Both LIFO and FIFO

FIFO

FIFO is an acronym for first in, first out, a method for organising and manipulating a data buffer, where the oldest entry, or 'head' of the queue, is processed first. It is analogous to processing a queue with first-come, first-served behaviour: where the people leave the queue in the order in …

Why would a company have to pick LIFO or FIFO?

Why Would a Company Have to Pick LIFO or FIFO?

- Inventory FIFO. In inventory management, FIFO means that the oldest inventory items -- the ones purchased first -- are sold before newer items.

- Inventory LIFO. Although it is rare, there are companies that have to pick LIFO, rather than FIFO, to manage their inventory.

- Accounting Considerations. ...

- Accounting Alternatives. ...

Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

Which is a better method LIFO or FIFO?

FIFO assumes that cheaper items are sold first, generating a higher profit than LIFO. However, when the more expensive items are sold in later months, profit is lower. LIFO generates lower profits in early periods and more profit in later months. FIFO is the easier method to use, and most businesses stick with the FIFO method.

How to determine which shares to sell, FIFO or LIFO?

How to Determine Which Shares to Sell, FIFO or LIFO

- FIFO vs LIFO Stock Trades. The first-in, first-out method is the default way to decide which shares to sell. ...

- Tell Your Broker. If you plan to use any method besides FIFO, including LIFO, you must specifically direct your broker as to which shares to sell so that your taxes ...

- 2018 Tax Law Changes. ...

- 2017 Tax Law. ...

Is LIFO and FIFO allowed under GAAP?

One of the most basic differences is that GAAP permits the use of all three of the most common methods for inventory accountability—weighted-average cost method; first in, first out (FIFO); and last in, first out (LIFO)—while the IFRS forbids the use of the LIFO method.

Can a company use LIFO for tax and FIFO for book?

Unfortunately, taxpayers are not permitted to simultaneously use LIFO for tax purposes and FIFO for book purposes. In order to recognize the tax breaks provided by LIFO, companies must do two things: (1) begin using LIFO for book purposes, and (2) file for a change in accounting method with the IRS.

What happens when you switch from FIFO to LIFO?

Financial Statement Impact of LIFO-to-FIFO Switch In times of cost increases, LIFO will result in a higher cost-of-goods expense, but lower end-of-period inventory values. However, in times of cost decreases, LIFO will result in a lower cost-of-goods expense, but higher end-of-period inventory values.

Can companies use different inventory valuation methods?

Comparing different inventory valuation methods: FIFO, LIFO, and WAC. Different inventory valuation methods – such as FIFO, LIFO, and WAC – can affect your bottom line in different ways, so it's important to choose the right method for your business.

Why LIFO is not allowed?

IFRS prohibits LIFO due to potential distortions it may have on a company's profitability and financial statements. For example, LIFO can understate a company's earnings for the purposes of keeping taxable income low. It can also result in inventory valuations that are outdated and obsolete.

Can I use LIFO for stock sales?

Yes, you can choose which stocks you sell by giving the proper instructions to your stock broker. The IRS does not prohibit you from choosing the LIFO (last in, first out) method rather than the FIFO method.

Can you use LIFO for crypto and FIFO for stocks?

Using HIFO or LIFO instead of FIFO can help you save money on your tax bill. Still, FIFO is used by most investors since it is considered the most conservative accounting method. HIFO and LIFO should only be used if you've kept detailed records of your crypto transactions.

Do most companies use LIFO or FIFO?

Most companies prefer FIFO to LIFO because there is no valid reason for using recent inventory first, while leaving older inventory to become outdated. This is particularly true if you're selling perishable items or items that can quickly become obsolete.

Why would a company use LIFO instead of FIFO?

During times of rising prices, companies may find it beneficial to use LIFO cost accounting over FIFO. Under LIFO, firms can save on taxes as well as better match their revenue to their latest costs when prices are rising.

Can a business change from one inventory costing method to another any time they wish?

The IRS requires you commit to an inventory cost method the first year your business files its tax return and encourages you to maintain consistency throughout the years. However, the IRS does allow your company to apply to change your inventory cost method.

Do companies have to use the same inventory method for all items of inventory?

The choice is important, and it may be tempting to use different methods for different products. Businesses are required to have consistent inventory valuation methods not only during the current year, but over time as well.

Are companies allowed to use more than one inventory valuation method?

d) Companies are allowed to use more than one inventory valuation method. Companies using IFRS may not reverse entries for inventory write-downs if the market recovers.

