LIFO The IRS refers to variable annuities funded with taxable money as non-qualified annuities. Roth individual retirement arrangements (IRAs), like non-qualified annuities, contain after-tax money that grows on a tax-deferred basis. The IRS uses the first-in-first-out (FIFO) method to tax partial Roth withdrawals.

How would FIFO and LIFO affect the income taxes paid?

The main difference between LIFO and FIFO is based on the assertion that the most recent inventory purchased is usually the most expensive. If that assertion is accurate, using LIFO will result in a higher cost of goods sold and less profit, which also directly affects the amount of taxes you’ll have to pay. What is LIFO?

How to sell stock with LIFO or FIFO?

How to Sell Stock With LIFO or FIFO. In the United States, the Internal Revenue Service (IRS) allows investors to sell stock using various methods to select the basis of stock when a sale of stock does not liquidate an investor's position. Commonly investors may select stock sales as "first in, first out" ...

How to determine which shares to sell, FIFO or LIFO?

How to Determine Which Shares to Sell, FIFO or LIFO

- FIFO vs LIFO Stock Trades. The first-in, first-out method is the default way to decide which shares to sell. ...

- Tell Your Broker. If you plan to use any method besides FIFO, including LIFO, you must specifically direct your broker as to which shares to sell so that your taxes ...

- 2018 Tax Law Changes. ...

- 2017 Tax Law. ...

What type of business would use LIFO?

- specific identification method

- FIFO

- weighted average method

Do variable annuities use LIFO?

Variable annuity fees and expenses are not tax-deductible. Withdrawals (also called non-periodic distributions) from a non-qualified variable annuity are made on a LIFO, or last-in-first-out, basis. That means withdrawals are fully taxable until all of the capital gains and dividends credited are withdrawn.

What are variable annuities classified as?

Variable annuities should be considered long-term investments, due to the limitations on withdrawals. Typically, they allow one withdrawal each year during the accumulation phase.

Do annuities get a step up in basis?

Unlike other investments, the named beneficiary of a nonqualified annuity does not get a step-up in tax basis to the date of death. However, that doesn't mean the beneficiary will have to pay taxes on the full amount.

When did annuities become LIFO?

August 13, 1982All these various tax law dates can be confusing. Annuities: Distributions from annuities issued after August 13, 1982 or amounts attibutable to contributions made after that date are LIFO.

What are the characteristics of a variable annuity?

A typical variable annuity offers three basic features not commonly found in mutual funds: tax-deferred treatment of earnings; a death benefit; and. annuity payout options that can provide guaranteed income for life.

What is the difference between a fixed annuity and a variable annuity?

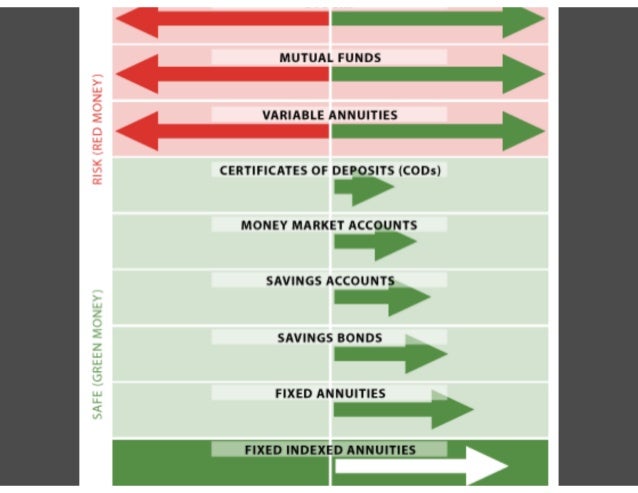

A fixed annuity guarantees payment of a set amount for the term of the agreement. It can't go down (or up). A variable annuity fluctuates with the returns on the mutual funds it is invested in. Its value can go up (or down).

What happens when you inherit a variable annuity?

A person who inherits an annuity has to pay income tax based on the difference between the premium paid into the annuity and the amount still in it when the annuitant died. The amount of annuity taxation depends on how the particular payout for the annuity is set up.

