Why should you use LIFO over FIFO?

One final reason to use LIFO over FIFO is that there are fewer inventory write-downs under LIFO during inflation. An inventory write-down occurs when the inventory is deemed to have decreased in price below its carrying value.

Should I use FIFO or standard cost?

FIFO can impact cost but mainly serves to ensure inventory age is minimized assuming you are tracking lot cost. The lot cost impacts average cost or creates purchase price variances to standard cost. Given our experience I would almost always recommend standard cost unless there are few items and manageable transaction volumes.

What are the alternatives to FIFO?

Alternatives to FIFO. The inventory valuation method opposite to FIFO is LIFO, where the last item in is the first item out. In inflationary economies, this results in deflated net income costs and lower ending balances in inventory when compared to FIFO. The average cost inventory method assigns the same cost to each item.

What happens to LCM reserves when FIFO increases?

Even if a LCM reserve may exceed the first year LIFO reserve, the LIFO reserve will grow with continued inflation regardless of FIFO value increases and this is not true of LCM reserves. LCM reserves must be taken into income when LIFO is adopted as a Section 481 (a) adjustment but this is spread over 3 years.

Can a company use both LIFO and FIFO?

The U.S. accounting standards organization, the Financial Accounting Standards Board (FASB), in its Generally Accepted Accounting Procedures, allows both FIFO and LIFO accounting.

Can LCM be used with FIFO?

Like firms that adopt the LIFO method, firms using the FIFO approach can also value their goods at cost. But firms that use the FIFO approach have still another choice—the “lower of cost or market” (LCM) method.

When should you not use FIFO?

1: Batch Processing If you are moving or processing your parts in boxes or batches, then it will be difficult to maintain a FiFo within the box. It is possible using some creative numbering scheme, but unless there is a compelling reason to do so, the effort is not worth the benefit.

Why would you use FIFO over LIFO?

Key takeaway: FIFO and LIFO allow businesses to calculate COGS differently. From a tax perspective, FIFO is more advantageous for businesses with steady product prices, while LIFO is better for businesses with rising product prices.

When the lower of cost or market LCM rule requires an inventory adjustment?

The lower of cost or market rule states that a business must record the cost of inventory at whichever cost is lower – the original cost or its current market price. This situation typically arises when inventory has deteriorated, or has become obsolete, or market prices have declined.

What is the Lcnrv rule?

Generally accepted accounting principles require that inventory be valued at the lesser amount of its laid-down cost and the amount for which it can likely be sold — its net realizable value (NRV). This concept is known as the lower of cost and net realizable value, or LCNRV.

What happens if you don't follow FIFO?

If you don't follow FIFO or LIFO methods, then another inventory valuation method has to be applied: Weighted average method, Moving average method are other valuation methods that can be used.

Is it better to sell stock FIFO or LIFO?

FIFO vs LIFO Stock Trades Under FIFO, if you sell shares of a company that you've bought on multiple occasions, you always sell your oldest shares first. FIFO stock trades results in the lower tax burden if you bought the older shares at a higher price than the newer shares.

What are the limitations of FIFO?

The first-in, first-out (FIFO) accounting method has two key disadvantages. It tends to overstate gross margin, particularly during periods of high inflation, which creates misleading financial statements. Costs seem lower than they actually are, and gains seem higher than they actually are.

Can you switch from FIFO to LIFO?

Therefore, switching from FIFO to LIFO can have a significant impact on all financial statements. A business switching from FIFO to LIFO will need to consider whether it needs to restate its financial data for prior years to reflect the new method or only apply the new method to the current and future years.

Why is LIFO not allowed?

IFRS prohibits LIFO due to potential distortions it may have on a company's profitability and financial statements. For example, LIFO can understate a company's earnings for the purposes of keeping taxable income low. It can also result in inventory valuations that are outdated and obsolete.

Why don t more companies use LIFO?

Opponents of LIFO say that it distorts inventory figures on the balance sheet in times of high inflation. They also point out that LIFO gives its users an unfair tax break because it can lower net income, and subsequently, lower the taxes a firm faces.

What is FIFO method?

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

What is FIFO accounting?

First In, First Out (FIFO) is an accounting method in which assets purchased or acquired first are disposed of first. FIFO assumes that the remaining inventory consists of items purchased last. An alternative to FIFO, LIFO is an accounting method in which assets purchased or acquired last are disposed of first.

