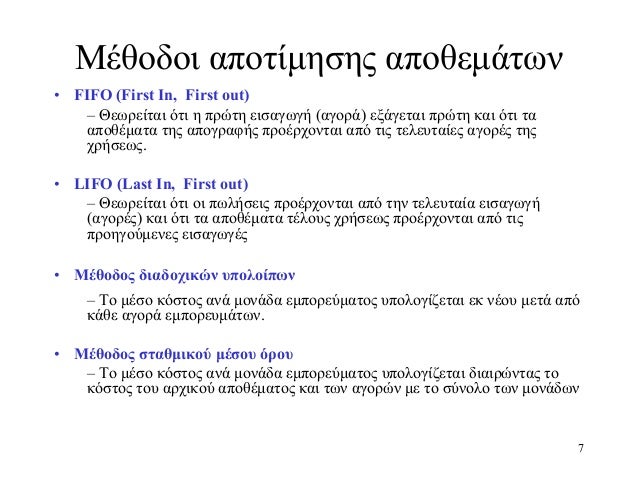

What is the difference between FIFO vs. LIFO?

- First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method.

- Last-in, first-out (LIFO) assumes the last inventory added will be the first sold.

- Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

Do most companies use FIFO or LIFO?

The FIFO method is the standard inventory method for most companies. FIFO gives a lower-cost inventory because of inflation; lower-cost items are usually older. LIFO is a newer inventory cost valuation technique (accepted in the 1930s), which assumes that the newest inventory is sold first. LIFO gives a higher cost to inventory.

How would FIFO and LIFO affect the income taxes paid?

The main difference between LIFO and FIFO is based on the assertion that the most recent inventory purchased is usually the most expensive. If that assertion is accurate, using LIFO will result in a higher cost of goods sold and less profit, which also directly affects the amount of taxes you’ll have to pay. What is LIFO?

Can you switch from FIFO to LIFO?

Therefore, switching from FIFO to LIFO can have a significant impact on all financial statements. A business switching from FIFO to LIFO will need to consider whether it needs to restate its financial data for prior years to reflect the new method or only apply the new method to the current and future years.

Is change from LIFO to FIFO retrospective?

Under U.S. GAAP, retrospective adjustments are NOT made to the financial statements if a company is changing inventory method: A. From LIFO to FIFO.

Can you change inventory methods?

The IRS requires you commit to an inventory cost method the first year your business files its tax return and encourages you to maintain consistency throughout the years. However, the IRS does allow your company to apply to change your inventory cost method.

Can you mix FIFO and LIFO?

When I sold a stock I selected FIFO, but after I got the statement for that transaction, I would like to change it to LIFO, can I still do that ? Yes, you can choose which stocks you sell by giving the proper instructions to your stock broker.

Is LIFO going away?

In any case, it is premature to say that LIFO is on its deathbed. Indeed, small companies not required to use IFRS may very well stay on LIFO. For tax planning purposes, companies may consider reducing their inventories and their LIFO reserves gradually between now and changeover dates to IFRS.

Why is LIFO banned in IFRS?

IFRS prohibits LIFO due to potential distortions it may have on a company's profitability and financial statements. For example, LIFO can understate a company's earnings for the purposes of keeping taxable income low. It can also result in inventory valuations that are outdated and obsolete.

Can you switch from average cost to FIFO?

Furthermore, you should be aware that you cannot simply convert from Average Cost to FIFO just because you want to, or because you change computer software.

How do you elect out of LIFO?

To elect out of LIFO, you would file a change of accounting method (Form 3115) with your timely filed tax return. The pro in this scenario is income pickup can be spread out over four years. The con is that once you elect out of LIFO, you must wait five years before you can elect back into it.

Can you switch from FIFO to weighted average?

If company changes its inventory valuation method from FIFO to weighted average method then it is basically changing the principle of valuation as FIFO follows a particular cost flow assumption whereas weighted average method uses weighted average of the cost at which inventory was held at the beginning of the period ...

Should I sell FIFO or LIFO?

FIFO vs LIFO Stock Trades Under FIFO, if you sell shares of a company that you've bought on multiple occasions, you always sell your oldest shares first. FIFO stock trades results in the lower tax burden if you bought the older shares at a higher price than the newer shares.

Should I sell my oldest or newest shares first?

Shares with the most recent acquisition date are sold first, regardless of cost basis. Shares with the greatest cost basis are sold first. If more than one lot has the same price, the lot with the earliest acquisition date is sold first.

Does Robinhood use FIFO?

Robinhood uses the “First In, First Out” method. This means that your longest-held shares are recorded as having been sold first when you execute a sell order. The shares themselves are not specifically tracked, but the cost associated with those shares is expensed first.

How to compare companies using LIFO method?

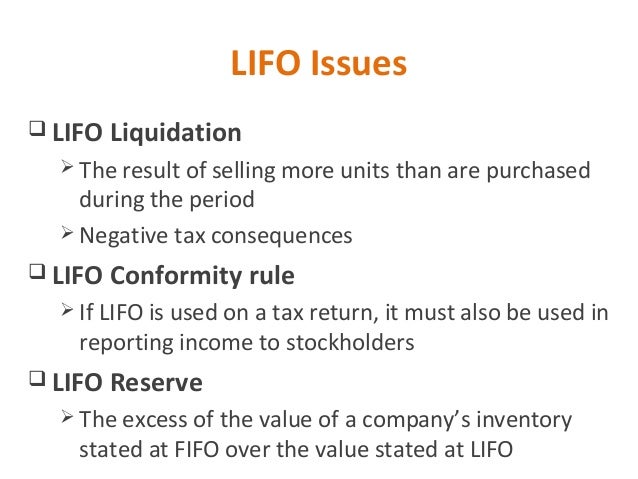

To compare companies that use the LIFO method with other companies, the inventory amount has to be adjusted by adding the disclosed LIFO reserve to the inventory balance that is reported on the balance sheet. The cost of sales figure should also be adjusted by subtracting the increase in the LIFO reserve during the period from the cost of sales amount reported on the income statement.