How are variable annuities taxed at death?

Tax-Free Variable Annuity Death Benefits Beneficiaries don't pay tax, however, until they have received an amount that is equal to the total contributions. Any withdrawals made by the owner treated as principal will be subtracted from the calculation.

What is a step up in a variable annuity?

Variable annuities frequently offer a step up feature. A step up allows you to take advantage of rising markets by increasing the death benefit for your beneficiary. When the value of your investment rises, you can lock in the new higher amount, and that becomes the new guaranteed death benefit.

Are variable annuities subject to RMD?

Key Takeaways. Qualified variable annuities held in IRAs are subject to the IRS required minimum distribution (RMD) requirement. At age 72, qualified account owners are required to begin taking RMDs from their IRAs. Roth IRAs are not subject to RMDs while the account owner is alive.

Should I cash out my variable annuity?

Take the money and run But beware: cashing out of an annuity can have tax consequences and surrender charges, and you may miss out on potential benefits, depending on the annuity contract and your personal situation.

How are nonqualified variable annuities taxed?

Nonqualified variable annuities don't entitle you to a tax deduction for your contributions, but your investment will grow tax-deferred. When you make withdrawals or begin taking regular payments from the annuity, that money will be taxed as ordinary income.

Is a variable annuity a fixed unit investment trust?

A variable annuity is a participating unit investment trust. The trust is an "umbrella vehicle" used to collect payments from annuity contract holders.

Are variable annuities exempt securities?

Accordingly, variable annuities are not exempt from regulations under the Investment Company Act of 1940. Because most state laws still classify variable securities as insurance products, state securities regulators have traditionally been precluded from investigating complaints involving variable annuities.

Are variable annuities insurance products?

A variable annuity is a contract between you and an insurance company. It serves as an investment account that may grow on a tax-deferred basis and includes certain insurance features, such as the ability to turn your account into a stream of periodic payments.

Are variable annuity contributions tax deductible?

Key Takeaways. Nonqualified variable annuities don't entitle you to a tax deduction for your contributions, but your investment will grow tax-deferred. When you make withdrawals or begin taking regular payments from the annuity, that money will be taxed as ordinary income.

Can you lose money in a variable annuity?

Because variable annuities are tied to the stock market, you can lose money in a variable annuity. For this reason, fixed annuities are a safer pro...

Are variable annuities protected from creditors?

States provide varying degrees of protection from creditors for variable annuities. Some offer full protection, and others offer none. For example,...

What is a group variable annuity?

A group variable annuity contract is a vehicle for companies that offer 401(k) and other retirement plans. These contracts are offered by insurance...

Who should buy a variable annuity?

People with the objective of capital appreciation and higher risk tolerance should buy variable annuities. These products are not suitable for peop...

What is a GMIB?

A guaranteed minimum income benefit, or GMIB, is a rider that protects variable annuity holders from the market risk inherent in these products. GM...

How does a non qualified variable annuity work?

When you buy a non-qualified variable annuity, the IRS classifies your purchase premium as your cost basis. When you make withdrawals, you only pay taxes on the difference between the account value and your cost basis. On most types of investment accounts, when you die, your heirs receive a stepped-up cost basis. If you heirs liquidate the investment, they only pay taxes on the difference between the value of the investment when they inherited it and the sale price. On variable annuities, your heirs do not get a cost basis step-up, which means they pay taxes on the difference between the account value and the original purchase price. Therefore, variable annuities result in more taxes for your heirs than other kinds of securities.

How long is variable annuity?

Variable annuities are deferred annuity contracts and usually have terms of at least four years. Aside from paying taxes, you also pay surrender fees to the annuity issuer if you make withdrawals before the annuity term ends.

What is a Roth annuity?

The IRS refers to variable annuities funded with taxable money as non-qualified annuities. Roth individual retirement arrangements (IRAs), like non-qualified annuities, contain after-tax money that grows on a tax-deferred basis. The IRS uses the first-in-first-out (FIFO) method to tax partial Roth withdrawals.