What Are the Advantages of First In, First Out (FIFO)?

The obvious advantage of FIFO is that it's the most widely used method of valuing inventory globally. It is also the most accurate method of aligning the expected cost flow with the actual flow of goods which offers businesses a truer picture of inventory costs . Furthermore, it reduces the impact of inflation, a ssuming that the cost of purchas ing newer inventory will be higher than the purchasing cost of older invent ory. Finally, it reduces the obsolescence of inventory.

What is FIFO in manufacturing?

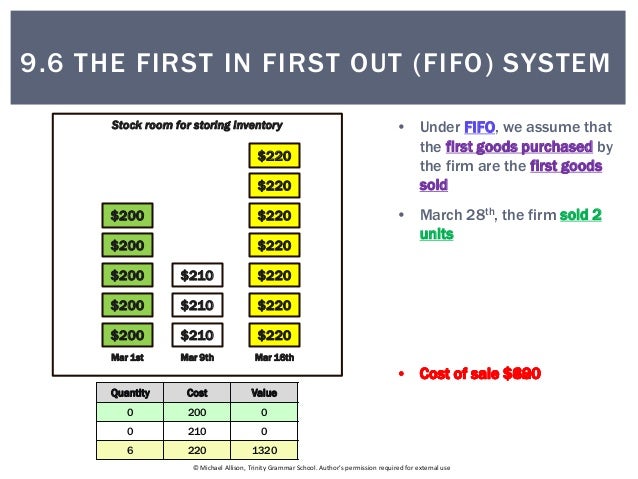

The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense. Under FIFO, it is assumed that the cost of inventory purchased first will be recognized first. The dollar value of total inventory decreases in this process because inventory has been removed from the company’s ownership. The costs associated with the inventory may be calculated in several ways — one being the FIFO method.

What happens when FIFO assigns the oldest costs to the cost of goods sold?

In this situation, if FIFO assigns the oldest costs to the cost of goods sold, these oldest costs will theoretically be priced lower than the most recent inventory purchased at current inflated prices. This lower expense results in higher net income. Also, because the newest inventory was purchased at generally higher prices, the ending inventory balance is inflated.

Why do firms use LIFO?

The main argument for this option is that it would align tax accounting rules with the way businesses tend to sell their goods. Under many circumstances, firms prefer to sell their oldest inventory first to minimize the risk that the products will become obsolete or damaged while in storage. In such cases, allowing firms to use alternative approaches to identify and value their inventories for tax purposes allows them to reduce their tax liabilities without changing their economic behavior. Under the LIFO approach, companies defer taxes on real (inflation-adjusted) gains when the prices of their goods are rising relative to general prices. Firms that use the LIFO approach can value items sold out of inventory on the basis of costs associated with newer—and more expensive—items when, in fact, the actual items sold may have been acquired or produced at a lower cost at some point in the past. By deducting those higher costs as the cost of production, firms can defer paying taxes on the amount their goods have appreciated until those goods are sold.

How does LCM work in inventory accounting?

Another argument for this option is that the LCM and subnormal-goods methods of inventory accounting treat losses and gains asymmetrically by allowing firms to immediately recognize losses in the value of inventory but not requiring them to recognize gains. The LCM method will reduce the value of a business's year-end inventory if the market value of any item in the inventory is less than its assigned cost. Similarly, the subnormal-goods method of inventory valuation allows firms to immediately deduct the loss in a good's value, lowering the value of their year-end inventory. In either case, that lower value increases the deduction for the cost of goods sold and reduces taxable income. In effect, those methods allow firms to immediately deduct from taxable income the losses they incur from the decline in the value of their inventory without requiring them to include gains in the value of their inventory in taxable income.

What is the LCM method of inventory valuation?

Firms that do not use the LIFO approach to assign costs can value inventory using the "lower of cost or market" (LCM) method. The LCM method allows firms to use the current market value of an item (that is, the current-year cost to reproduce or repurchase it) in their calculation of year-end inventory values if that market value is less than the cost assigned to the item. In addition, businesses can qualify for the "subnormal goods" method of inventory valuation, which allows a company to value inventory below cost if its goods cannot be sold at cost because they are damaged or flawed.

Why is the estimate for this option uncertain?

The estimate for this option is uncertain because it relies on the Congressional Budget Office's 10-year projections of corporate profits, investment, and inflation, which are inherently uncertain. In addition to those economic factors, the estimate depends on projections of firms' choices of inventory-valuation approaches. Those choices are also uncertain.

