receivable 500. AndMoreNow how much was my sale I sold 100 units at $5 each so I'm gonna debit accounts receivable 500. And I'm gonna credit sales 500. I remember debits and credits always have to balance.

What is LIFO and FIFO with example?

First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method. Last-in, first-out (LIFO) assumes the last inventory added will be the first sold. Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

How do you maintain FIFO in retail?

First-in, first-out (FIFO) The FIFO stock control method is when a retailer fulfills an order with the item that has been sitting on the shelf the longest. Basically, the products that were acquired first will also be the first products that you sell. Generally, FIFO leads to higher profits.Apr 23, 2018Inventory Management Techniques | How to Manage Retail Stock - Vendhttps://www.vendhq.com › blog › inventory-management...https://www.vendhq.com › blog › inventory-management...Search for: How do you maintain FIFO in retail?

What is FIFO expense?

FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold. It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system. It provides a poor matching of revenue with expenses.

What is the benefit of using FIFO?

1. Better valuation of inventory . By using FIFO, the balance sheet shows a better approximation of the market value of inventory. The latest costs for manufacturing or acquiring the inventory are reflected in inventory, and therefore, the balance sheet reflects the approximate current market value.

What is the term for the days required for a business to receive inventory, sell the inventory, and collect cash from

It considers the cost of goods sold, relative to its average inventory for a year or in any a set period of time. Operating Cycle. Operating Cycle An Operating Cycle (OC) refers to the days required for a business to receive inventory, sell the inventory, and collect cash from the sale.

Can you use LIFO in Canada?

Therefore, we can see that the balances for COGS and inventory depend on the inventory valuation method. For income tax purposes in Canada, companies are not permitted to use LIFO. However, US companies are able to use FIFO or LIFO.

Why is FIFO accounting used?

FIFO method of accounting saves time, and money spends in calculating the exact inventory cost that is being sold because the recording of inventory is done in the same order as they are purchased or produced. Easy to understand.

What are the disadvantages of FIFO accounting?

One of the biggest disadvantages of FIFO accounting method is inventory valuation during inflation, First In First Out method will result in higher profits, and thus will results in higher “Tax Liabilities” in that particular period. This may result in increased tax charges and higher tax-related cash outflows.

Which method of inventory valuation gives the most accurate calculation of the inventory and sales profit?

A business which is in the trading of perishable items generally sells the items which are purchased earliest first, FIFO method of inventory valuation generally gives the most accurate calculation of the inventory and sales profit. Other examples include retail businesses that sell foods or other products with an expiration date.

How are inventory costs reported?

Inventory costs are reported either on the balance sheet, or they are transferred to the income statement as an expense to match against sales revenue. When inventories are used up in production or are sold, their cost is transferred from the balance sheet to the income statement as cost of goods sold.

Is the first in first out method a good measure of inventory?

Use of First In First Out method is not a suitable measure of inventory in times of “ hyperinflation .”. During such times, there is no particular pattern of inflation, which may result in prices of goods to inflate drastically.

Does inflation increase operating expenses?

Normally in an inflationary environment, prices are always rising, which will cause an increase in operating expenses, but with FIFO accounting, the same inflation will cause an increase in ending inventory.

How does FIFO work?

Before kicking back and relaxing, she wants to figure out what her net income was for the trade show. To do this, Bertie uses the FIFO method ...

What is FIFO in real life?

What is First In, First Out (FIFO)? First In, First Out is a method of inventory valuation where you assume you sold the oldest inventory you own first. It’s so widely used because of how much it reflects the way things work in real life, like your local coffee shop selling its oldest beans first to always keep the stock fresh.

How does inventory valuation affect financial statements?

Your inventory valuation method will affect two key financial statements: the income statement and balance sheet. If your inventory costs are increasing over time, using the FIFO method and assuming you’re selling the oldest inventory first will mean counting the cheapest inventory first. This will reduce your Cost of Goods Sold, ...

What does Bertie want to know about her inventory?

Bertie also wants to know the value of her remaining inventory —she wants her balance sheet to be accurate. To do this, she counts up the value of her remaining inventory.