What is FIFO in accounting?

FIFO and LIFO are methods used in the cost of goods sold calculation. FIFO (“First-In, First-Out”) assumes that the oldest products in a company’s inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company’s inventory have been sold first ...

What is LIFO reserve?

The LIFO reserve is the amount by which a company’s taxable income has been deferred, as compared to the FIFO method. The remaining unsold 350 televisions will be accounted for in “inventory”.

Why are FIFO profits more accurate?

Although this may mean less tax for a company to pay under LIFO, it also means stated profits with FIFO are much more accurate because older inventory reflects the actual costs of that inventory. If profits are naturally high under FIFO, then the company becomes that much more attractive to investors.

Is LIFO more attractive than FIFO?

You can see how for Ted, the LIFO method may be more attractive than FIFO. This is because the LIFO number reflects a higher inventory cost, meaning less profit and less taxes to pay at tax time. The LIFO reserve in this example is $31,250.

Is LIFO legal in the US?

Under GAAP, LIFO is legal. Outside the United States, LIFO is not permitted as an accounting practice. This is why you’ll see some American companies use the LIFO method on their financial statements, and switch to FIFO for their international operations.

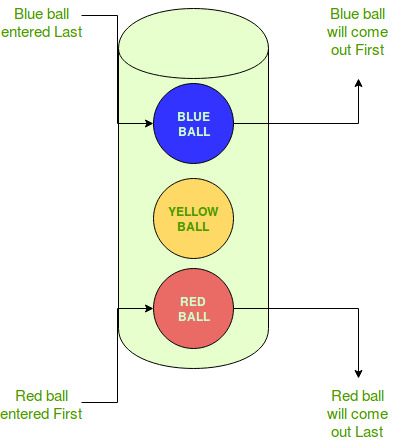

What is a LIFO?

LIFO and FIFO are the two most common inventory methods that are used by a company. The goal is to properly account for cost of purchased inventory on the balance sheet. Generally, a business can calculate its inventory either directly or through profits shown in the income statement and the cash flow statement.

Why is LIFO used?

LIFO is well used in inventory accounting to increase the cost of goods sold by a company. It is also used to reduce net profits, which can then reduce corporate tax liability. So, it is not surprising that LIFO is much more desirable when the corporate tax rate is higher.

What is LIFO in accounting?

LIFO or "last-in, first-out" is a method of accounting for inventory that assumes an inventory unit which is bought first will come out last. It also means that the first unit to be sold is the last inventory that comes into the warehouse. Under LIFO, if there is the last units of inventory purchased were bought at the highest price, ...

What are the advantages of LIFO?

There are several advantages of LIFO for inventory accounting method: 1) Easy to compare current costs with current income, 2) If prices increase then the price of goods becomes conservative, 3) Operating profit is not affected by profit or loss from price fluctuations, 4) More tax savings.

What does FIFO mean in warehouse?

FIFO (First-In, First-Out) As the name suggests, FIFO means the first entry comes out first. This method assumes that the first units to enter warehouse are sold first. So, the oldest items are sold first. This system is usually used by companies with perishable inventory.

Which takes the most investment of funds?

Inventory usually takes the most investment of funds. One way to calculate the profits generated by a company is to track sales revenues and all the costs involved in producing the goods.

Why use FIFO vs LIFO?

FIFO vs. LIFO for flow of goods. Many companies choose to use FIFO because it more closely mimics the actual flow of goods in and out of inventory. It's considered a simpler system with less spoilage and waste of materials.

Why is FIFO higher than LIFO?

Because the cost of goods sold is usually higher under LIFO, this decreases a company's reported profits, which can lower the amount of tax liability. Conversely, FIFO valuations present a higher tax liability because the cost of goods sold is lower. Read more: FIFO Accounting: What It Is and What You Need To Know.

What is a fifo and a fifo?

While both FIFO and LIFO are a way to manage inventory, the marketable goods produced by a company usually dictate which method to choose. FIFO is typically used for perishable products like food and beverages or stock that may become obsolete if it isn't sold within a certain period of time. LIFO however is often used for products that aren't affected by the amount of time spent in inventory or where the flow of product fits the LIFO method.

How is FIFO inventory calculated?

FIFO inventory cost is calculated by determining the cost of the oldest stock and multiplying that amount by the number of items sold.

What is FIFO in inventory?

What is FIFO? First in, first out is a method to value inventory and calculate the cost of goods sold. FIFO items are the oldest products in an inventory because they were the first stock to be added after purchase or production. FIFO uses the principle that when items are acquired first, they are also sold first.