What is the other costing method?

The other costing method are a compromise between those two extremes, Think about he business decisions you face with regard to inventory costs and that will help you decide.

Do costing methods work ok?

If costs are stable and inventory is largely consumed and accounted in the same month then any costing methods work ok in general you might as well use the one that you understand and that has the least performance hit. How many items and orders you have, and the complexity of your boms , how seasonal and erratic is demand, exchange rates etc may force a pragmatic decision of what is most workable.

Can you have both FIFO & Standard costing methods?

Many accountants with whom I discuss seem to have only have book knowledge of costing and have often only been trained on, or had experience with, average costing. They then write the accounting standards so it becomes a loop. I say that because they say stupid thing like your get different profit margin with average and standard. However, profit is sell price - buy price so how you cost in between has no impact.

Why do companies use LIFO?

A final reason that companies elect to use LIFO is that there are fewer inventory write-downs under LIFO during times of inflation. An inventory write-down occurs when the inventory is deemed to have decreased in price below its carrying value .

How does LIFO work?

How Last in, First out (LIFO) Works. Under LIFO, a business records its newest products and inventory as the first items sold. The opposite method is FIFO, where the oldest inventory is recorded as the first sold. While the business may not be literally selling the newest or oldest inventory, it uses this assumption for cost accounting purposes.

Why is LIFO so controversial?

The higher COGS under LIFO decreases net profits and thu s creates a lower tax bill for One Cup. This is why LIFO is controversial; opponents argue that during times of inflation, LIFO grants an unfair tax holiday for companies. In response, proponents claim that any tax savings experienced by the firm are reinvested and are of no real consequence to the economy. Furthermore, proponents argue that a firm's tax bill when operating under FIFO is unfair (as a result of inflation).

Why is LIFO used?

When prices are rising, it can be advantageous for companies to use LIFO because they can take advantage of lower taxes. Many companies that have large inventories use LIFO, such as retailers or automobile dealerships.

What is LIFO for businesses?

Businesses that sell products that rise in price every year benefit from using LIFO. When prices are rising, a business that uses LIFO can better match their revenues to their latest costs.

What is the LIFO method?

Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first . This method is banned under the International Financial Reporting Standards ...

Why do supermarkets use LIFO?

For example, many supermarkets and pharmacies use LIFO cost accounting because almost every good they stock experiences inflation. Many convenience stores—especially those that carry fuel and tobacco—elect to use LIFO because the costs of these products have risen substantially over time.

What are the advantages of using the IPIC LIFO method?

Advantages of using the IPIC LIFO method include: Good possibility of greater inflation than internal index method. Manufacturers LIFO inflation should be less volatile than if an internal index method is used. IPIC is a simpler method and less prone to index calculation errors.

What is LIFO PRO?

LIFO-PRO is the only non-auto dealer LIFO calculation software with a menu-driven user interface. There are a number of LIFO calculation Excel templates in use but it is a real stretch to call this software because:

What are the disadvantages of using IPIC?

A disadvantage of using the IPIC method is that once the method is used, it is not an automatic approval change to switch back to an internal index method if an internal index method had been used before the company change to IPIC method. What can be a disadvantage for some manufacturers is the fact that the different index categories published for their products is not granular enough. For example, we have had client that had to use a nonferrous metals PPI code because there is no indexes published for their specific metal for that particular stage of production.

Why is IPIC change important?

A change to the IPIC method provides audit protection which is very important for a substantial number of LIFO taxpayers using bad methods

Why is the LIFO exclusion not in inventory?

specifically prohibit exclusion of items not in inventory the prior year (link-chain) or base year (double-extension) because doing so tends to overstate inflation. The Regs. allows the prior year or base year index to be set equal to the current year price, but this method understates inflation.

When was LIFO allowed?

This was the only LIFO method allowed by the IRS until 1947 but this method should never be used because of the burdensome record keeping requirements and the fact that the taxable income deferral using this method is only a fraction of the deferral achieved using a dollar-value LIFO method.

Is LIFO a conformity rule?

Yes, the “LIFO conformity rule” which is contained in Reg. § 1.472–2 (e) were amended in 1981 to specifically permit the use of book LIFO methods that are different from IRS Regs. methods. The most common book v. tax LIFO methods difference is companies using the IPIC method for tax purposes and an internal index method for financial reporting purposes.