What is the opposite of FIFO?

The opposite to FIFO, is LIFO which is when you assume you sell the most recent inventory first. This is favored by businesses with increasing inventory costs as a way of keeping their Cost of Goods Sold high and their taxable income low.

How much is Bertie's ending inventory?

Bertie’s ending inventory = $450. Bertie had 300 bars left over—the same amount she sold. But when using the first in, first out method, Bertie’s ending inventory value is higher than her Cost of Goods Sold from the trade show. This is because her newest inventory cost more than her oldest inventory.

How to find average cost?

The average cost is found by dividing the total cost of inventory by the total count of inventory.

Modify the cost and initial quantity of an item

Entering the incorrect cost and initial quantity of the item during the initial set up will result in an incorrect value in the inventory asset account. To correct this:

Sign in for the best experience

Ask questions, get answers, and join our large community of QuickBooks users.

What is FIFO accounting?

That being said, FIFO is primarily an accounting method for assigning costs to your goods sold. So you don’t necessarily have to actually sell your oldest products first—you just account for the cost of goods sold using the oldest numbers. In other words, when determining your business’s cost of goods sold (COGS), ...

What is the FIFO method?

Short for first in, first out, the FIFO method is a popular strategy for fulfilling customer orders and assigning costs to your sold inventory for accounting purposes. The first in, first out (or FIFO) method is a strategy for assigning costs to goods sold. Essentially, it means your business sells the oldest items in your inventory first—at least ...

What is the first in first out method?

The first in, first out (or FIFO) method is a strategy for assigning costs to goods sold. Essentially, it means your business sells the oldest items in your inventory first—at least on paper, anyway. FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual ...

Why is FIFO used?

FIFO is probably the most commonly used method among businesses because it’s easy and it provides greater transparency into your company’s actual financial health. Here’s everything you need to know to decide if the FIFO method is right for you.

Is FIFO better than LIFO?

FIFO is also more transparent and easier to use than LIFO. LIFO systems are easy to manipulate to make it look like your business is doing better than it is. But a FIFO system provides a more accurate reflection of the current value of your inventory. This is one of the reasons why the International Financial Reporting Standards (IFRS) Foundation requires businesses to use FIFO.

What are some examples of FIFO?

We can apply this approach to unique items with a particular cost. Some examples can be antiquities, jewelry, paintings, and others.

Why do investors prefer FIFO?

Investors and financial institutions prefer FIFO as it’s a transparent approach to the Cost of Goods Sold’s calculation. It is easier to manage and allows the company to declare more profit. The First In, First Out method also presents a more accurate ending balance of the remaining inventory.

What are the drawbacks of FIFO?

In normal circumstances, where the markets experience inflation, FIFO results in a higher gap between selling prices and cost. Due to this, the company experiences higher income tax than other methods. If there’s abnormal inflation or rising prices, the technique can overstate profit and inflate inventory balances.

What happens when you apply FIFO?

The method will use the older costs, which are priced lower than the most recent ones. Doing so will result in a higher net income. Also, newer, more expensive items will remain on the Balance Sheet, inflating the inventory’s ending balance.

When we apply LIFO, what happens to the last items we acquire?

When we apply LIFO, the last items we acquire are the ones we use first. LIFO will produce lower net income and a lower ending balance of inventory in the premise of inflation.

What is the first in first out method?

The First In, First Out method has some benefits. It is easy to understand, well-known, and trusted by professionals. FIFO follows the actual inventory flow, and it provides for easier bookkeeping and is less prone to mistakes.

What is FIFO in accounting?

The First-In, First-Out (FIFO) method assumes that the first unit making its way into inventory–or the oldest inventory–is the sold first. For example, let's say that a bakery produces 200 loaves of bread on Monday at a cost of $1 each, and 200 more on Tuesday at $1.25 each. FIFO states that if the bakery sold 200 loaves on Wednesday, the COGS ( on the income statement) is $1 per loaf because that was the cost of each of the first loaves in inventory. The $1.25 loaves would be allocated to ending inventory ( on the balance sheet ).

When sales are recorded using the FIFO method, what is the oldest inventory?

