If prices are increasing, under FIFO you're going to have a lower cost of goods sold than under LIFO, meaning higher gross margin, higher income taxes and likely higher net income. Assets on the balance sheet will be higher because you'd be keeping the higher cost items and assuming you sold the lower cost items.

Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

How do companies report switching from LIFO to FIFO?

Your Top Offers

- FIFO vs. LIFO. ...

- Retrospective vs. Prospective. ...

- Change in Inventory Valuation Method Disclosure Requirements. Financial statements are required to disclose all significant changes in accounting policies. ...

- Federal Tax Changes. ...

Which is a better method LIFO or FIFO?

FIFO assumes that cheaper items are sold first, generating a higher profit than LIFO. However, when the more expensive items are sold in later months, profit is lower. LIFO generates lower profits in early periods and more profit in later months. FIFO is the easier method to use, and most businesses stick with the FIFO method.

How would FIFO and LIFO affect the income taxes paid?

The main difference between LIFO and FIFO is based on the assertion that the most recent inventory purchased is usually the most expensive. If that assertion is accurate, using LIFO will result in a higher cost of goods sold and less profit, which also directly affects the amount of taxes you’ll have to pay. What is LIFO?

How does LIFO and FIFO affect financial statements?

Financial Statement Impact of LIFO-to-FIFO Switch The inventory's purchase price is the key determining factor on the LIFO-to-FIFO switch's impact on a financial statement. In times of cost increases, LIFO will result in a higher cost-of-goods expense, but lower end-of-period inventory values.

What happens when you switch from LIFO to FIFO?

A change from LIFO to FIFO typically would increase inventory and, for both tax and financial reporting purposes, income for the year or years the adjustment is made.

How is a change from FIFO to LIFO accounted for by a company?

FIFO assumes the opposite. Under LIFO, cost of goods sold is higher, which reduces net income. Under FIFO, cost of goods sold is lower, thereby making net income higher. The tax code allows a company to use LIFO to report taxable income even though it uses FIFO to calculate its accounting profit.

How does LIFO affect the balance sheet and income statement?

LIFO results in lower inventory costs on the balance sheet because the latest, higher costs were removed from inventory ahead of the older lower costs. LIFO means that the cost of goods sold on the income statement will contain the higher most recent costs.

How does LIFO and FIFO affect cost of goods sold?

Decreasing Inventory Costs As for declining inventory costs, the impacts of FIFO vs LIFO are: If Inventory Costs Decreased ➝ Higher COGS Under FIFO (Lower Net Income) If Inventory Costs Decreased ➝ Lower COGS Under LIFO (Higher Net Income)

What is the effect of using FIFO during a period of rising prices under a perpetual inventory system?

What is the effect of using FIFO during a period of rising prices under a perpetual inventory system? - In periods of rising prices, the FIFO method of inventory valuation will give the lowest cost of goods sold as you are 'selling' the older, lower-priced goods first.

Is change from LIFO to FIFO retrospective?

Under U.S. GAAP, retrospective adjustments are NOT made to the financial statements if a company is changing inventory method: A. From LIFO to FIFO.

Why would a company switch to the LIFO method of inventory valuation?

Why would a company switch to the LIFO method of inventory valuation? (a) By switching to LIFO, reported earnings will be higher.

Does GAAP prefer LIFO or FIFO?

There are no GAAP or IFRS restrictions on the use of FIFO in reporting financial results. IFRS does not all the use of the LIFO method at all. The IRS allows the use of LIFO, but if you use it for any subsidiary, you must also use it for all parts of the reporting entity.

How does FIFO affect the income statement?

FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet. As a result, FIFO can increase net income because inventory that might be several years old–which was acquired for a lower cost–is used to value COGS.

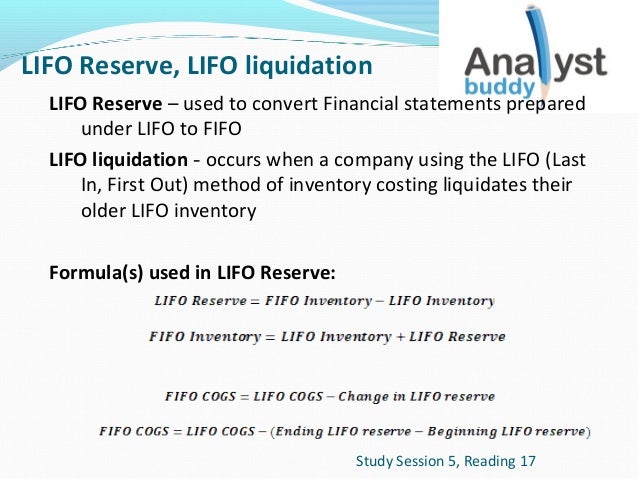

How is LIFO reserve presented in the financial statements?

When preparing company financials for the LIFO method, the difference in costs in inventory between LIFO and FIFO is the LIFO reserve. Therefore, a company's LIFO reserve = (FIFO inventory) - (LIFO inventory).