What is LIFO method?

Using the LIFO method, more recent stock can be valued higher than older goods when there is a price increase. LIFO works well using the matching principle, which is used to charge costs along with revenues during the same period of inventory calculations. Read more: A Guide To the Inflation Rate.

What is the last in first out approach?

Last in, first out is another way to manage inventory and calculate profits from goods. In this approach, businesses figure that the most recent inventory is the first sold. This means that older stock continues to sit for longer periods before being sold.

What is FIFO vs LIFO?

FIFO is a more realistic and logical approach of inventory valuation compared to LIFO. There is a risk of stocks, getting obsolete and outdated in case of LIFO, as goods are used from old stock, this risk can be reduced if FIFO is used. Unlike LIFO, record maintenance is easier in FIFO, as several layering is less.

Why use LIFO method?

So ultimately, the benefit of using the LIFO method for a company is that it can report a lower Net Income and hence defer its tax liabilities during the times of high inflation.

What is FIFO in accounting?

FIFO is the globally and widely used method for inventory valuation. While US GAAP allows adopting LIFO as well as FIFO, but in the international scenarios, FIFO is widely used, and IFRS restricts the use of LIFO for inventory valuation. Under LIFO, stock in hand represents the oldest stock, while in FIFO, stock in hand represents the latest stock.

Why is the LIFO method not attractive?

Investment potential. Using the LIFO method may not attract potential investors, as the use of LIFO leads to lower net income. Using the FIFO method helps the investors to understand the current scenario. It helps to attract investors.

What does LIFO mean in stock?

LIFO stands for Last In, First Out, which implies that the inventory which was added last to the stock will be removed from the stock first. So the inventory will leave the stock in an order reverse of that in which it was added to the stock.

What happens if you use LIFO?

If LIFO is used, only old inventory will remain in stock, and its purchase price will have a lesser chance of going below its carrying value. Carrying Value Carrying value is the book value of assets in a company's balance sheet, computed as the original cost less accumulated depreciation/impairments.

Is inventory expensed the same as FIFO?

Hence, whether you use the LIFO method or FIFO method, the value of the inventory expensed or even that in stock will also come out to be the same in any case. But since inflation is a reality, the value of inventory comes out to be something when we use FIFO, and it comes out to be something else when we use LIFO.

What is LIFO for tax reporting?

In normal economic conditions, using LIFO for your tax reporting minimizes your taxable income. If you choose LIFO for taxes and FIFO for financial reporting, you usually report the excess of FIFO inventory over LIFO as your “LIFO reserve.”. To use LIFO for tax reporting, you must file IRS Form 970 in the year you adopt this method.

Is FIFO good for financial reporting?

You have greater gross profits -- sales minus COGS -- under FIFO, as well as higher current assets, which includes inventory. This might be good for financial reporting, as it emphasizes your profitability, but is not so good for tax reporting because it creates higher taxable income.

Can you use gross profit instead of LIFO?

For example, you can assign average costs to your merchandise instead of LIFO or FIFO. In addition, you can adopt the gross profit method to value your inventory for financial reporting, but not for taxes. IRS tax reporting also rules out the combination of the LIFO cost flow assumption and the "lower of cost or market" method for valuing inventory ...

What is the FIFO method?

They can use the first-in, first-out (FIFO) method, the last-in, first-out method (LIFO), or they can calculate inventory costs by using the average cost method. 1 By comparison, companies reporting under International Financial Reporting Standards (IFRS) are required to use FIFO only. 2 . LIFO has been the subject of some budget controversy in ...

Why did Obama ban LIFO?

In 2014, the administration of President Barack Obama sought to ban LIFO, which it said allowed companies to make their incomes appear smaller for the purposes of taxation. 3 Proponents for keeping LIFO say repeal would increase the cost of capital for companies and have negative consequences for economic growth. 4 .

What is FIFO in crypto?

If you don’t have detailed records to meet the Specific ID requirements, you have to use the First in, first out (FIFO) method to calculate your cost basis. This means each time you dispose of your crypto assets, you are presumably disposing of the oldest coin you had in your wallet.

What is HIFO coin?

Highest in, first out (HI FO) is a tax friendly subset of the aforementioned Specific ID method. The goal of HIFO is to minimize gains and maximize losses. When you use HIFO, you first dispose of the coins with the highest cost basis. This leads to the least amount of gains (or highest amount of losses) and overall taxes.