When sales are recorded using the FIFO method, the oldest inventory–that was acquired first–is used up first. FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet.

Why is LIFO not accurate?

As a result, LIFO doesn't provide an accurate or up-to-date value of inventory because the valuation is much lower than inventory items at today's prices.

Why would COGS be higher under LIFO?

In an inflationary environment, the current COGS would be higher under LIFO because the new inventory would be more expensive. As a result, the company would record lower profits or net income for the period. However, the reduced profit or earnings means the company would benefit from a lower tax liability.

Why is FIFO better than COGS?

FIFO can be a better indicator of the value for ending inventory because the older items have been used up while the most recently acquired items reflect current market prices. For most companies, FIFO is the most logical choice since they typically use their oldest inventory first in the production of their goods, which means the valuation of COGS reflects their production schedule.

What is LIFO method?

LIFO. When sales are recorded using the LIFO method, the most recent items of inventory are used to value COGS and are sold first. In other words, the older inventory, which was cheaper, would be sold later.

How does inventory accounting work?

Inventory accounting assigns values to the goods in each production stage and classifies them as company assets, as inventory can be sold, thus turning it into cash in the near future. Assets need to be accurately valued so that the company as a whole can be accurately valued. The formula for calculating inventory is:

What does FIFO mean in accounting?

FIFO is an acronym. It stands for “First-In, First-Out” and is used for cost flow assumption purposes. Cost flow assumptions refers to the method of moving the cost of a company’s product out of its inventory to its cost of goods sold. Inventory refers to:

Why use LIFO or FIFO?

The LIFO method for financial accounting may be used over FIFO when the cost of inventory is increasing, perhaps due to inflation. Using FIFO means the cost of a sale will be higher because the more expensive items in inventory are being sold off first.

What is the difference between FIFO and LIFO?

The FIFO (“First-In, First-Out”) method means that the cost of a company’s oldest inventory is used in the COGS (Cost of Goods Sold) calculation. LIFO (“Last-In, First-Out”) means that the cost of a company’s most recent inventory is used instead. Here’s What We’ll Cover:

When calculating COGS, what is the company going to go by?

Therefore, when calculating COGS (Cost of Goods Sold), the company will go by those specific inventory costs. Although the oldest inventory may not always be the first sold, the FIFO method is not actually linked to the tracking of physical inventory, just inventory totals. However, FIFO makes this assumption in order for ...

Why Value Inventory?

Inventory Costing Explained

- The calculation of inventory cost is an important part of filing your business tax return. Like other legitimate business costs, the cost of the products you buy to resell can be deducted from your business income to reduce your taxes. At the beginning of the year, you have an initial inventory of products in various stages of completion or ready to be sold. During the year, you buy more inve…

Other Costing Methods

- Instead of using FIFO, some businesses use one of these other inventory costing methods: 1. Specific identificationis used when specific items can be identified. For example, the cost of antiques or collectibles, fine jewelry, or furs can be determined individually, usually through appraisals. 2. LIFO costing ("last-in, first-out") considers the last produced products as being tho…

Example of First-In, First-Out

FIFO vs. LIFO

- To reiterate, FIFO expenses the oldest inventories first. In the following example, we will compare FIFO to LIFO (last in first out)Last-In First-Out (LIFO)The Last-in First-out (LIFO) method of inventory valuation is based on the practice of assets produced or acquired last being the first to be. LIFO expenses the most recent costs first. Consider the same example above. Recall that un…

Impact of FIFO Inventory valuation Method on Financial Statements

- Recall the comparison example of First-In First-Out and LIFO. The two methods yield different inventory and COGS. Now it is important to consider the impact of using FIFO on a company’s financial statements?

Key Takeaways from First-In First-Out

- FIFO expenses the oldest costs first. In other words, the inventory purchased first (first-in) is first to be expensed (first-out) to the cost of goods sold.

- It provides a better valuation of inventory on the balance sheet, as compared to the LIFO inventory system.

- It provides a poor matching of revenue with expenses.

Related Reading

- CFI is a global provider of financial analyst training and career advancement for finance professionals, including the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll t…