What is the penalty for premature withdrawal from an annuity?

To deter investors from making premature withdrawals, the IRS assesses a 10 percent premature withdrawal penalty. You pay this penalty along with state and federal income tax.

What are the tax consequences of variable annuities?

The Internal Revenue Service (IRS) gives preferential tax treatment to variable annuities, which means that your premium grows tax-deferred. However, as with other types of tax-deferred investments, you do have to pay taxes when you make withdrawals and your age has an impact on the amount ...

What happens to investment accounts when you die?

On most types of investment accounts, when you die, your heirs receive a stepped-up cost basis. If you heirs liquidate the investment, they only pay taxes on the difference between the value of the investment when they inherited it and the sale price.

Can you rollover a 401(k) into an annuity?

You can roll money from a tax-deferred retirement account, such as a 401k, into a variable annuity without having to pay any taxes at the time of the rollover. When you eventually withdraw funds from the contract, you pay ordinary income tax on the withdrawal.

Why is FIFO better than COGS?

FIFO can be a better indicator of the value for ending inventory because the older items have been used up while the most recently acquired items reflect current market prices. For most companies, FIFO is the most logical choice since they typically use their oldest inventory first in the production of their goods, which means the valuation of COGS reflects their production schedule.

Why is LIFO not accurate?

As a result, LIFO doesn't provide an accurate or up-to-date value of inventory because the valuation is much lower than inventory items at today's prices.

Why would COGS be higher under LIFO?

In an inflationary environment, the current COGS would be higher under LIFO because the new inventory would be more expensive. As a result, the company would record lower profits or net income for the period. However, the reduced profit or earnings means the company would benefit from a lower tax liability.

When sales are recorded using the FIFO method, what is the oldest inventory?

When sales are recorded using the FIFO method, the oldest inventory–that was acquired first–is used up first. FIFO leaves the newer, more expensive inventory in a rising-price environment, on the balance sheet.

How much is ending inventory in LIFO?

Ending Inventory per LIFO: 1,000 units x $8 = $8,000. Remember that the last units in (the newest ones) are sold first; therefore, we leave the oldest units for ending inventory.

Is LIFO practical for perishable goods?

As a result, LIFO isn't practical for many companies that sell perishable goods and doesn't accurately reflect the logical production process of using the oldest inventory first.

What is variable annuity?

As for what they are, a variable annuity is a type of retirement account. The owner of the account has an investment fund that is intended, after retirement, to provide a regular monthly income in an amount that is subject to the fluctuations in value of the investments selected for the account.

What are the pros and cons of variable annuities?

Variable Annuities: The Pros and Cons 1 They can end up generating significant taxes. 2 They usually come with high fees. 3 They are so complex that many who own them don’t understand them.

Do variable contracts have to be taxed?

Although variable contracts grow tax-deferred until retirement , they impose the same 10% early withdrawal penalty as traditional IRAs and qualified plans. 1 . All distributions from these contracts are taxed as ordinary income unless the contract was placed inside a Roth IRA. 7 .

Is a variable annuity probate exempt?

As with fixed and indexed annuities, variable annuity contracts are unconditionally exempt from probate. That allows the beneficiaries to get their money quickly. 4

Do variable annuities provide superior returns?

You also need to know the pros and cons of these unique products. Variable annuities can provide superior returns over the long haul, but it is prudent to learn about the tax treatment of this financial product before you invest.

Do variable annuities have a contribution limit?

They aren’t subject to contribution limits. The money in them grows tax deferred. Many states protect them from creditors. They are exempt from probate. Cons of Variable Annuities. They can end up generating significant taxes. They usually come with high fees.

Do variable products have living and death benefit riders?

Most variable products also contain living and death benefit riders that guarantee either a minimum account value or a stream of income (see below). Nevertheless, even this information is not enough to allow you to make an educated buying decision. You also need to know the pros and cons of these unique products.

What is variable annuity?

