What is the difference between FIFO vs. LIFO?

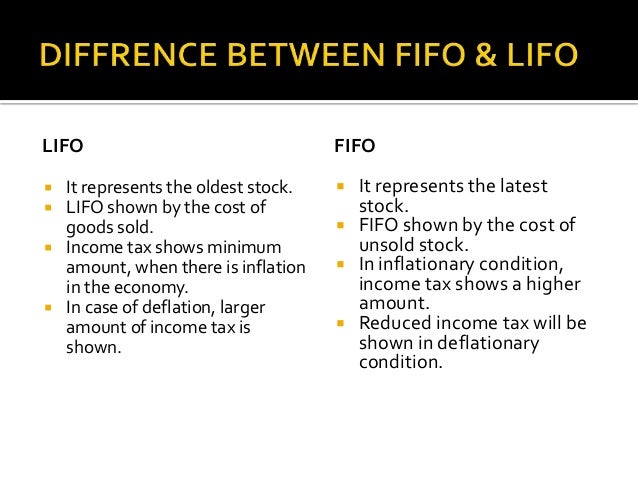

- First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method.

- Last-in, first-out (LIFO) assumes the last inventory added will be the first sold.

- Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

Do most companies use FIFO or LIFO?

The FIFO method is the standard inventory method for most companies. FIFO gives a lower-cost inventory because of inflation; lower-cost items are usually older. LIFO is a newer inventory cost valuation technique (accepted in the 1930s), which assumes that the newest inventory is sold first. LIFO gives a higher cost to inventory.

How would FIFO and LIFO affect the income taxes paid?

The main difference between LIFO and FIFO is based on the assertion that the most recent inventory purchased is usually the most expensive. If that assertion is accurate, using LIFO will result in a higher cost of goods sold and less profit, which also directly affects the amount of taxes you’ll have to pay. What is LIFO?

How do you record change from LIFO to FIFO?

Convert LIFO to FIFO statementAdd the LIFO reserve to LIFO inventory.Deduct the excess cash saved from lower taxes under LIFO (i.e. LIFO Reserve x Tax rate)Increase the retained earnings component of shareholders' equity by the LIFO reserve x (1-T)In the income statement, FIFO COGS = LIFO COGS – Δ LIFO Reserve.

Is it better to sell stock FIFO or LIFO?

FIFO vs LIFO Stock Trades Under FIFO, if you sell shares of a company that you've bought on multiple occasions, you always sell your oldest shares first. FIFO stock trades results in the lower tax burden if you bought the older shares at a higher price than the newer shares.

Should I sell my oldest or newest shares first?

Shares with the most recent acquisition date are sold first, regardless of cost basis. Shares with the greatest cost basis are sold first. If more than one lot has the same price, the lot with the earliest acquisition date is sold first.

Is LIFO better for day trading?

Why Use LIFO? If you sell a portion of your positions on the way up, using LIFO to calculate your cost basis is probably the most advantageous. An intermediate-term momentum trading style like that of Market Wizard Mark Minervini is a perfect example of where LIFO might be useful.

What is the difference between FIFO and LIFO?

On the other hand, FIFO increases net income and increased net income can increase taxes owed. The LIFO method assumes the last item entering inventory is the first sold. Similar Asks.

What is LIFO in inventory?

LIFO moves the latest/more recent costs from inventory and reports them as the cost of goods sold and leaves the first/oldest costs in inventory. A U.S. company may switch from FIFO to LIFO. However, after the switch the company must use LIFO consistently.

Is LIFO to FIFO a change in accounting principle?

Additionally, is LIFO to FIFO a change in accounting principle? A change in inventory valuation (from LIFO to FIFO, from FIFO to LIFO, from average cost to LIFO, etc.) is considered a change in accounting principle.

Why do companies use FIFO?

While most companies stick with FIFO or LIFO for consistency, sometimes the owners change their minds. When they do, companies must comply with special reporting requirements to keep their investors informed.

What is FIFO in accounting?

FIFO and LIFO represent accounting methods that determine the value of a company's unsold inventory, cost of goods sold and other transactions. Under FIFO, companies attribute the cost of their oldest goods to their newest sales. The opposite is true under LIFO: The cost of the newest goods is attributed to the newest sales. In periods of rising prices, or inflation, FIFO offers the lowest cost of goods sold and the highest reported profits. In periods of falling prices, or deflation, LIFO results in the highest reported profits.

Do private companies have to follow GAAP?

Private companies often follow GAAP reporting, though they're not obligated to, because investors and lenders are trained to evaluate GAAP information and demand it from companies. If a private company is making the switch from LIFO to FIFO, its owners will probably want to explain it to stakeholders.

Why is LIFO not accurate?

As a result, LIFO doesn't provide an accurate or up-to-date value of inventory because the valuation is much lower than inventory items at today's prices.

Why is FIFO better than COGS?

FIFO can be a better indicator of the value for ending inventory because the older items have been used up while the most recently acquired items reflect current market prices. For most companies, FIFO is the most logical choice since they typically use their oldest inventory first in the production of their goods, which means the valuation of COGS reflects their production schedule.

Why would COGS be higher under LIFO?

In an inflationary environment, the current COGS would be higher under LIFO because the new inventory would be more expensive. As a result, the company would record lower profits or net income for the period. However, the reduced profit or earnings means the company would benefit from a lower tax liability.

When sales are recorded using the FIFO method, what is the oldest inventory?

When sales are recorded using the FIFO method, the oldest inventory–that was acquired first–is used up first. FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet.

How much is ending inventory in LIFO?

Ending Inventory per LIFO: 1,000 units x $8 = $8,000. Remember that the last units in (the newest ones) are sold first; therefore, we leave the oldest units for ending inventory.

Can seafood companies leave their inventory idle?

In other words, the seafood company would never leave their oldest inventory sitting idle since the food could spoil, leading to losses. As a result, LIFO isn't practical for many companies that sell perishable goods and doesn't accurately reflect the logical production process of using the oldest inventory first.

Is LIFO practical for perishable goods?

As a result, LIFO isn't practical for many companies that sell perishable goods and doesn't accurately reflect the logical production process of using the oldest inventory first.