Can you use LIFO for tax purposes and FIFO for financial reporting purposes?

LIFO could be used for U.S. income tax purposes, while FIFO is used for financial reporting.

conversion from LIFO to FIFO Definition

Conversion from LIFO to FIFO is a process by which the financial statements of an entity that uses the LIFO method can be converted into the financial statements that would be prepared using the FIFO method.

Overview of Conversion from LIFO to FIFO

A business that deals in goods must maintain an inventory of raw materials and the inventory of finished goods. The business must keep a stock of finished goods to fulfill the increases in demand of the customers. Although, a very high amount of inventory may harm the business if any unfortunate event occurs.

LIFO & FIFO

The inventory valuation method chosen by a company has a significant impact on its financial statements, such as balance sheets and income statements. The generally accepted accounting principles allow a business to use any of three methods to evaluate inventory.

Procedure Of Conversion

The financial statements of an entity reported as per the LIFO method are converted into the FIFO method by using the following steps:

Example for LIFO to FIFO Conversion

An Ltd prepares the financial statements as per the LIFO method. The following elements are extracted from the financial statements of An Ltd. The applicable tax rate is 40%.

What is LIFO compared to FIFO?

During periods of significantly increasing costs, LIFO when compared to FIFO will cause lower inventory costs on the balance sheet and a higher cost of goods sold on the income statement. This will mean that the profitability ratios will be smaller under LIFO than FIFO.

Why is inventory turnover ratio higher under LIFO?

The inventory turnover ratio will be higher when LIFO is used during periods of increasing costs. The reason is that the cost of goods sold will be higher and the inventory costs will be lower under LIFO than under FIFO.

What is LIFO method?

LIFO. When sales are recorded using the LIFO method, the most recent items of inventory are used to value COGS and are sold first. In other words, the older inventory, which was cheaper, would be sold later.

What is FIFO in accounting?

The First-In, First-Out (FIFO) method assumes that the first unit making its way into inventory–or the oldest inventory–is the sold first. For example, let's say that a bakery produces 200 loaves of bread on Monday at a cost of $1 each, and 200 more on Tuesday at $1.25 each. FIFO states that if the bakery sold 200 loaves on Wednesday, the COGS ( on the income statement) is $1 per loaf because that was the cost of each of the first loaves in inventory. The $1.25 loaves would be allocated to ending inventory ( on the balance sheet ).

What would happen if inflation was nonexistent?

If inflation were nonexistent, then all three of the inventory valuation methods would produce the same exact results. Inflation is a measure of the rate of price increases in an economy. When prices are stable, our bakery example from earlier would be able to produce all of its bread loaves at $1, and LIFO, FIFO, and average cost would give us a cost of $1 per loaf. However, in the real world, prices tend to rise over the long term, which means that the choice of accounting method can affect the inventory valuation and profitability for the period. 1

Why is LIFO not accurate?

As a result, LIFO doesn't provide an accurate or up-to-date value of inventory because the valuation is much lower than inventory items at today's prices.

Why would COGS be higher under LIFO?

In an inflationary environment, the current COGS would be higher under LIFO because the new inventory would be more expensive. As a result, the company would record lower profits or net income for the period. However, the reduced profit or earnings means the company would benefit from a lower tax liability.

Why is FIFO better than COGS?

FIFO can be a better indicator of the value for ending inventory because the older items have been used up while the most recently acquired items reflect current market prices. For most companies, FIFO is the most logical choice since they typically use their oldest inventory first in the production of their goods, which means the valuation of COGS reflects their production schedule.

When sales are recorded using the FIFO method, what is the oldest inventory?

When sales are recorded using the FIFO method, the oldest inventory–that was acquired first–is used up first. FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet.

What is FIFO in accounting?

FIFO and LIFO represent accounting methods that determine the value of a company's unsold inventory, cost of goods sold and other transactions. Under FIFO, companies attribute the cost of their oldest goods to their newest sales. The opposite is true under LIFO: The cost of the newest goods is attributed to the newest sales. In periods of rising prices, or inflation, FIFO offers the lowest cost of goods sold and the highest reported profits. In periods of falling prices, or deflation, LIFO results in the highest reported profits.

Why do companies use FIFO?

While most companies stick with FIFO or LIFO for consistency, sometimes the owners change their minds. When they do, companies must comply with special reporting requirements to keep their investors informed.

Why do companies need to provide footnotes?

The company must provide footnotes to explain why it was impractical to restate its historical financial statements. Generally speaking, records are usually easier to obtain when switching from LIFO to FIFO than the other way around.

How does the income statement affect the cash flow statement?

The income statement is affected from changes in cost of goods sold, and this affects all measures of earnings, such as operating income and net income. The balance sheet is also affected from changes in inventory valuations. All of these changes trickle down to impact the cash flow statement.

Do private companies have to follow GAAP?

Private companies often follow GAAP reporting, though they're not obligated to, because investors and lenders are trained to evaluate GAAP information and demand it from companies. If a private company is making the switch from LIFO to FIFO, its owners will probably want to explain it to stakeholders.