Some insurance companies offer variable annuities, which are tax-deferred investments that distribute money to the annuity holder in a variety of ways, including as a series of regular payments for the rest of her life. Unlike fixed annuities, variable annuities allow their owners to choose how the money is invested. The amount of taxes due on withdrawals from a variable annuity depends on how the owner takes the money and when she opened the annuity.

How are variable annuities settled?

Variable annuity owners can settle their annuities into regular payments for either a fixed period or for life. Annuity settlement payments are considered both a return of capital and payment of taxable growth. The amount of tax due on each payment is determined by the exclusion ratio, which is the ratio of original investment to expected payout. If the recipient of annuity settlement payments lives long enough that he has received all of his original investment, any subsequent payments become entirely taxable.

What is the responsibility of an annuity owner?

The company issuing the owner’s annuity is responsible for sending a Form 1099 to both the Internal Revenue Service and the annuity owner reporting any taxable withdrawals. Additionally, the company is responsible for making adjustments to the annuity owner’s basis in the policy. The taxable withdrawal from an annuity is included on the recipient’s Form 1040 (Individual Tax Return).

When did the TEFRA change the accounting method for annuities?

The Tax Equality and Fiscal Responsibility Act of 1982 (TEFRA) changed the accounting method for withdrawals from annuities opened after Aug. 13, 1982 . Annuity withdrawals subject to TEFRA occur on the LIFO method, while annuities opened before that date are withdrawn on a first-in, first-out, or FIFO, method. This method allows annuity owners to take all of their original investment out of the annuity tax free before any withdrawals come from growth.

Is growth taxed on an annuity?

The growth in an annuity compounds untaxed while it is left in the annuity. This feature is especially important for variable annuities, as the owner does not have to pay tax on the sale of any investments inside the annuity when changing the allocation. When it's time to pay taxes on the earnings, the money is taxed as ordinary income.

Why are non-qualified annuities so popular?

Annuities have become increasingly popular. Tax deferred growth is arguably the most appealing feature of a non-qualified annuity. This permits earnings on premiums to avoid income taxation until distribution. Long-term savings advantages and the ability to insure an income stream for life add to annuities' increasing appeal.

What are the phases of the annuity contract?

There are two distinct phases of the annuity contract: the accumulation phase and the annuitization phase. During the accumulation phase, the owner generally is not taxed on the earnings credited to the cash value of the annuity contract unless a distribution is received. The accumulation phase continues until the annuity contract is terminated or the annuitization phase begins. The annuitization phase starts when the contract value is applied to an annuity payout option. This phase continues until the last payment is made according to the annuity payout period chosen by the owner (or in some cases, the beneficiary).

What happens to an annuity after death?

If the owner of the annuity is a non-natural owner, then the annuitant's death triggers the distribution at death rules. In addition, the distribution at death rules are also triggered by a change in the annuitant on an annuity contract owned by a non-natural person. Income Tax. Unlike death benefits paid from life insurance policies, the beneficiary may be taxed on distributions made from an annuity after the owner's death. Amounts paid under the five-year rule are taxed in the same manner as partial withdrawals or full surrenders, and amounts paid under an annuity option are taxed in the same manner as annuity payments. For variable annuity contracts issued on or after 10/29/79, and for all fixed annuity contracts, there is no "step-up" in basis for income tax purposes and the beneficiary pays income tax on the earnings. However, the beneficiary is entitled to deduct a portion of estate tax paid on the annuity for income tax purposes. For variable annuity contracts issued prior to 10/21/79, there is a "step-up" in basis for income tax purposes and no income tax is payable on the earnings.

What age does 10% penalty apply to annuities?

The 10% penalty tax generally applies to the taxable amount of distributions from annuities made before the owner attains age 59½. However, there are exceptions for distributions: (1) made as a result of the owner's death or disability; (2) made in substantially equal periodic payments over the life or life expectancy of the owner, or joint lives or joint life expectancy of the owner and designated beneficiary; (3) made under an immediate annuity; or (4) attributable to investment in the annuity made prior to 8/14/82.

What age can you withdraw from an annuity?

