The tax professionals we consult strongly recommend FIFO as the more conservative treatment. You also need to stick with one tax treatment for all your years of tax returns. You cannot switch from LIFO to FIFO each year.

What is the difference between FIFO vs. LIFO?

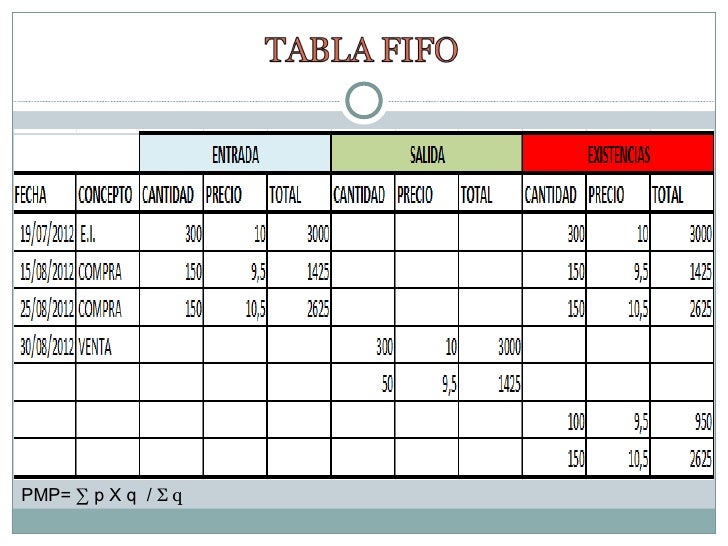

- First-in, first-out (FIFO) assumes the oldest inventory will be the first sold. It is the most common inventory accounting method.

- Last-in, first-out (LIFO) assumes the last inventory added will be the first sold.

- Both methods are allowed under GAAP in the United States. LIFO is not allowed for international companies.

Why would a company use LIFO instead of FIFO?

Key Takeaway

- Last in, first out (LIFO) is a method used to account for how inventory has been sold that records the most recently produced items as sold first.

- The U.S. ...

- Virtually any industry that faces rising costs can benefit from using LIFO cost accounting.

Do most companies use FIFO or LIFO?

The FIFO method is the standard inventory method for most companies. FIFO gives a lower-cost inventory because of inflation; lower-cost items are usually older. LIFO is a newer inventory cost valuation technique (accepted in the 1930s), which assumes that the newest inventory is sold first. LIFO gives a higher cost to inventory.

How would FIFO and LIFO affect the income taxes paid?

The main difference between LIFO and FIFO is based on the assertion that the most recent inventory purchased is usually the most expensive. If that assertion is accurate, using LIFO will result in a higher cost of goods sold and less profit, which also directly affects the amount of taxes you’ll have to pay. What is LIFO?

Can a company change its inventory costing method?

The IRS requires you commit to an inventory cost method the first year your business files its tax return and encourages you to maintain consistency throughout the years. However, the IRS does allow your company to apply to change your inventory cost method.

What type of change would a change from LIFO to FIFO be considered?

Key Takeaways. An accounting change is a change in accounting principles, accounting estimates, or the reporting entity. A change in accounting principles is a change in a method used, such as using a different depreciation method or switching between LIFO to FIFO inventory valuation methods.

Can a company change its inventory method each accounting period?

But can a company change its inventory method each accounting period? In short, no. Switching inventory methods continuously actually breaches the accounting principles of consistency. Though you may change your accounting method at the end of an accounting period, you can't do it each accounting period.

How does switching from FIFO to LIFO affect accounting statements?

Financial Statement Impact of LIFO-to-FIFO Switch In times of cost increases, LIFO will result in a higher cost-of-goods expense, but lower end-of-period inventory values. However, in times of cost decreases, LIFO will result in a lower cost-of-goods expense, but higher end-of-period inventory values.

Why LIFO is better than FIFO?

FIFO focuses on using up old stock first, whilst LIFO uses the newest stock available. LIFO helps keep tax payments down, but FIFO is much less complicated and easier to work with.

Why LIFO is not allowed?

IFRS prohibits LIFO due to potential distortions it may have on a company's profitability and financial statements. For example, LIFO can understate a company's earnings for the purposes of keeping taxable income low. It can also result in inventory valuations that are outdated and obsolete.

Can you switch from average cost to FIFO?

Furthermore, you should be aware that you cannot simply convert from Average Cost to FIFO just because you want to, or because you change computer software.

Why would a company switch to the LIFO method of inventory valuation?

Why would a company switch to the LIFO method of inventory valuation? (a) By switching to LIFO, reported earnings will be higher.

How do you elect out of LIFO?

To elect out of LIFO, you would file a change of accounting method (Form 3115) with your timely filed tax return. The pro in this scenario is income pickup can be spread out over four years. The con is that once you elect out of LIFO, you must wait five years before you can elect back into it.

Can a company use both LIFO and FIFO?

The U.S. accounting standards organization, the Financial Accounting Standards Board (FASB), in its Generally Accepted Accounting Procedures, allows both FIFO and LIFO accounting.

Is LIFO or FIFO better for net income?

Since inventory costs have increased in recent times, LIFO shows higher COGS and lower net income – whereas COGS is lower under FIFO, so net income is higher.

Is change from LIFO to FIFO retrospective?

Under U.S. GAAP, retrospective adjustments are NOT made to the financial statements if a company is changing inventory method: A. From LIFO to FIFO.