What happens if LIFO reserve decreases?

If the LIFO reserve decreases during a reporting period, the decrease in the reserve should be added to the cost of the sales amount which is reported on the income statement.

What is LIFO in Xtractor?

Xtractor Inc. uses LIFO to evaluate its inventory. The price of production inputs within the company’s industry has been decreasing for the last few years. To compare the gross profit of Xtractor with other companies reporting using FIFO, an analyst would need to:

Is LIFO used in comparison to FIFO?

It is oftentimes necessary to compare the financial statements of companies that use LIFO against companies that use FIFO. The use of the LIFO reserve makes this possible. For example, The LIFO reserve disclosure enables adjustments to be made to the financial statements of a US company that uses the LIFO method, ...

Does LIFO reserve decrease?

Since the prices of inventory have been decreasing, the LIFO reserve must have been decreasing as well. Further, since the company has been reporting a cost of sales lower than the actual replacement cost, due to price decreases, the company’s cost of sales has been underestimated. To make a proper estimation of Xtractor’s cost of sales, the amount of decrease of the LIFO reserve needs to be added to the cost of sales.

Why do companies use FIFO?

While most companies stick with FIFO or LIFO for consistency, sometimes the owners change their minds. When they do, companies must comply with special reporting requirements to keep their investors informed.

What is FIFO in accounting?

FIFO and LIFO represent accounting methods that determine the value of a company's unsold inventory, cost of goods sold and other transactions. Under FIFO, companies attribute the cost of their oldest goods to their newest sales. The opposite is true under LIFO: The cost of the newest goods is attributed to the newest sales. In periods of rising prices, or inflation, FIFO offers the lowest cost of goods sold and the highest reported profits. In periods of falling prices, or deflation, LIFO results in the highest reported profits.

What is FIFO valuation?

The FIFO and LIFO valuation methods are examples of accounting principles that measure the value of inventory. FIFO and LIFO value inventory very differently, so the same inventory can have different balances depending on the method. Therefore, switching from FIFO to LIFO can have a significant impact on all financial statements. A business switching from FIFO to LIFO will need to consider whether it needs to restate its financial data for prior years to reflect the new method or only apply the new method to the current and future years.

What does FIFO mean in inventory?

FIFO stands for first-in, first-out. Under this method, items that go into inventory first are considered to be the items that are sold first for valuation purposes. LIFO stands for last-in, first-out . This valuation method assumes that the latest inventory items are the first sold.

Do you have to file Form 970 to switch to LIFO?

If you plan on changing from FIFO to LIFO for tax purposes, you are required to complete Form 970 and comply with all requirements listed in the form. You must file the form with the return for the first tax year you plan on using LIFO. Switching to LIFO is irrevocable unless you gain permission from the IRS to switch to another method.

Why is LIFO not accurate?

As a result, LIFO doesn't provide an accurate or up-to-date value of inventory because the valuation is much lower than inventory items at today's prices.

Why is FIFO better than COGS?

FIFO can be a better indicator of the value for ending inventory because the older items have been used up while the most recently acquired items reflect current market prices. For most companies, FIFO is the most logical choice since they typically use their oldest inventory first in the production of their goods, which means the valuation of COGS reflects their production schedule.

Why would COGS be higher under LIFO?

In an inflationary environment, the current COGS would be higher under LIFO because the new inventory would be more expensive. As a result, the company would record lower profits or net income for the period. However, the reduced profit or earnings means the company would benefit from a lower tax liability.

When sales are recorded using the FIFO method, what is the oldest inventory?

When sales are recorded using the FIFO method, the oldest inventory–that was acquired first–is used up first. FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet.

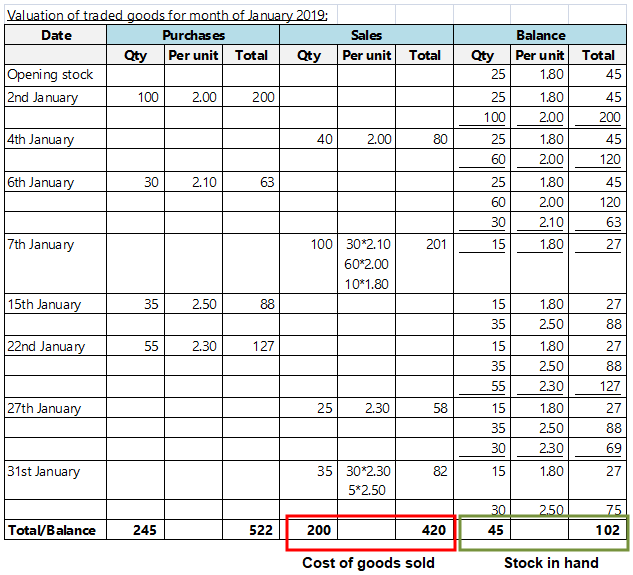

How much is ending inventory in LIFO?

Ending Inventory per LIFO: 1,000 units x $8 = $8,000. Remember that the last units in (the newest ones) are sold first; therefore, we leave the oldest units for ending inventory.

Can seafood companies leave their inventory idle?

In other words, the seafood company would never leave their oldest inventory sitting idle since the food could spoil, leading to losses. As a result, LIFO isn't practical for many companies that sell perishable goods and doesn't accurately reflect the logical production process of using the oldest inventory first.

Is LIFO practical for perishable goods?

As a result, LIFO isn't practical for many companies that sell perishable goods and doesn't accurately reflect the logical production process of using the oldest inventory first.