Annuities are designed to function as retirement investment vehicles, placing withdrawals after the attained age of 59 1/2. Should the annuity owner begin withdrawals following this age and assuming that they have satisfied any relevant surrender schedule, they will not be assessed fees outside of their tax liabilities. However, should the annuity owner opt to receive withdrawals prior to reaching the age of 59 ½, they may be subject to a 10% IRS penalty on any gains posted to-date. One exception to this rule is if the annuity owner has established an agreement with the IRS, referred to as substantially equal periodic payments (SEPP). Under this agreement, equal withdrawal payments can begin prior to the annuity owner’s age of 59 ½ without penalty as long as they continue to the agreed upon future date, which at a minimum is the later of age 59 ½ or a 5 year period.

When is an annuity gift taxable?

When an annuity is gifted to another party, the transaction triggers a taxable event for the donor. Any relevant capital gains will be taxed at the current owner’s tax bracket. And, should the gift occur prior to the annuity owner’s age of 59 ½, the transaction will be subject to a 10% IRS early withdrawal penalty. Two exceptions may apply; should the transfer occur between spouses or former spouse (as in the event of a divorce settlement), or if the annuity was issued prior to April 23, 1987. Annuities issued prior to this date will be taxed following donation when the contract is surrendered rather than at the time of transfer.

What is aggregation in annuity?

Purchasing several individual annuity contracts from a single insurance company within the same calendar year is often referred to as aggregation. In this scenario, the IRS treats these purchases as a single transaction in order to prevent the owner of the policies from manipulating the basis in each contract. Aggregation can result in an unexpected tax liability for the annuity owner. This rule does not apply when contracts are purchased from different insurance companies or if one annuity is deferred and another is immediate.

What Is a Nonqualified Variable Annuity?

Nonqualified variable annuities are tax-deferred investment vehicles with a unique tax structure. While you won’t receive a tax deduction for the money you contribute, your account grows without incurring taxes until you take money out, either through withdrawals or as a regular income in retirement.

Why are variable annuities attractive?

Variable annuities can be attractive from a tax perspective because of the deferral feature that allows you to postpone tax on your investment gains. However, at some point, you or your beneficiaries will have to pay tax on the income earned in the contract.

What is the penalty for a variable annuity withdrawal?

As with other tax-deferred accounts intended for retirement, variable annuity withdrawals of any kind—whether a single withdrawal or a stream of monthly payments—taken before age 59½ are subject to a 10% early withdrawal penalty on the taxable portion of the payment. 8

What happens to an annuity when you die?

The variable annuity contract may provide that at your death, a person you name as a beneficiary will receive a lump-sum death benefit. 7 Depending on the terms of the contract, when a death benefit becomes payable to a beneficiary, some taxes may be due. Even though this is an inheritance, the beneficiary must pay income tax on the portion ...

What to do before taking out an annuity?

Before taking withdrawals from a nonqualified variable annuity—or if you inherit money from one—it is important to seek competent tax advice . Making a wrong move could create a hefty tax bill.

What happens if you surrender an annuity?

If you “surrender” the contract, which means cashing it in before you start to receive annuity payments, you may face a significant surrender charge imposed by the insurer. 9 The portion of the money that represents your investment in the contract is tax-free, but any additional amount is taxable as ordinary income.

Is a nonqualified variable annuity a retirement account?

A nonqualified annuity, on the other hand, is not considered a retirement account for tax purposes and doesn’t earn you a deduction—even if you are using it to save for retirement. You make contributions to a nonqualified variable annuity with after-tax dollars, like adding money to a bank account or any investment outside of a retirement plan.

Forums Under Maintenance

My question is if a client has an IRA (in an annuity) and decides to convert to a Roth. I understand the taxable implications of conversions. My question is which rule supercedes which, on withdrawals? Roths are withdrawn as FIFO but annuities are withdrawn as LIFO.

The forums are temporarily unavailable for posting while undergoing maintenance

My question is if a client has an IRA (in an annuity) and decides to convert to a Roth. I understand the taxable implications of conversions. My question is which rule supercedes which, on withdrawals? Roths are withdrawn as FIFO but annuities are withdrawn as LIFO.

How long does an annuity last?

With this option, the value of your annuity is paid out over a defined period of time of your choosing, such as 10, 15, or 20 years. Should you elect a 15-year period certain and die within the first 10 years, the contract is guaranteed to pay your beneficiary for the remaining five years.

What are the two most common factors used to determine annuity payments?

Methods for taking annuity payouts include the annuitization method, the systematic withdrawal schedule, and the lump-sum payment. Gender and age are the two most common factors used to determine payments.

How do you add money to an annuity?

2 During the accumulation phase, you can add funds to your annuity contract by depositing cash, converting life insurance cash values, or doing a 1035 exchange from another annuity (to name a few ways of contributing). 3 If you follow the annuity rules, your annuity will accumulate earnings on a tax-deferred basis until you begin to make withdrawals.

What are the methods of annuity payout?

Methods for taking annuity payouts include the annuitization method, the systematic withdrawal schedule, and the lump-sum payment.

What factors affect life insurance?

There are several factors that insurance companies use to compute your monthly payment amount, but two of the most common are gender and age—both of which affect your life expectancy. As women have a longer life expectancy than men, they will not receive as high a monthly payment as their male counterparts. And, of course, the older you are, the lower your life expectancy. Thus, a 75-year-old man with the life option will receive a higher monthly payout than a 65-year-old man.

Why is the monthly payment lower than the life option?

The monthly payment is lower than that of the life option, because the calculation is based on the life expectancy of both spouses.

What is a life with guaranteed term?

Life With Guaranteed Term. Many people like the idea of income for life (which they get with the life option), but they are afraid to choose it in case they die in the near future. The life-with-guaranteed-term option gives you an income stream for life (like the life option), so it pays you for as long as you live.

How are distributions taxed for non-qualified annuities?

There are two basic ways distributions are taxed for non-qualified annuities: - If the distribution from a non-qualified annuity is part of an actual annuitization of the contract, i.e. a periodic payout of the contract over the annuitant’s lifetime, the taxable part of each payment is prorated over the annuitant’s lifetime.

How are annuities taxed?

First, to the extent the annuity is deferred, taxation on the growth in the annuity’s value is income tax deferred until distributions are made from the policy. This is a different tax treatment than other savings vehicles, such as a bank account, where the growth is income taxable annually even if the contract owner doesn’t withdraw any of the growth. Next – to the extent any of the distributions being paid out from the annuity are taxable: they are taxed at ordinary income tax rates, not capital gains rates. This is true even if the assets inside the annuity are mutual fund subaccounts (a “variable annuity”) and would have otherwise been subject to capital gains treatment.

What is taxation on annuities?

Taxation depends on how the annuity is owned, and how distributions are made from the product. And if these details are ignored, there are hidden “gotchas” that can result in radically different tax outcomes.

What happens if you gift an annuity to a widow?

Here is another gotcha. When an annuity is gifted to another party, the transfer triggers a taxable event for the donor. The widow could incur an income tax on any gain in the contract, and if she made this gift before she reaches age 59 ½, she could potentially have a 10% penalty tax as well.

What is an annuity deferral?

1. There are two basic kinds of annuities. One is a “deferred annuity,” where the funds in the contract build up over time and are distributed later. The other is an “immediate annuity,” where funds begin paying out immediately and periodically. These payments may be over an annuitant’s lifetime, for a period certain, or some combination of these measures. And the annuity deferral period is taxed differently than the payout period.

What are the basic tenets of annuity taxation?

There are some fundamental tenets of annuity taxation. These are the four underlying principles that drive the general income tax regime for these products. 1. There are two basic kinds of annuities. One is a “deferred annuity,” where the funds in the contract build up over time and are distributed later. The other is an “immediate annuity,” ...

What happens if a widow surrenders an annuity?

If the heirs surrender the contract, they will have “income in receipt of a decedent (IRD),” and they will have to pay income tax on any gain above what the decedent paid for the annuity.